October 30, 2023

- BoC Governor testifies to House of Commons today.

- Daylight Savings Time ends in Europe and UK.

- US dollar opens mixed from Friday morning.

FX at a Glance

Source: IFXA/RP

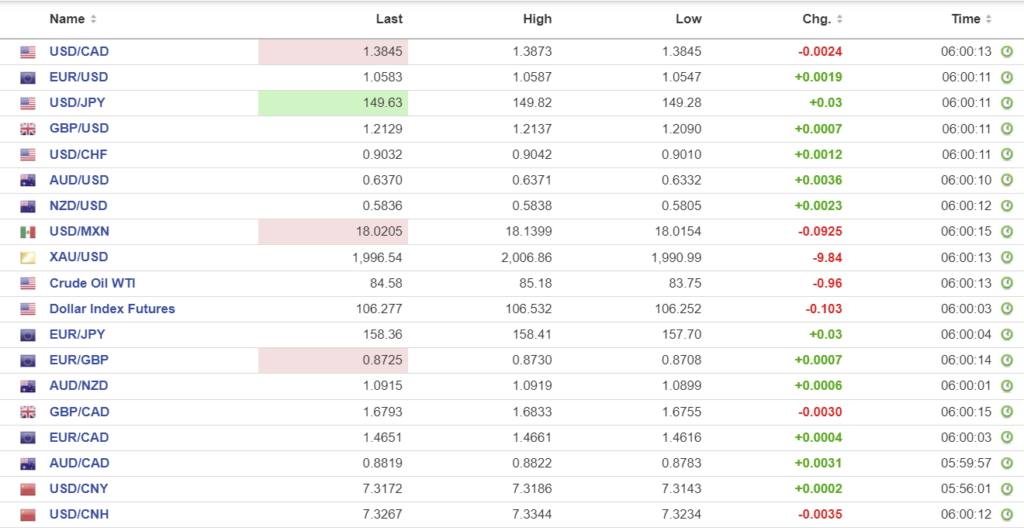

USDCAD Snapshot: open: 1.3843-47, overnight range 1.3843-1.3873, close 1.3874

USDCAD retreated somewhat reluctantly with improved risk sentiment weighing on prices, but softer oil prices acted as a drag.

WTI traded in a $83.75-$85.18/b range partly because of rumours that Saudi Arabia may leave oil prices unchanged for Asian customers.

Bank of Canada Governor Tiff Macklem and his side-kick Carolyn Rogers face-off with the House of Commons Standing committee on Finance. The BoC delivered a hawkish hold on Wednesday when they warned that rates could go higher due to rising inflation, then Macklem contradicted that view on Thursday. He said, “there is more inflation relief in the pipeline and if it comes through, we won’t have to raise rates.” Who knows what he will say today.

USDCAD Technicals

USDCAD is consolidating Friday’s gains but has a bullish bias if prices stay above the 1.3830-1.3840 area. The intraday technicals suggest that a break below 1.3830 risks further losses to 1.3760 while a move above 1.3880 is needed to negate the downward pressure.

Longer, term, USDCAD is appearing overbought and vulnerable to a correction to 1.3760,

For today, USDCAD support at 1.3830 and 1.3760. Resistance at 1.3870 and 1.3920. Today’s expected trading range is 1.3770-1.3860.

Chart: USDCAD DAILY

Source: Daily FX

G-10 FX recap

October is on the ropes; traders will be navigating a minefield of risks this week, and things are as clear as mud. Risk sentiment is on the upswing, as evidenced by gains in European equity markets and S&P 500 futures rising 0.62%.

The S&P 500 is down over for the year, but according to Bloomberg’s John Authers, if you exclude Apple, Amazon, Alphabet, Meta, Microsoft Corp., Nvidia, and Tesla, the S&P is still in positive territory. It remains to be seen if the Fed, Treasury, nonfarm payrolls, or geopolitics will change the story. The usual month-end madness will happen Tuesday.

Treasury Secretary Janet Yellen and her quarterly Treasury refunding announcement will vie with Fed Chair Jerome Powell’s monetary policy statement for dominance on Wednesday.

The Bank of Japan could roil markets if it tweaks its yield curve control policy on November 1, and UK traders are awaiting the Bank of England’s monetary policy decision on Thursday.

The week is loaded with top-tier data culminating in the US employment report Friday, but nothing from the US or Canada today.

EUR/USD drifted higher in a 1.0547-1.0589 range in an understated session due to a holiday in Germany. Preliminary German Q3 GDP fell 0.1% q/q and is -0.3% y/y, both of which were a tad better than expected. However, that news was offset by Euro-area economic sentiment unchanged at 93.3.

GBP/USD traded in a 1.2090-1.2140 range due to mildly improved risk sentiment, which sparked broad-based US dollar sales. Gains are limited ahead of the Fed and BoE meetings later this week.

USD/JPY dipped then bounced in a 149.28-149.82 range and is near the top of that band in early NY. The BoJ meeting is tomorrow, and the risk of a YCC tweak should limit gains.

AUD/USD is at the top of its 0.6332-0.6374 range, supported by the weaker US dollar and by stronger-than-expected Retail Sales (actual 0.9% vs forecast 0.3% m/m)

FX high, low, open

Source: Investing.com

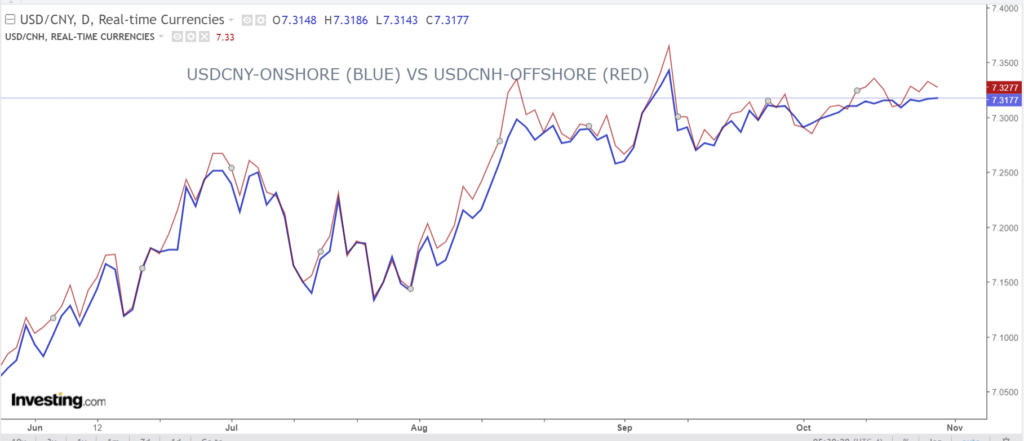

China Snapshot

PBoC fix: today 7.1781, expected 7.3165, previous 7.1782.

Shanghai Shenzhen CSI 300 rose 0.60% to 3583.77

Chart: USDCNY (onshore) vs USDCNH (offshore)

Source: Investing.com