February 27, 2026

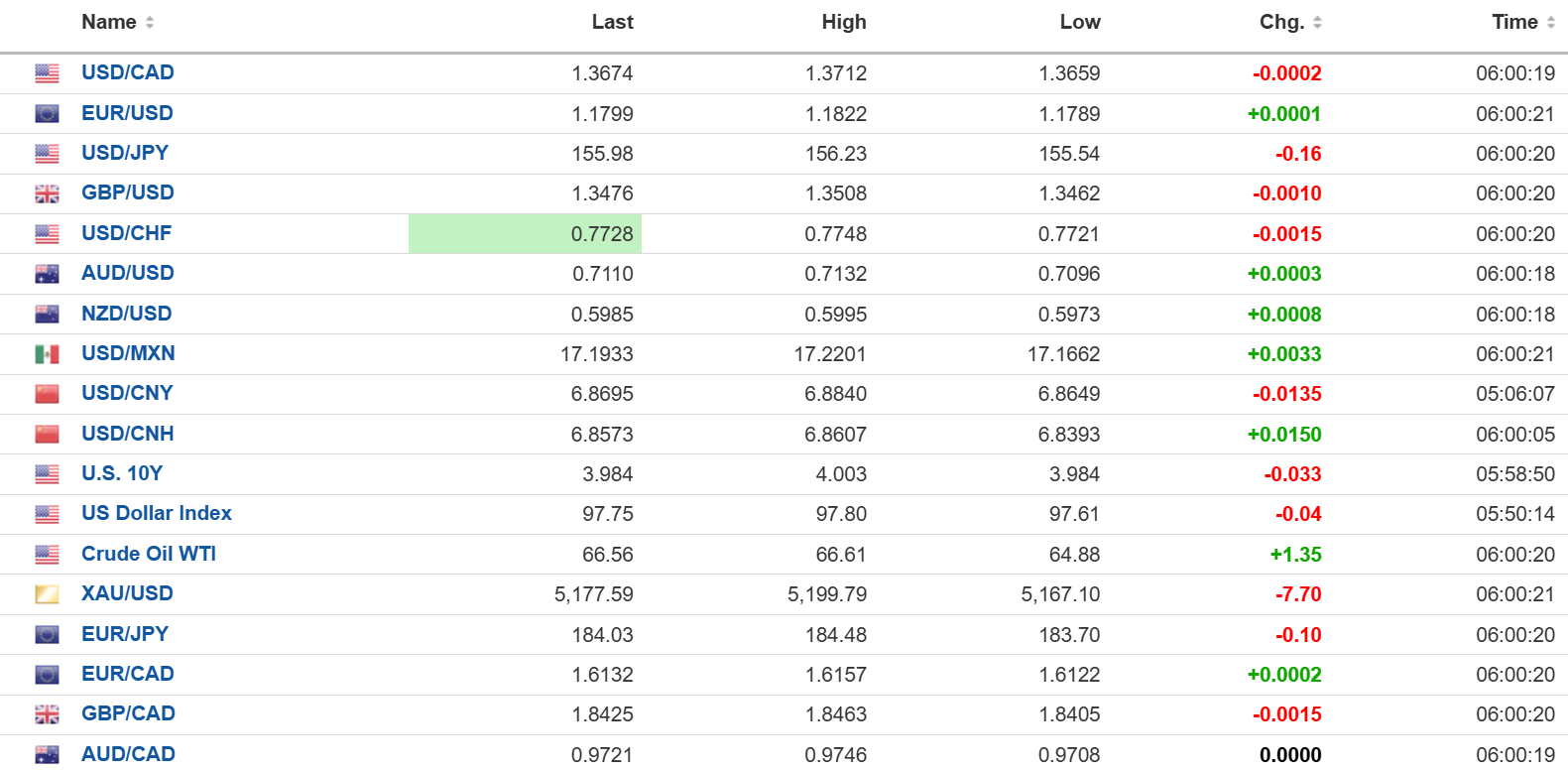

USDCAD open: 1.3674, overnight range 1.3659-1.3712, close 1.3682

USDCAD is on pace to end the week where it started, and today’s release of disappointing Q4 GDP didn’t make any difference. Q4 GDP fell 0.6% q/q (forecast 0% y/y), and sharply lower to Q3’s 2.6% result. The weakness wasn’t really a surprise, but it does add another layer of support to USDCAD downside.

Prime Minister Carney is in India trying to mend fences and boost trade. Dinesh Patnaik, High Commissioner to Canada, told CBC News yesterday, “On energy, there is an appetite which even Canada cannot fulfill, and we are willing to buy whatever Canada is offering on crude, on LPG, on LNG.” Hmmm, if only Canada had another pipeline to the West Coast.

WTI oil is at the top of its 64.88-67.65 range after US and Iran indirect talks, with both parties in separate rooms, in Geneva concluded without a deal. Polymarket odds that the US attacks Iran are around 37% for next week and 63% by the end of March.

USDCAD Technical Outlook

The intraday USDCAD technicals are unchanged. Prices are rangebound in a 1.3630-1.3730 band and are mildly above 1.3650. A topside break targets 1.3780 while a downside move puts 1.3610 in play.

The medium-term technicals are bearish below 1.3755-1.3800, leaving prices trapped inside a broad 1.3480-1.3780 band. A break below 1.3585 would reopen downside risk toward 1.3500 and 1.3400, while a sustained break above 1.3800 would argue for a move toward 1.3900.

For today, USDCAD support is at 1.3660 and 1.3630. Resistance is at 1.3710 and 1.3730.

Today’s Range: 1.3650-1.3720

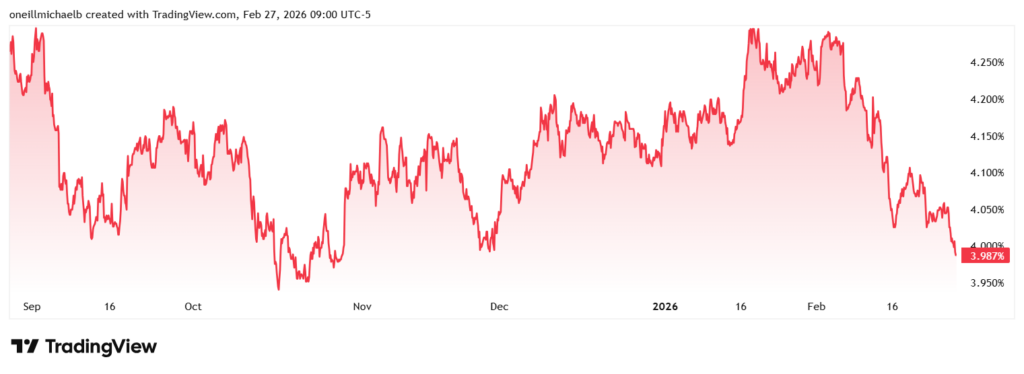

Treasuries are Still a Haven

The 10-year Treasury yield chart says it all. America is still the preferred destination when geopolitics get nasty. The US and Iran nuclear talks have ended for this week but at (very rough estimate) around $50 million/day to keep the US strike force deployed, Trump may lose patience.

That’s just one event driving Treasury demand. The lingering fallout from the Russia/Ukraine war, Pakistan announcing it is “open war” with Afghanistan, the uncertainty around tariffs after the US Supreme Court ruled IEEPA tariffs were illegal, and the Fed/Justice Department issue are also weighing on yields.

US Prices Rising

A stronger than expected January PPI report served to justify the Fed’s unchanged rates policy. PPI rose 0.5% in January (forecast 0.3) but Decembers was revised down a tick to 0.4%. Core-PPI prices jumped 3.6% y/y compared to expectations for a 3.0% y/y increase and 3.3% in December. The greenback wobble on the news but S&P futures dropped.

Taking Stock

Asian equity markets closed higher. Japan’s Topix rose 1.5% to finish February with an impressive 11.38% gain. Australia’s ASX gained 0.25% and finished February with a gain of 2.57%. The Hong Kong Hang Seng rose 0.85% but finished the month with a 2.54% loss.

As of 5:40 am, PT, European bourses are all negative except for the UK FTSE 100 which is up 0.23%. The French CAC-40 is down 0.58% and the German DAX has lost 0.22%. S&P 500 futures are down 0.94% while the DXY is 97.83. The 10-year Treasury yield is 3.984%, and gold (XAUUSD) is 5,216.27.

EURUSD

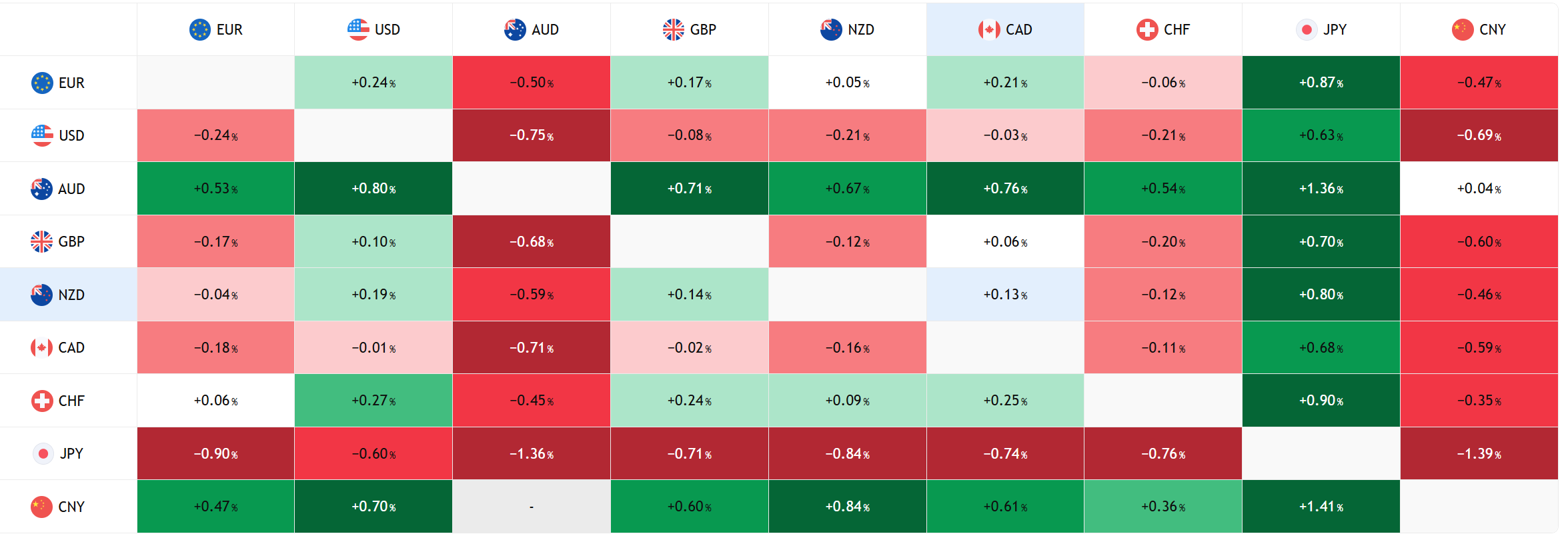

EURUSD chopped higher in a 1.1789-1.1822 range and is in the middle of that band in NY. There were a slew of inflation reports across German regions, and Germany’s unemployment rate was unchanged at 6.3%. The data was ignored. For now, EURUSD will consolidate in a 1.1760-1.1860 band.

GBPUSD

GBPUSD dropped from 1.3508 to 1.3462 after the ruling UK Labour Party finished in third place in a by-election. The Green Party won the seat that Labour had held for almost 100 years, raising questions about Prime Minister Starmer’s longevity. Weaker than expected GfK consumer confidence data, actual -19 vs -16 in January, did not help sentiment.

USDJPY

USDJPY bounced around in a 155.54-156.23 range. Tokyo inflation rose 1.8% y/y, a tick higher than forecast but below the 2.0% reported previously. Japan’s retail sales surged in January, rising 1.8% y/y compared to the consensus forecast for a 0.4% decline. Even so, prices are torn between talk of rate hikes and anticipated government stimulus.

AUDUSD

AUDUSD traded in a 0.7096-0.7132 range and is poised to end February with a 1.42% gain against the US dollar. The key driver was higher inflation numbers that reopened the door to further RBA tightening.

USDMXN

USDMXN consolidated yesterday’s losses in a 17.1662-17.2201 range. USDMXN gains are capped by the recent US IEEPA tariff ruling and US and Mexico interest rate differentials.

China

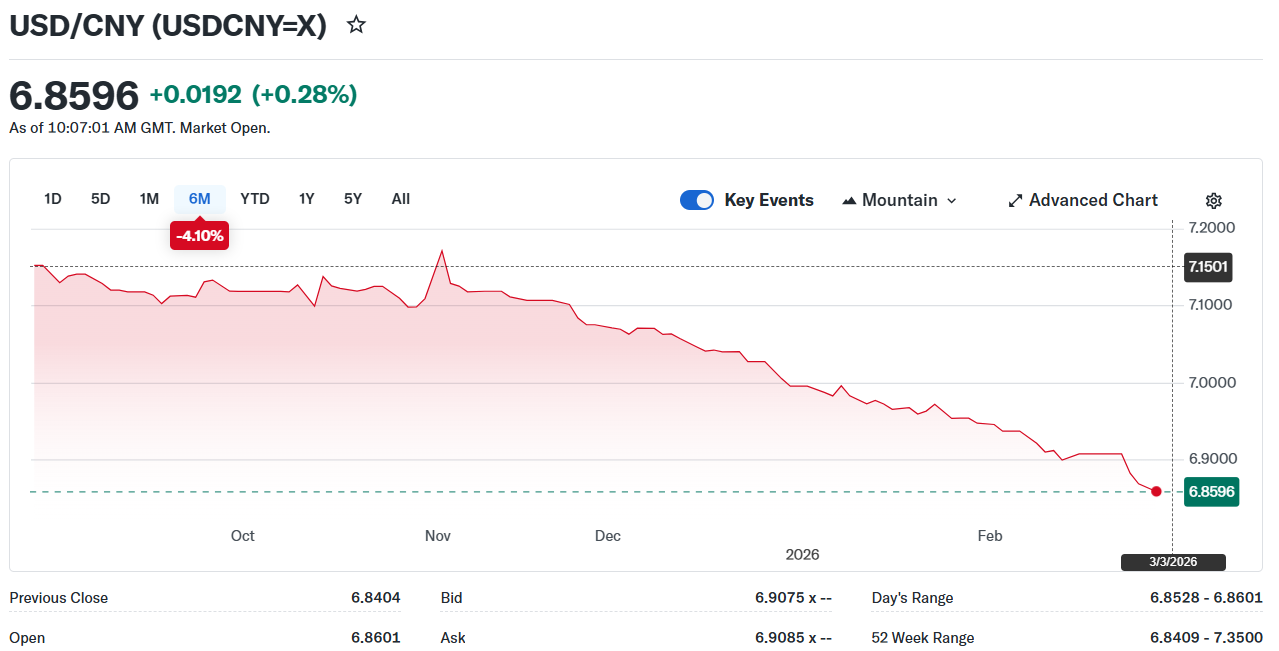

USDCNY Fix: 6.9228 vs exp. 6.8428 (Prev. 6.9228

Shanghai Shenzhen CSI 300 fell 0.34% to 4,710.35

PBoC cuts reserve ratio for forward FX sales to 0% from 20% in a move designed to encourage US dollar buying. Officials would like to see the pace of yuan strength slow.

FX open high low

FX Heat Map (6:00 am) one week

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview