By Michael O’Neill

The Canadian dollar was the worst performing major currency since the Iran war started and Kevin Warsh’s first Federal Open Market Committee meeting made it worse.

The FOMC left rates unchanged at 3.50%-3.75%, but the Summary of Economic Projections delivered a clear higher-for-longer message. Policymakers raised inflation forecasts, pushed their projected rate path higher and reaffirmed their commitment to restoring price stability.

The updated projections drove the point home. Median PCE inflation for 2026 was revised to 3.6% from 2.7% in March while Core PCE inflation rose to 3.3% from 2.7%. At the same time, the median year-end federal funds rate projection increased to 3.8% from 3.4%.

But that’s not the story.

The story is markets reacted like it was the Powell-Fed and not the Warsh-Fed. Mr. Warsh’s first FOMC meeting statement underscored the difference, being 114 words long compared to the April statement’s 244 words.

That brevity is deliberate. The new Chair has long argued that central banks became overly dependent on signalling future policy intentions. He views tools like the dot plot as dangerous, as they risk creating a false sense of certainty regarding the future path of interest rates. Warsh spent years criticizing this reliance on forward guidance, consistently warning that detailed policy forecasts provide little more than an illusion of precision. Which also makes the market reaction to the dot plots a bit of a head-scratcher.

Ch-Ch-Changes

The greenback and Treasury yields rallied even though Warsh appears to have failed to submit a projection. In the press conference, Mr. Warsh described a number of “task forces” that have been formed to review and recommend changes to all aspects of monetary policy with the message, “changes are coming”. And that’s the key phrase that markets ignored today.

The Fed and BoC Diverge

The Federal Reserve continues to battle inflation while the Bank of Canada continues to grapple with weak economic growth. Canada’s preferred inflation measures remain relatively contained, but sluggish productivity, weak business investment and persistent growth concerns leave policymakers with little room to contemplate a sustained tightening cycle.

The Canada-US two-year spread has deteriorated from roughly -95 basis points in mid-March to near -131 basis points today. The ten-year spread has widened from approximately -82 basis points to around -105 basis points over the same period.

Capital follows returns.

When US Treasury yields significantly outperform comparable Canadian government bonds, global investors have a powerful incentive to own US dollar assets. Those flows have helped propel USDCAD steadily higher even as oil prices surged and geopolitical risks intensified across the Middle East. The result has been a remarkably weak Canadian dollar. Even worse, the Canadian dollar didn’t get any relief when oil prices fell and geopolitical tensions eased dramatically.

Today’s FOMC meeting only reinforced the argument that those spreads could continue moving in favour of the United States.

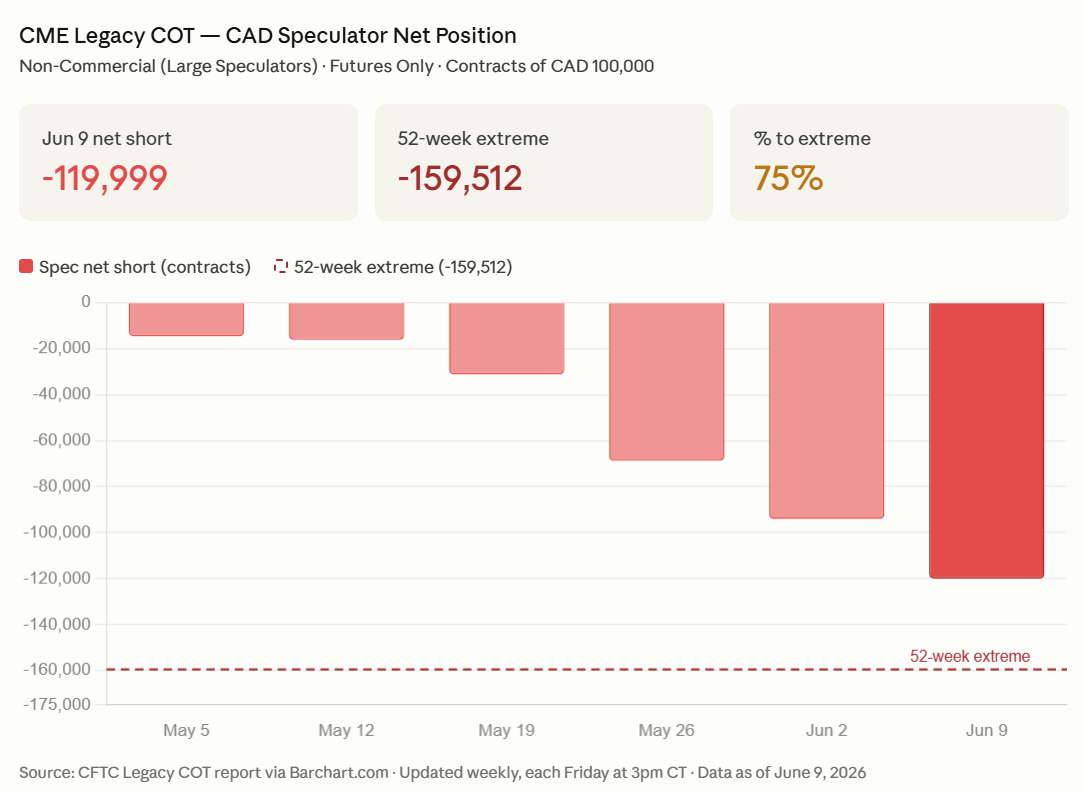

Speculators Have Gone “All-In”

That fundamental backdrop explains why speculative positioning has become increasingly one-sided.

According to the latest Commitment of Traders data, Non-Commercial traders expanded their net short Canadian dollar position from just 14,659 contracts on May 5 to 119,999 contracts by June 9.

That represents an eightfold increase in only six weeks.

Current positioning has already reached roughly 75% of the most extreme bearish Canadian dollar position recorded during the past year. At the current pace of accumulation, speculators could challenge those record levels within weeks.

Commercial traders are sending a very different message.

The so-called smart-money hedgers are now net long 128,812 Canadian dollar contracts and continue to add exposure. Commercials are not momentum traders. Their willingness to accumulate Canadian dollars while speculators aggressively build short positions deserves attention.

This creates an interesting setup.

Fundamentally, the US dollar story remains compelling. The US economy continues to outperform Canada. Yield spreads favour the United States. The first Warsh FOMC delivered a higher-for-longer message. The Federal Reserve’s inflation forecasts moved sharply higher while the Bank of Canada’s growth concerns continue to mount.

On that basis alone, USDCAD should remain well supported.

However, currency markets are not driven solely by fundamentals. They are also driven by positioning. The danger for US dollar bulls is not that they are wrong. The danger is that everyone agrees with them.

Crowded trades can remain crowded for long periods. But when they unravel, the move is usually violent and steep.

That does not mean a Canadian dollar rally is imminent. Wednesday’s FOMC meeting argues otherwise. Nevertheless, the positioning data should not be ignored, and neither should momentum indicators suggesting the Canadian dollar is extremely oversold.

Fed Chair Warsh is still Trump’s man, and he could very well be a dove in hawk feathers. If so, he could soon be throwing the Loonie a life preserver.