Photo: Matt Stone/Trey Parker

May 3, 2023

- Oil prices plunge on US recession fears.

- FOMC meeting to reignite terminal rate debate.

- US dollar retreats except against AUD and CAD.

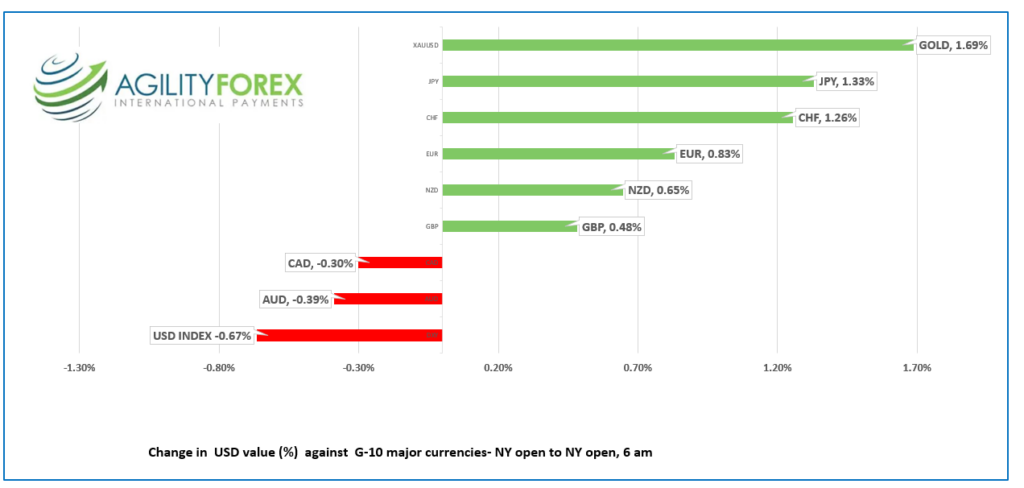

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3621-25, overnight range 1.3605-1.3638, close 1.3626

USDCAD rallied after yesterday’s JOLTS report fueled recession fears, and never looked back. The Bureau of Labor Statistics reported that US job opening fell to 9.6 million as of March 31, a decline of 384,000.

The news spooked oil traders who sold WTI from $75.60/b to $69.25/b in NY today. Fibonacci retracement analysis of the March 20-April 12 range suggests that a move below $68.50 will extend losses to $63.95/b. Traders ignored the API report showing crude inventories declined by 3.9 million barrels last week.

USDCAD is bolstered by the weaker oil prices and US recession fears, with the risk that a more hawkish than expected FOMC outcome underpinning prices.

Today’s US Stronger than expected ADP data, offset the JOLTS report, and soothed recession fears somewhat. However, it raised the risk for more than one additional Fed rate hike, which supports USDCAD.

However, further gains may be limited on speculation that the BoC follows the RBA lead and hikes rates due to stick inflation, at next week’s meeting. The odds of that happening are low, but Governor Tiff Macklem likes to make waves.

USDCAD Technical Outlook

The USDCAD technicals are bullish while prices are above 1.3550 (4 hour chart) looking for a break above 1.3670 to extend gains to 1.3810. A break below 1.3550 would extend losses to 1.3400 today.

The RSI indicator suggests USDCAD is overbought while the Bollinger bands are inconclusive.

For today, USDCAD support is at 1.3590 and 1.3540. Resistance is at 1.3650 and 1.3700

Today’s range 1.3560-1.3660

Chart: USDCAD 1 day

Source: Saxo Bank

G-10 FX recap and outlook

On Monday, JP Morgan Chase CEO Jamie Dimon declared the banking crisis over. Yesterday, investors call “B.S.” and drove regional bank stock prices sharply lower. One of which was PacWest Bancorp, whose shares dropped 28%.

Investors were spooked by rising US recession concerns after the JOLTS job opening survey showed vacancies fell more than expected, suggesting the tight labour market, isn’t so tight anymore and is feeling the bite of rate hikes.

The US bank jitters fueled demand for gold. XAUUSD soared from $1978.75 Tuesday, to $2019.44 overnight, a gain of $40.69 or 2.0%.

Plenty of traders were on the sidelines awaiting the results of today’s FOMC meeting which contributed to the somewhat wide FX ranges.

The ADP employment report muddled the “Fed pausing” rate hike debate. Private sector employment rose 296,000 in April compared to the forecast for an increase of 148,000, but pay gains slowed.

The FOMC is universally expected to raise rates by 25 bps to 5.25% which many analysts believe is the terminal or peak rate. The debate will shift to the timing of the first rate cut. The Fed’s Summary of Projections (SEP) suggested a rate cut was not likely until 2024 while the CME FedWatch tool puts the odds at 75.4% for a rate cut to 5.0% or below, at the September meeting.

European equity markets are posting gains led by a 0.75% rise in the German Dax, S&P 500 futures have risen 0.24%, and WTI oil is down 3.0%.

EURUSD rallied from 1.0999 to 1.1046 in NY, with prices supported by speculation that after today’s 25 bp rate hike, the Fed has reached its terminal rate. Meanwhile the ECB may have another three more rate hikes in the pipeline which will narrow the US interest rate advantage.

GBPUSD traded with a bullish bias in a 1.2469 to 1.2532 overnight, then gave up half of the gains following the JOLTS data.

USDJPY is still under pressure. The currency pair attempted to rally overnight, rising from 135.56 to 136.61, but the move was reversed in Europe and USDJPY dropped to 135.34 in NY after the JOLTS data. USDJPY weighed down by safe-haven demand and falling Treasury yields. The 10-year Treasury yield is 3.40% compared to 3.60% on Monday.

AUDUSD drifted in a 0.6656-0.6676 range. Manufacturing PMI and Trade data did not have any impact on FX.

NZDUSD climbed to 0.6248 in Asia then retreated to 0.6217 in NY after the bump from the robust employment report (Unemployment rate 3.4%, same as last month), faded.

ISM Services PMI is expected at 51.8 (previous 51.2)

Chart of the Day: Gold (weekly)

Source: Saxo Bank

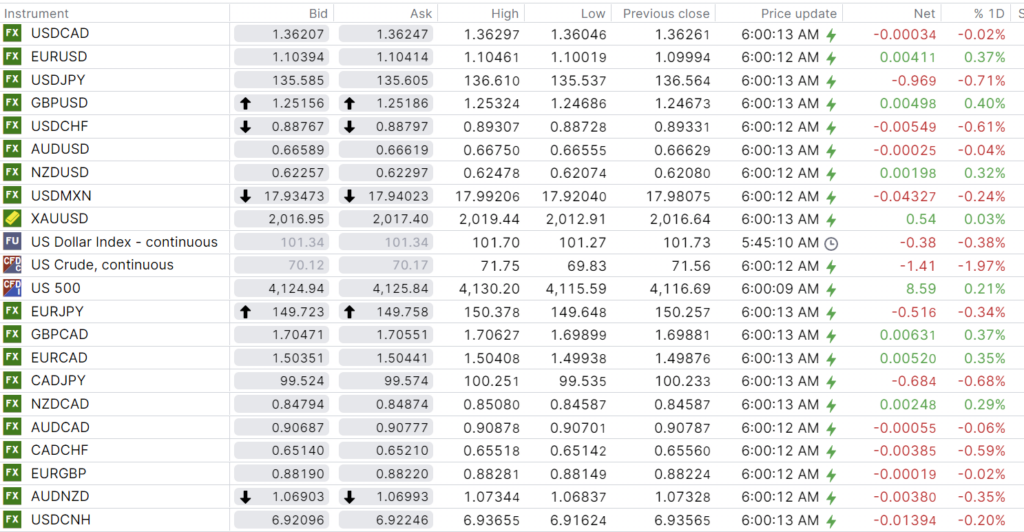

FX open, high, low, previous close as of 6:00 am ET

China Snapshot

Bank of China Fix: 6.9240, closed.

Shanghai Shenzhen CSI 300 closed: 4029.09.

China on National holiday from May 1-3.

Chart: USDCNH 4 hour

Source: Saxo Bank