By Michael O’Neill

The US dollar is in the driver’s seat. US Treasury yields are the fuel. FX traders are buying greenbacks with every rise in Treasury yields and the focus is on 10-year Treasuries. They have risen to 3.10%, from 2.83% between April 17 and May 17. EURUSD dropped from 1.2415 to 1.1765 in the same period.

It is not as if higher US interest rates should come as a surprise to anyone. The year started with the Fed and most economists/analysts forecasting three rate increases in 2018. Some even had four hikes penciled in. Despite the hawkish rate outlook, the US dollar declined. EURUSD climbed from 1.1915 to 1.2550

The reason for that move was the European Central Bank. (ECB) Various ECB members started talking about policy rate normalisation and the issues around ending the quantitative easing program. FX traders concluded that ECB interest rates had far more upside potential than US rates and bought EURUSD. The single currency spent February to May locked in a 1.2160-1.2550 trading band.

A series of weaker than expected Eurozone data, contrasting with robust US economic reports and dovish ECB policy meeting statement and press conference triggered a reassessment of the Fed/ECB interest rate, and the ECB was found lacking. EURUSD positions established in anticipation of hawkish ECB policy were large, and stale. The ensuing position unwind triggered stop-loss selling which exacerbated the move lower. EURUSD is now trading below the January 2018 low, and the bias is for further losses.

The US dollar may be in the driver’s seat, but some traders, believe that if the fuel is rising Treasury yields, the rally may be running out of gas very soon.

Bill Gross, co-founder of Pacific Investment Management Co, and current Portfolio Manager at Janus Henderson Investors, also dubbed the “bond king” for his trading prowess, is one of them. On May 15, he predicted that the 30-year bond yield would be capped at 3.22%, saying the US economy could not support yields higher than 3.25%. His prediction is being tested as this is being written.

The ECB may have disappointed FX traders with their cautious policy stance and their reluctance to hasten the pace of policy normalisation, but it is still going to happen. Net asset purchases, currently €30 billion/month are intended to run out on September 30, although they could be extended. Recent, soft inflation readings are thought to be temporary, and if correct, would support a more hawkish ECB outlook. EURUSD is still above long-term uptrend line support which comes into play in the 1.1500 area.

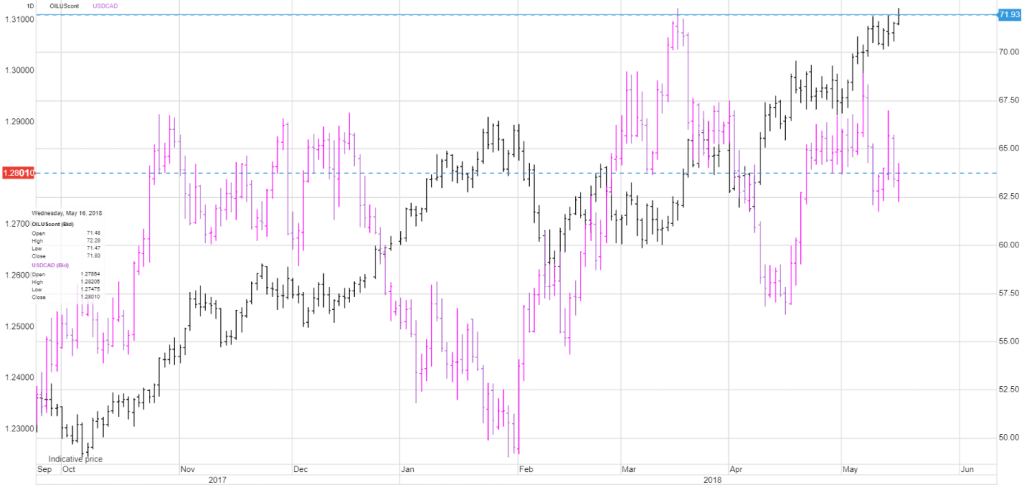

Oil prices used to chauffer Canadian dollar price movements, but that relationship has deteriorated in the past month. West Texas Intermediate (WTI), the North American crude benchmark price, has surged 16.9% since April 9. The Canadian dollar only rose 0.3% during the same period.

Chart: USDCAD and WTI

Source: Saxo Bank

When looked in isolation, it is fair to say the WTI and USDCAD relationship has decoupled. However, it wouldn’t be accurate. Between April 9 and May 17, the Canadian dollar is the best performing major G10 currency and the only currency to have increased in value against the US dollar. The New Zealand dollar lost 5.5%, and the Euro shed 3.8%. Arguably, high oil prices did their job and cushioned the Canadian dollar from the brunt of the US dollar strength.

May 17th is the “line in the sand” day for the successful conclusion of the North America Free Trade Agreement renegotiation. It is a somewhat arbitrarily assigned deadline, suggested by US House of Representatives Speaker Paul Ryan. Mr Ryan said that a deal needs to be concluded by this date for the 2018 version of Congress to review and ratify it.

A signed and sealed deal would trigger a steep sell-off in the Canadian dollar on the assumption, that with NAFTA uncertainty out of the way, the Bank of Canada would be free to raise interest rates. However, recent media reports suggest that in the unlikely chance a deal is announced on May 17, it would be more of an agreement to continue working on the details rather than the finished product. If so, USDCAD losses may be short-lived.

The impact of a non-deal to USDCAD would be minimal as long as the parties continue to work on a resolution.

The US dollar is unlikely to leave the driver’s seat, at least for the next week and perhaps not until the second week in June when the FOMC and ECB policy meetings are held. The issue will be if geopolitical issues, China/US trade talks or Treasury yields provide the fuel.