By Michael O’Neill

COVID-19 is a nasty virus in itself. Then came the variants-UK, Brazilian, and South African. These variants spread easier and quickly, threatening to overwhelm healthcare systems around the globe.

A far more insidious variant infected Statistic Canada. Some analysts refer to it as the StatsCan B.S variant that came to light in February. It caused core-inflation numbers to be depressed. Coincidently, that data is one of the key metrics the Bank of Canada (BoC) uses to fulfil its monetary policy mandate.

The BoC goes to great pains to describe its efforts in calculating inflation. Its quarterly monetary policy report explains how it looks through transitory inflation movements, using various tools and models to assess results. To that end, their preferred measures of core-inflation are CPI-trim, CPI-median, and CPI-common. (a more detailed explanation is in the MPR).

Statistics Canada reported its three Core inflation measures rose a combined average of 1.5% y/y. on February 17. That news is important as evidenced by the BoC monetary policy statement three days later.

The headline read: “Bank of Canada will hold current level of policy rate until inflation objective is achieved, continues quantitative easing.”

Except the results were not accurate. On February 22, Stats Canada issued a revision and said the January core CPI rose 1.77% rather than 1.5% as reported. They said the correction was necessary because “methodological changes to the seasonal adjustment models were applied to some input series. Following feedback from users, Statistics Canada has determined that these changes require further evaluation and analysis.”

It is doubtful they arrived at the decision on their own initiative. Why?

A February 24 Financial Post article explained it, writing “Statistics Canada sent emails to at least 20 economists and analysts apologizing for the inconvenience the agency caused.” That suggests the agency received a fair number of complaints.

Big deal. Mistakes happen. But was it a mistake, or was it a very deliberate attempt by authorities to manipulate the data to serve their purposes?

Investigative journalists know to “follow the money” when they seek answers for a story. Perhaps the same is true with the CPI data. A cynic would suggest that the money trail is a mere four kilometres long and leads from Statistics Canada’s head office to the Parliament Buildings.

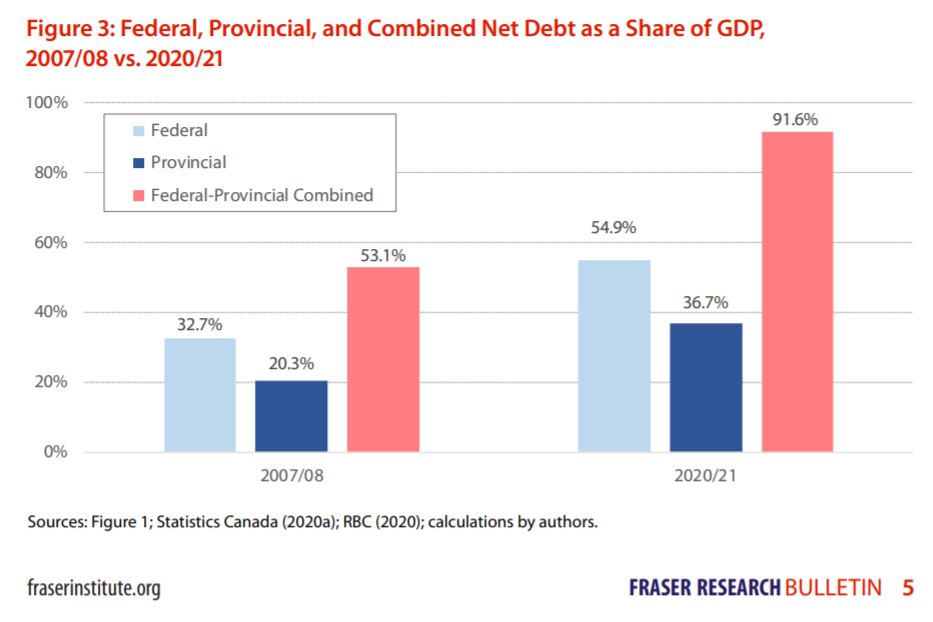

The government needs low interest rates. That’s because the combined Federal and Provincial debt will exceed $2.0 trillion in 2020/2021, or 91.6% of the Canadian economy, according to the Fraser Institute’s February 2021 bulletin. A mere 0.25% increase in the overnight rate will add $5 billion to debt servicing costs.

To put it in perspective, in British Columbia, every man, woman, child or even a newborn owes $43,635.00 as their share of the provincial and federal debt.

Source: Fraser Institute

It is not in the Bank of Canada or the Federal governments interest to see higher interest rates and they are not alone.

The US has racked up over $27.0 trillion as of 2020, and it is not getting better any time soon. President Trump berated Fed Chair Jerome Powell ad nauseum saying interest ratees were too high. The media called it manipulation, but Mr Powell took the message to heart. He told Congress that “The economy is a long way from our employment and inflation goals, and it is likely to take some time for substantial further progress to be achieved.” He also said that inflation can run higher than 2% following periods when it has been below that level. Nor would rates automatically rise in response to low unemployment.

Vice Chair Richard Clarida went a step further reiterating that monetary policy wouldn’t normalize until the end of 2023.

The general public have noticed higher prices for many of their day to day expenses, but those increases do not seem to be reflected in the official inflation numbers. At some point it will become a problem, especially for those on fixed incomes, as rising prices in a low or zero interest rate environment erodes their purchasing power, and their quality of life.

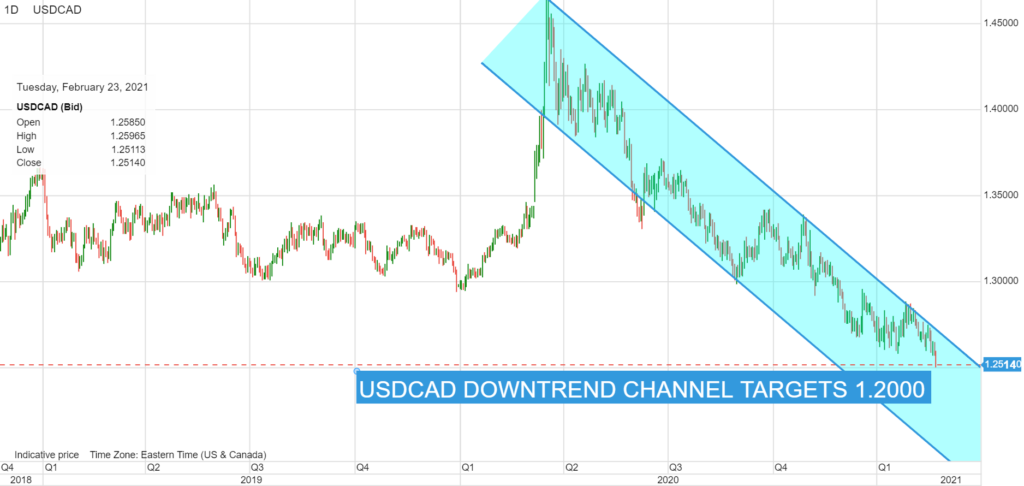

It is not a problem for the Loonie. The Canadian dollar is not suffering from the country’s high debt levels. Far from it. USDCAD dropped over 14% since last March and it has further to go, especially if commodity prices continue to rally.

Chart: USDCAD daily

Source: Saxo Bank

COVID-19 and all its variants have wreaked havoc on global economies. Dodgy economic data reports are merely another variant, and not a barrier to Bank of Canada objectives or to the health of the Canadian dollar.