September 30, 2025

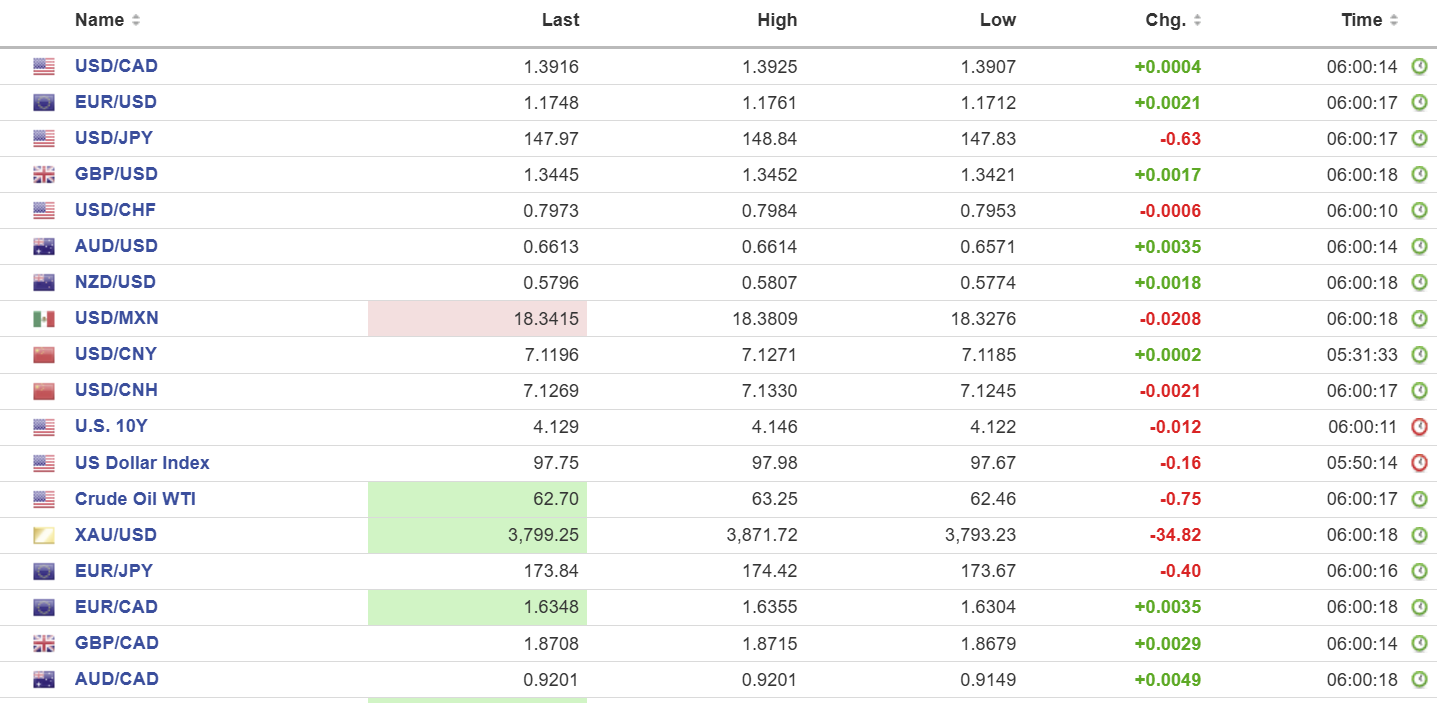

USDCAD open 1.3916, overnight range 1.3907-1.3925, close, 1.3917

USDCAD drifted lower but without conviction due to broad-based US dollar weakness. USDCAD continues to be supported after last week’s comments by Bank of Canada Governor Tiff Macklem, who warned that trade frictions would act as a drag on domestic growth. Canada GDP rose 0.2% m/m in July, but the modest improvement masked underlying weakness mainly due to slower consumer spending.

WTI oil prices fell to 62.46 from 63.45 as ongoing concerns about higher Opec production in November weigh on prices. The cartel is reportedly planning to announce another 137,000 bpd increase for November at its October 5 meeting.

Today is a Federal statutory holiday in Canada for Truth and Reconciliation Day. All federally regulated employees, including government workers and banks, get the day off. But not everyone. Non-federally regulated workers in British Columbia and Manitoba get a day off, but those toiling in Ontario and Quebec do not.

It is month end and quarter end, and the 3.11% MTD gain in the S&P 500 implies that portfolio managers will need to sell USDCAD to balance their portfolios.

The Canadian economic calendar is empty.

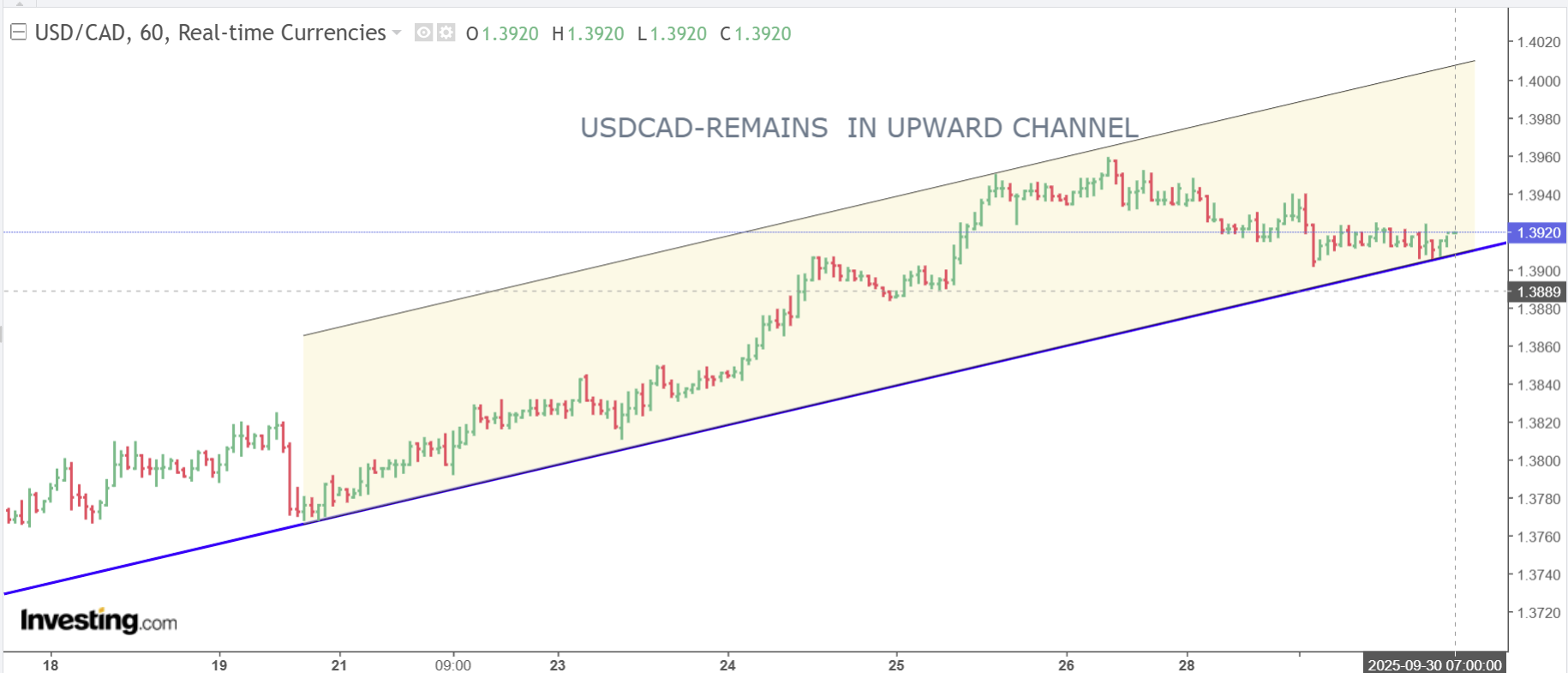

USDCAD Technical Outlook:

The intraday technicals are bullish above 1.3860 and still looking to crack resistance in the 1.3960 area to test the 200-day moving average at 1.3994, which if broken opens up a rally to 1.4110.

The medium-term technicals are bullish, but momentum indicators are not overly bullish.

For today, USDCAD support is 1.3900 and 1.3860. Resistance is 1.3950 and 1.4000. Today’s Range: 1.3870-1.3960.

JOLTS Job Openings on Tap

Traders are awaiting today’s JOLTS Job openings report (forecast 7.1 million vs 7.181 million in July) to provide further evidence that the US employment market is cooling. A result that meets the forecast would mean that the job market, although cooling, remains resilient. The Chicago PMI index and Consumer Confidence data are also on tap.

The data is released against a backdrop of political and geopolitical distractions. Trump and Israeli Prime Minister Netanyahu have agreed to a peace plan, and they told Hamas to get on board or Israel will “finish the job.” Trump slapped a tariff between 10 and 50% on imports of softwood lumber, kitchen cabinets, vanities, and upholstered wood products, effective Oct 14.

Meanwhile, Washington is counting down the hours until the government shuts down (12:01 am October 1). So far, the Democrats have no interest in keeping the government open unless Trump lowers healthcare costs.

Taking Stock

Asian equity indices closed on a mixed note. Japan’s Topix rose 0.19%, Australia’s ASX 200 fell 0.16%, and the Hong Kong Hang Seng index rose by 0.87%.

As of 5:10 am PDT, European equity index direction is undecided. The German DAX is up 0.12% and the UK FTSE 100 index has gained 0.18%, while the French CAC-40 index is down 0.30%. S&P 500 futures have lost 0.18%, U.S. dollar index (DXY) dropped to 97.79 from 97.98, gold (XAUUSD) is 3813.46, and the U.S. 10-year Treasury yield is 4.129%.

EURUSD

EURUSD trickled higher, rising from 1.1712 to 1.1761 before easing back to 1.1746 as NY opened with prices sliding on the back of general US dollar weakness. It’s US employment data week and that data is driving global FX. German retail sales fell 0.2% m/m in August. Forecasters were looking for a 0.6% rise. German unemployment rose by 14,000 to 2.98 million while the unemployment rate stayed at 6.3%. Traders are also hoping for some monetary policy insight from ECB President Christine Lagarde today.

GBPUSD

GBPUSD traded in a 1.3421-1.3452 range with prices getting a bit of a boost from stronger than expected GDP, which rose 1.4% y/y in Q2 (forecast 1.2%). The UK’s charm offensive of wining and dining Trump paid off, with Britain spared from the latest tariff barrage he unveiled yesterday.

USDJPY

USDJPY traded negatively in a 147.83-148.84 band after US government shutdown concerns sparked safe-haven yen buying. The BoJ summary of opinions revealed a hawkish shift with “some” policymakers supporting hiking interest rates in the near term. Japanese retail sales were weaker than expected.

AUDUSD

AUDUSD rallied from 0.6571 to 0.6614 due to broad US dollar strength, improved risk sentiment out of China, and because the RBA left rates unchanged at 3.6%. The RBA decision was expected.

USDMXN

USDMXN traded sideways in a 18.3276-18.3809 range. The downtrend channel from April remains intact and it continues to guide prices lower.

USDCNY

PBoC fix: 7.1055 vs exp. 7.1166 (Prev. 7.1089)

Shanghai Shenzhen CSI 300 rose 0.45% to 4640.69

NBS Manufacturing PMI was 49.8in September (August 49.4) while non-manufacturing PMI was 50.0 compared to 50.3 in August.

RatingDog Manufacturing PMI (former Caixin) was 51.2 in September (August 50.5) while Services PMI was 52.9 compared to 53.0 in August Q4.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics