Source: Pixabay

- Russia oil price cap chat sinks WTI

- FOMC minutes and lots of data on tap

- US dollar opens mixed compared to Tuesday

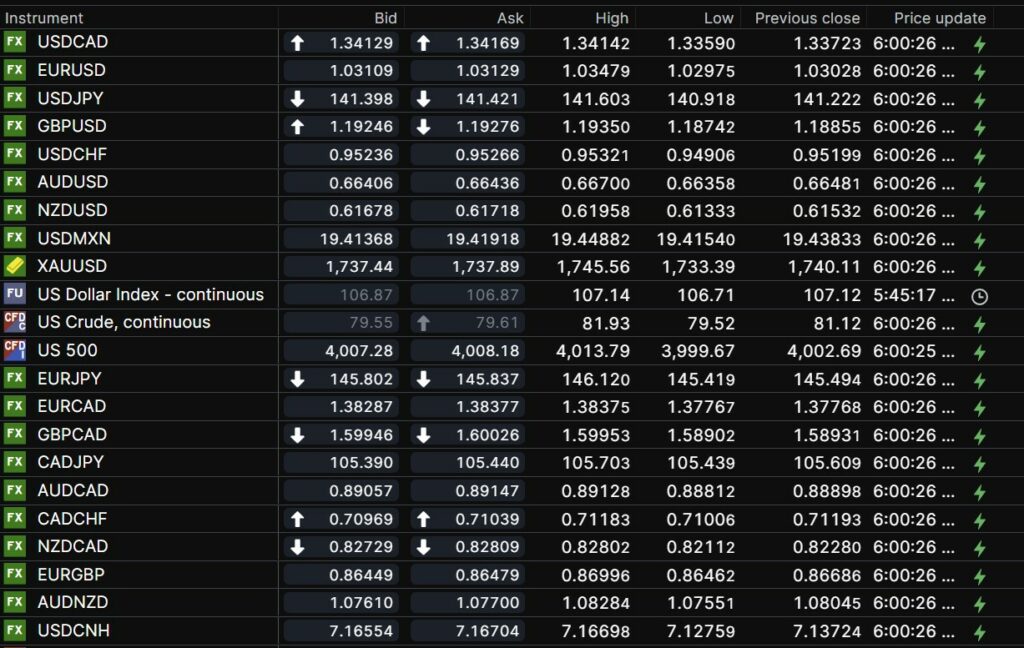

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3413-17, overnight range 1.3359-1.3438, close 1.3372

USDCAD continues to bounce between minor support and resistance levels with direction determined by external forces. Bank of Canada Deputy Governor Carolyn Rogers spoke about financial stability in times of uncertainty which pretty much sums up the world today. Anyway, she didn’t say anything of note and traders ignored her comments.

USDCAD popped in the wake of WTI oil prices dropping from $81.93/barrel to $78.42/b. The G7 are discussing a Russian oil price cap of $60-$70 /b.

Prices rose further after the US data, peaking at 1.3438, so far.

There are no Canadian economic reports today.

USDCAD Technical outlook

The intraday USDCAD technicals are bullish following the break above 1.3380, looking for a break above 1.3460 to extend gains to 1.3570.A move below 1.3350 would extend losses to 1.3300. WTI oil price action is dictating the intraday price action. The November range is intact while 1.3250 limits losses and 1.3550 caps gains.

Longer term, USDCAD traded in a 1.2020-1.3800 range since 2017, ignoring the pandemic pop between March and June 2020. Prices are in an uptrend above 1.2700.

For today, USDCAD support is at 1.3360 and 1.3310. Resistance is at 1.3430 and 1.3460

Today’s range 1.3360-1.3430

Chart: USDCAD weekly

Source: Saxo Bank

G-10 FX recap and outlook

Traders seem to be sick of news of people getting sick in China. There were 28,183 new cases on Tuesday compared to 27,307 on Monday but instead of being risk negative, stocks rose, and the US dollar eased. What a difference a day or two makes.

Evita is not the only one crying for Argentina; the whole country is in mourning after Iran beat Argentina yesterday in Qatar. Belgium will choke on their waffles if they same thing happens to them when they play Canada today.

Its Thanksgiving in America tomorrow and a travel day today with upwards of 2.9 million passengers cueing in airports around the country. It also suggests a low volume, slow US trading session today, despite the data dump and release of the FOMC minutes.

The FOMC minutes may not have much impact on markets as most of American will be headed home or there already. In addition, the blizzard of Fedspeak in the past two weeks is evidence the minutes will suggest policymakers are divided on the pace of rate hikes.

US Durable Goods Orders rose 1.0% in October compared to 0.3% in September. Excluding transportation new orders rose 0.5%m/m.

The good news was offset by a 17,000 jump in initial jobless claims to 240,000.

The results will not do anything to stop the Fed from increasing interest rates further and S&P 500 futures dropped on the news.

Asia equity markets took its lead from the upbeat close on Wall Street and finished the Asian session on a positive note. Australia’s ASX 200 gained 0.70% while Japan’s Nikkei 225 index rose 0.61%.

European bourses are either side of unchanged with many traders in their favourite pub to watch the former Axis powers do battle. S&P 500 futures are close to unchanged after a dull overnight session. WTI oil is down 2.15% from its close while gold slipped 0.14% to $1737.50.

The US 10-year yield is unchanged at 3.759%.

EURUSD extended Tuesday’s gains and rallied from 1.0298 to 1.0348 in early European trading then retreated to the low after Eurozone and German PPI data. The results were mixed. S&P/Markit wrote: “Business activity fell across the Eurozone, but the intensity of the downturn moderated. One upside was the cooling of price pressures, most notably in the manufacturing sector.

EU and Russia tensions are unlikely to improve any time soon after the EU Parliament declared Russia a “state sponsor of terrorism.”

The intraday EURUSD technicals are bullish above 1.0260.

GBPUSD is at the top of its 1.1874-1.1935 range. Prices are getting a bit of a lift from speculation that all the bad news for the currency is priced in and anticipation of a turn in the long-term US dollar rally. However, prices could drop to 1.1500 and the October uptrend would still be intact.

USDJPY traded in a 140.92-141.60 range. Volumes were lighter than usual due to a holiday in Japan. The BoJ is coordinating a digital currency experiment with three Japanese banks because Bitcoin has worked so well.

AUDUSD bounced in a 0.6636-0.6670 band. The bottom was seen after weaker than expected Markit Manufacturing and Service PPI results for November.

NZDUSD churned in a 0.6133-0.6196 range following the RBNZ’s 75 bps rate hike which lifted the OCR rate to 4.25% and surprised about 50% of analysts. Policymakers discussed a 100 bp hike. The RBNZ expects the economy to fall into a recession in Q2

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

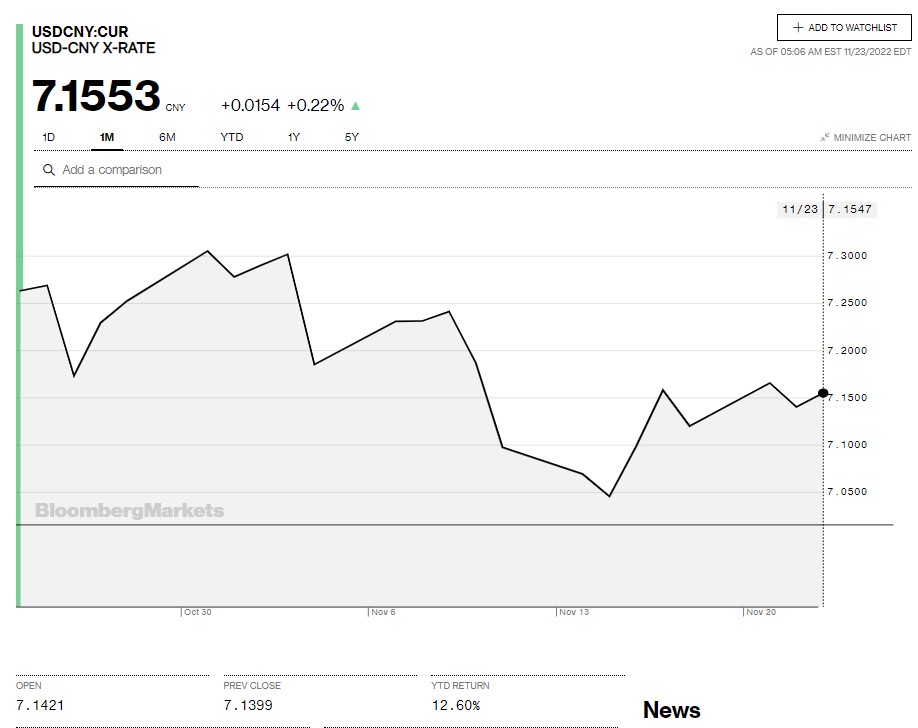

China Snapshot

Today’s Bank of China Fix: 7.1281, previous 7.1667

Shanghai Shenzhen CSI 300 rose 0.11% to 3773.53

PboC advisor Wang Yiming suggests 2023 GDP would be above 5.0% if the impact from Covid ends. He sees limited room for PboC to cut rates

Meanwhile, mass covid testing is occurring in Chengdu while Shenzhen will require 48-hour covid tests to enter public areas.

Chart: USDCNY 1 month

Source: Bloomberg