Photo:Bing Image Creator

August 31, 2023

- Eurozone inflation data muddies September ECB rate decision.

- US PCE data comes in as expected while weekly jobless claims fall.

- USD opens mixed with EUR underperforming.

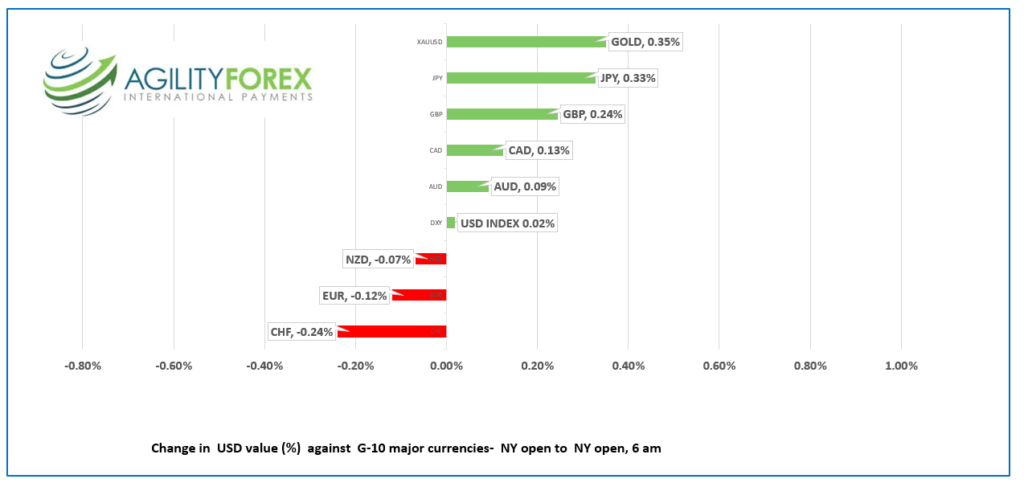

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3546-50, overnight range: 1.3521-1.3556, close 1.3534

USDCAD dropped steadily yesterday after weaker than expected US data questioned the need for further Fed rate hikes. US stocks and bonds rallied, and that positive risk sentiment fueled USDCAD losses. The US Personal Consumption Expenditure data came in as expected while weekly jobless claims rose less than expected.

Oil prices climbed on the back of the falling US dollar. WTI is at the top of its $81.49-$82.29/b overnight range. Prices got an added boost after the weekly EIA Crude oil stocks change report showed inventories falling 10.584 million barrels.

The Canada Q2 current account deficit widened by $3.15 billion to $6.6 billion. Statistics Canada wrote “The trade in goods balance moved into a deficit position for the first time in two years, mostly as a result of lower exports of energy products and farm, fishing, and food products. In contrast, movements in the trade in services and investment income balances moderated the overall increase in the current account deficit.”

USDCAD Technicals

The intraday USDCAD technicals are mildly bearish while prices are below 1.3580 and looking for a break of support at 1.3490 to target 1.3380. USDCAD bears are further encouraged by yesterday’s break below the August 1 uptrend line at 1.3550. A move above 1.3580 negates the downside pressure and shifts the focus back to 1.3650.

For today, USDCAD support is at 1.3520 and 1.3490. Resistance is at 1.3570 and 1.3620. Today’s range 1.3490-1.3590

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

The US economic “Goldilocks” scenario gained more traction after yesterday’s ADP data and GDP report. Both were weaker than expected, which eases pressure on the Fed to raise interest rates further. Stocks rallied, the US dollar dipped, and the US 10-year Treasury yield fell to 4.087% from 4.159%.

Markets didn’t get much insight from Fed’s favorite inflation gauge, Core Personal Consumption Expenditures (PCE) which rose 0.2% m/m and 4.2% y/y, as expected.

Traders should be careful what they wish for. There are other versions of Goldilocks and the Three Bears, where Goldilocks is devoured.

And there are plenty of geopolitical events that could put Goldilocks on the menu, starting with Russia. Ukraine launched a large drone assault on Russian territory, including Moscow, yesterday. Russia claims it thwarted the attack, but some politicians, including Foreign Minister Lavrov and Russia’s Deputy Chairman of its Security Council Dmitry Medvedev, are advocating using nuclear weapons. Yesterday, Medvedev accused the West of being complicit in the war against Russia.

China’s economy is in a mess. Youth unemployment is so high that the government is not publishing statistics. The US is banning high-tech exports to China, while shipping weapons to Taiwan. History is rife with examples of countries attempting to solve economic woes by war. The Russia/Ukraine conflict is at the top of the list, followed by the Syrian Civil War that started in 2011, and the Yugoslavia Wars between 1991 and 2001. Xi Jinping has the hots for Taiwan.

EURUSD peaked in Asia at 1.0940, traded sideways in Europe, then dropped to the session low of 1.0865 after the release of the Eurozone inflation report. Harmonized CPI rose 5.3% y/y in August, compared to the consensus forecast of 5.1%. However, Core-CPI ticked down to 5.3% y/y as expected, from 5.5% in July. The results leave the outlook for ECB rates in September up in the air. The inflation trend is lower, but the pace may be too slow for policymakers. ECB Board Member Isabel Schnabel would not commit to anything.

GBPUSD is modestly bid inside its 1.2674-1.2735 range, thanks to the Eurozone inflation data not bolstering the odds for an ECB rate hike in September. GBPUSD is also supported by hawkish comments from Bank of England Chief Economist Huw Pill, warning that UK rates will rise even if the higher rates hurt the economy.

USDJPY churned inside a 145.72-146.26 range, following weak industrial production data partly due to sluggish Chinese economic activity. Industrial output fell 2.0% compared to forecasts for a 1.4% drop. Retail Sales rose 2.1% in July (forecast 0.8%) but did not provide much support to the currency.

AUDUSD gave up its Asia gains and is trading at the bottom of its 0.6466-0.6508 range in NY due to renewed US dollar demand in Europe.

NZDUSD tracked AUDUSD lower in a 0.5954-0.5978 range. Kiwi traders ignored rising Business Confidence, which improved 9 points in August (actual -3.7, July -12.1), its highest reading since mid-2021.

Today’s US data includes weekly jobless claims, PCE, and Chicago PMI.

Top of Form

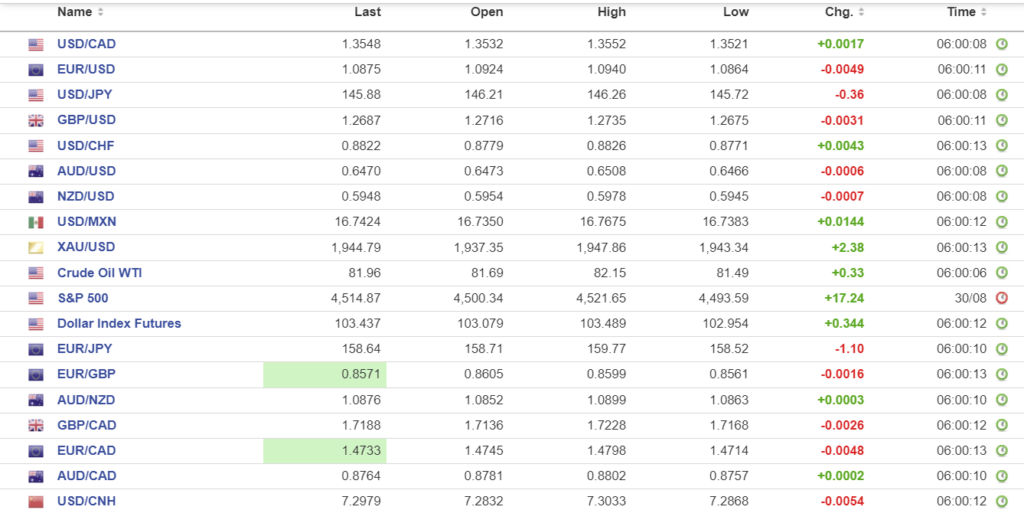

FX high, low, open

Source: Investing.com

China Snapshot

Bank of China Fix: today 7.1811, expected 7.2765, previous 7.1816.

Shanghai Shenzhen CSI 300 fell 0.61% to 3765.27.

Reuters reports that PboC says it will increase loans to private companies. It will encourage and guide institutional investors to buy bonds of private firms.

The official Chinese NBS (National Bogus Statistics) August Manufacturing PMI was 49.7 (forecast 49.4 and previous 49.3). Non-Manufacturing PMI was 51.0(previous 51.5)

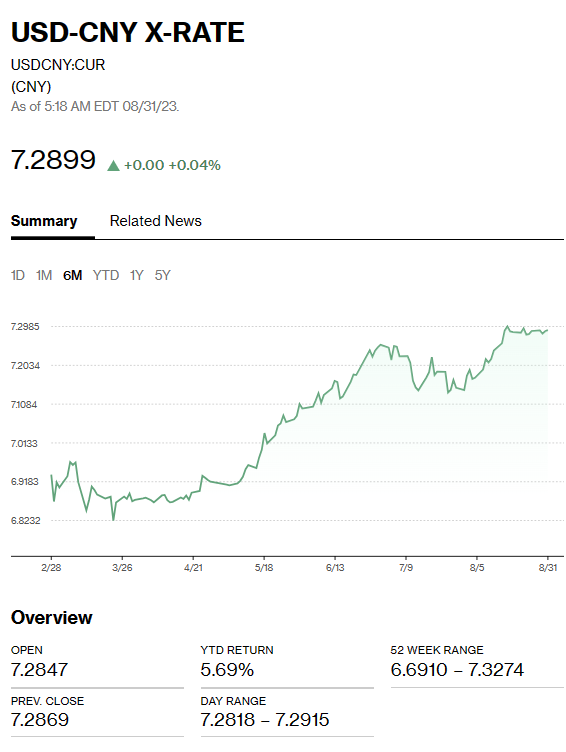

Chart: USDCNY 1 month

Source: Bloomberg