Photo: HDClipartAll.com

January 5, 2023

- FOMC minutes reiterate hawkish Fed outlook

- Weekly jobless claims fall, and ADP employment rises

- US dollar recoups some of Wednesday’s losses-CAD outperforms

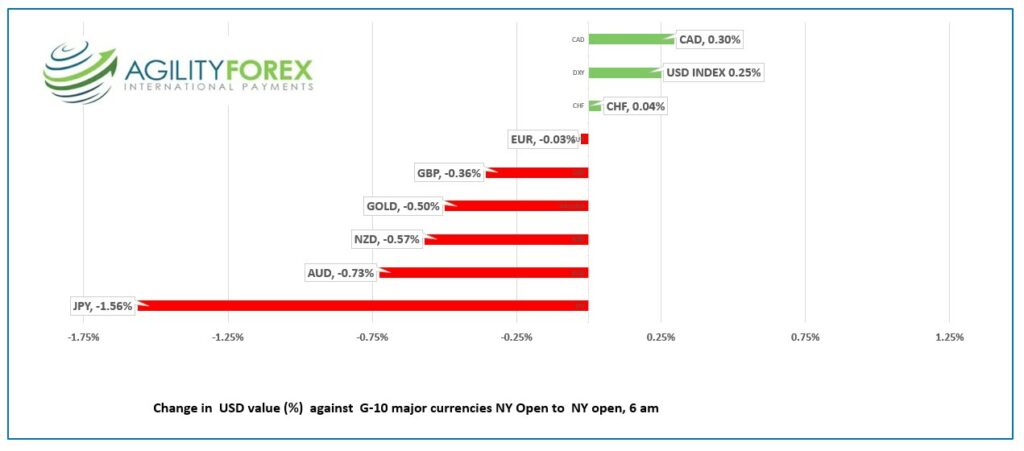

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3506-10, overnight range 1.3472-1.3546, close 1.3478

USDCAD consolidated yesterday’s losses as traders digest yesterday’s FOMC minutes until the release of the US ADP data then rallied to 1.3546

The FOMC minutes stressed the importance of reducing the core services component of the inflation data which would remain “persistently elevated, “if the labor market remained very tight. Essentially, a tight labour market will underpin inflation.

WTI oil traded in a $73.21-$74.89 range. The weekly API crude oil stocks report showed inventories rose by 3.298 million barrels, which helped to limit gains.

USDCAD direction is at the mercy of S&P 500 moves. Trading is likely to be subdued today ahead of Friday’s US and Canadian employment reports.

Canada’s November Trade surplus flipped to a small deficit ($41 million) with exports falling 2.3% largely due to a decline in energy exports.

USDCAD technical outlook.

The intraday technicals are bearish while trading below 1.3530 and looking to extend losses to 1.3460. A break above 1.3530 would negate the intraday downtrend and target 1.3610.

USDCAD tested the November 14 uptrend line in the 1.3460-70 area and it held. A move below 1.3460 suggests further losses to 1.3250, the November 14 low, which guards the long-term uptrend from June 2021, which comes into play at 1.2760.

For today, USDCAD support is at 1.3470 and 1.3450. Resistance is at 1.3530 and 1.3580

Today’s range 1.3470-1.3560.

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

The US dollar consolidated yesterday’s losses in a somewhat quiet overnight session.

The release of the FOMC minutes for the December 14 meeting reminded markets that not only are US interest rates going higher, but there would also not be any rate cuts in 2023. Pivot has been punted.

The minutes noted that officials agreed that inflation was unacceptably high and that it would take substantially more evidence of progress to be confident that inflation was on a downward path.

Risk sentiment soured slightly after the World Health Organization (WHO) and President Biden expressed concerns about the latest coronavirus outbreak in China. Mr Biden said China wasn’t “forthcoming” in providing accurate information and the WHO claimed China is underrepresenting the true impact of the disease.

China is oblivious to the concerns as evidenced by its plan to reopen the Hong Kong border.

Weekly jobless claims surprised with a 19,000 decline from last week while ADP employment rose 235,000 in December compared to the forecast for a 150,000 increase. The news reinforced the Fed’s view for higher interest rates because a tight labour market keeps inflation elevated.

Asia equity traders were non-plussed about the FOMC minutes and turned their attention to modestly better China Service PMI data and China’s reopening plans. Hong Kong’s Hang Seng index closed with a 1.25% gain, while Japan’s Nikkei 225 index rose 0.40%.

European bourses are trading with a mixed tone. The UK FTSE 100 is up 0.44% while the German Dax is unchanged.

S&P 500 futures gave up earlier gains thanks to the jobless claims data and are down 0.46% ahead of the Wall Street open.

EURUSD extended losses from overnight and dropped to 1.0555 from 1.0631 after the US jobless claims data. Prices were also weighed down by the hawkish FOMC minutes although the fall in Euro area energy prices may limit the downside. Traders ignored a slightly better-than-expected German trade report.

GBPUSD traded in a 1.2002-1.2077 band overnight then plunged to 1.1919 after the US ADP and jobless claims data. Rishi Sunak is channelling his inner Maggie Thatcher as he prepares to take on unions in six key areas. The pending legislation is supposedly giving employers the right to sue unions and fire employees. The intraday GBPUSD technicals are bearish below 1.2070.

USDJPY traded in a 131.70-132.89 range then soared to 133.76 after the ADP data. Prices got a bit of a boost after the US 10-year Treasury yield rose from 3.71% to 3.76%.

AUDUSD dropped to 0.06771 from an overnight peak of 0.6844 range due to broad US dollar strength,

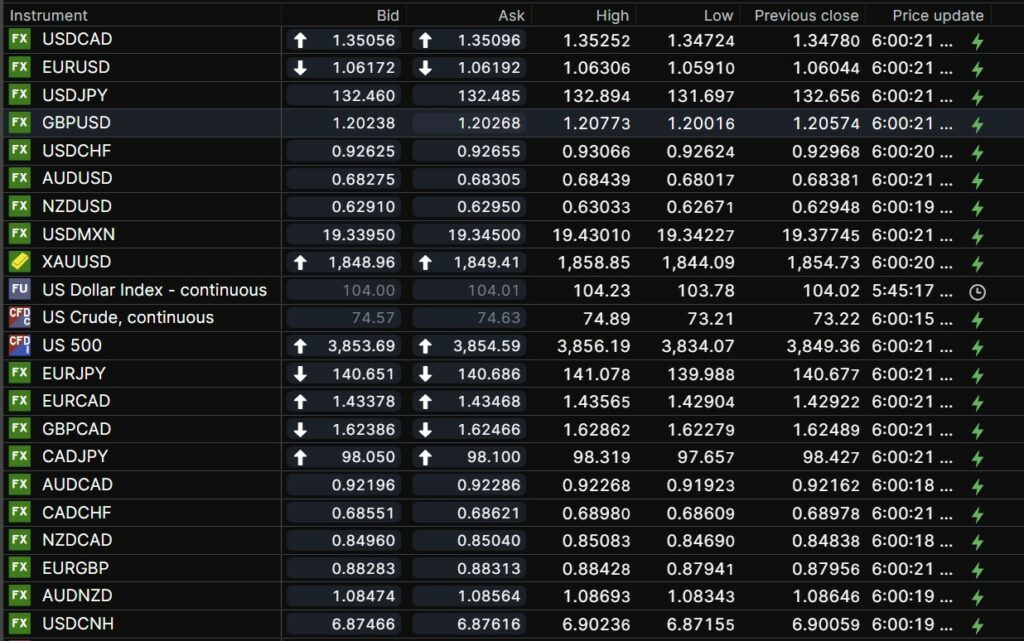

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

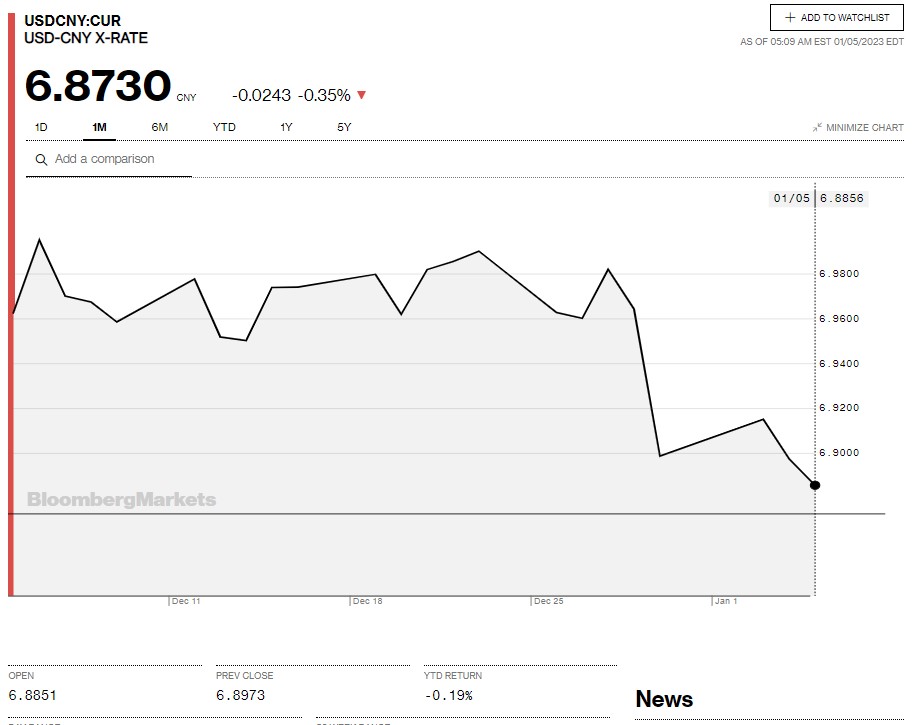

China Snapshot

Today’s Bank of China Fix: 6.8926, previous 6.9131

Shanghai Shenzhen CSI 300 rose 1.94% to 3968.58

Caixin December Services PMI 48 vs forecast 47.5, November 46.7

China announced gradual reopening of Hong Kong border, beginning January 8.

World Health Organization claims China’s “very narrow” definition of Covid-19 deaths are not showing the true scope of the outbreak. China is reporting just five or fewer deaths per day while a UK health data firm, Airfinity, estimates its more like 9,000 deaths /day.

Chart: USDCNY one month

Source: Bloomberg