March 10, 2026

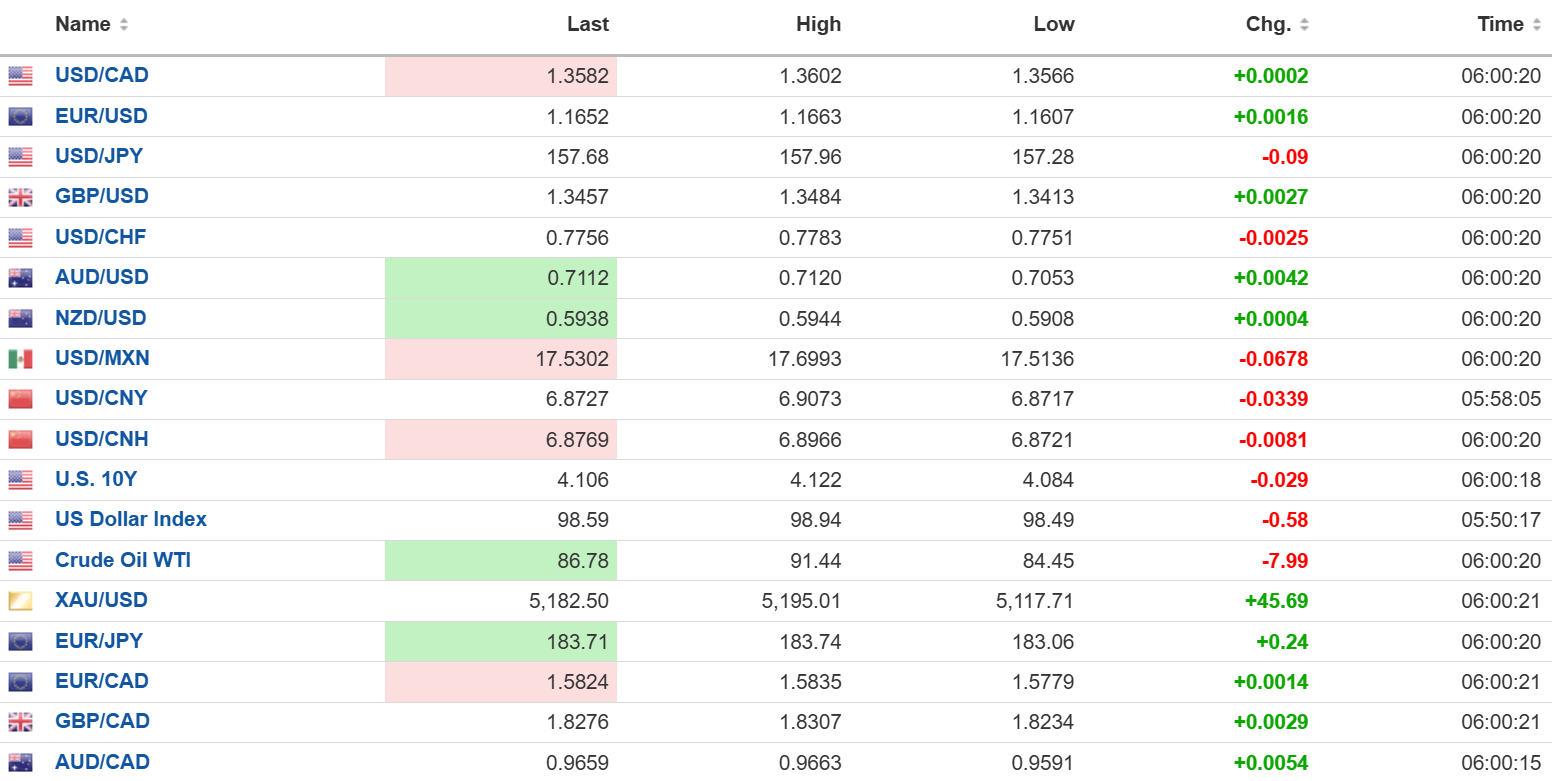

USDCAD open: 1.3582, overnight range 1.3550-1.3602, close 1.3588

The Canadian dollar traded inversely to the other G-7 majors because of its status as a petrocurrency (at least for the time being). Yesterday, USDCAD hit 1.3526, then rallied to 1.3610 as oil prices fell and that correlation continued overnight.

The currency did not get any benefit from broad-based US dollar selling pressure after Trump’s comment the war in Iran would end sooner than expected, caused oil prices to plunge from yesterday’s peak of116.24/b to 87.35 in NY today.

And… the war is just a week old. News of Trump’s attack on Iran drove oil prices in the Toronto area from $1.29 /litre to $1.55/litre. Yet not one ounce of any oil company fuel inventory was impacted by the spike in spot crude. Hmm.

Canada and the US open trade negotiations in May with the fate of the USMCA trade agreement on the line.

The are no Canadian economic reports released today, and the only US data of note is Existing Home Sales.

USDCAD Technical Outlook

The intraday USDCAD technicals (4-hour chart) are bearish while trading below 1.3620 and looking to test support at 1.3520. Momentum indicators remain weak with RSI indicating downside pressure. A break below 1.3510 would expose 1.3470, while a move above 1.3620 would ease the immediate pressure and extend gains toward 1.3660.

The medium-term technicals are bearish as USDCAD below the 1.3800–1.3830 zone, which contains the 100-day and 200-day moving averages on the daily chart. The daily RSI around 31 confirms downside momentum but also suggests the pair is nearing oversold conditions.

For today, USDCAD support is at 1.3510 and 1.3470. Resistance is at 1.3590 and 1.3620.

Today’s Range: 1.3510-1.3590

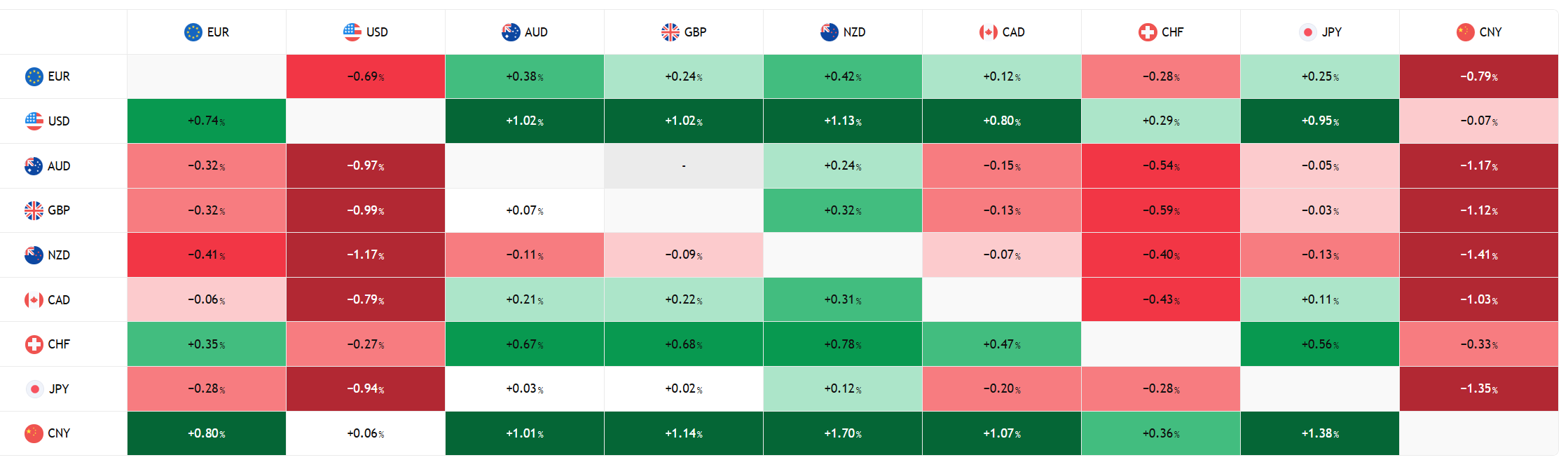

FX Heat Map (6:00 am) one week

FX open high low 6:00 am

Overnight Round-up

It’s all about oil, Iran, and Trump. The US dollar index (DXY) erased yesterday’s gains and traded negatively in a 98.49-98.94 range but has bounced to 98.59 in early NY trading.

Trump claimed the war in Iran “could end soon” and oil prices hit the skids. Then he kind of contradicted himself when he said he would hit Iran “20 times harder if they stop the flow of oil through the Strait of Hormuz.”

Supreme Leader Ayatollah Mojtaba Khamenei (ticket to the afterlife in hand) was not bothered. He said not a litre of oil will flow through the Strait if the attacks continue. Surprisingly, oil traders dismissed his comments although neither of these guys should be believed. And as it stands now, the Strait remains effectively closed.

Trump received advice from Putin on how to end the war and unsurprisingly the advice recommended reducing or ending sanctions on Russian oil exports.

The spike in oil prices and Trump’s already low approval ratings among voters has Trump advisors looking into how they could reduce Russian oil sanctions. In addition, the G-7 discussed tapping strategic reserves to alleviate oil shortages but decided to wait.

Taking Stock

Asian equity markets rebounded in reaction to Trump’s comments about the war being almost over. Japan’s Topix climbed 2.47%, Australia’s ASX 200 gained 1.28% and the Hong Kong Hang Seng rallied 2.17%.

As of 5:35 am PT, European bourses are in recovery mode. The German DAX is up 1.88%, the French CAC 40 has gained 1.22%, and the UK FTSE 100 has risen 1.32%. S&P 500 futures are down 0.40%, the 10-year Treasury yield is 4.126% and gold (XAUUSD) is 5,181.50.

EURUSD

EURUSD traded in a 1.1607-1.1663 range with the gains fueled by the drop in crude oil prices. News that Germany’s trade surplus widened to €21.2 b in January from €17.4 b in December was ignored, as was the drop in exports. The Euro area economic calendar did not have any actionable top-tier data.

GBPUSD

GBPUSD rose from 1.3413 to 1.3484 on optimism that Trump’s war on Iran would end earlier than expected, which also raises questions about the sustainability of the rally. The “TACO” trade became a thing because of Trump’s penchant for contradicting himself or just flip-flopping on policies. BRC Like-for-Like Retail Sales rose just 0.7% y/y in February (forecast 2.4%, January 2.3%). The disappointing result was blamed on “grey, wet weather.”

USDJPY

USDJPY dropped to 157.28 from 157.96, then bounced to 157.73 in early NY trade. Q4 2025 GDP rose 1.3% y/y compared to 0.2% previously, fueled by strong corporate capital expenditure and private consumption.

AUDUSD

AUDUSD is near the top of its 0.7053-0.7125 range in early NY trading. Improved global risk sentiment and the risk of higher RBA rates fueled the rally. The NAB Business Conditions index was unchanged at 7 in February while the Business Confidence index fell to -1 from 4.

USDMXN

USDMXN is near the middle of its 17.5136-17.6993 range in early NY trading. The sell-off was because of broad US dollar weakness after Trump suggested the Iran war would end earlier than expected. Yesterday, Mexican Core inflation rose 0.46% in Feb compared to 0.6% previously which gives Banxico room to ease monetary policy.

China

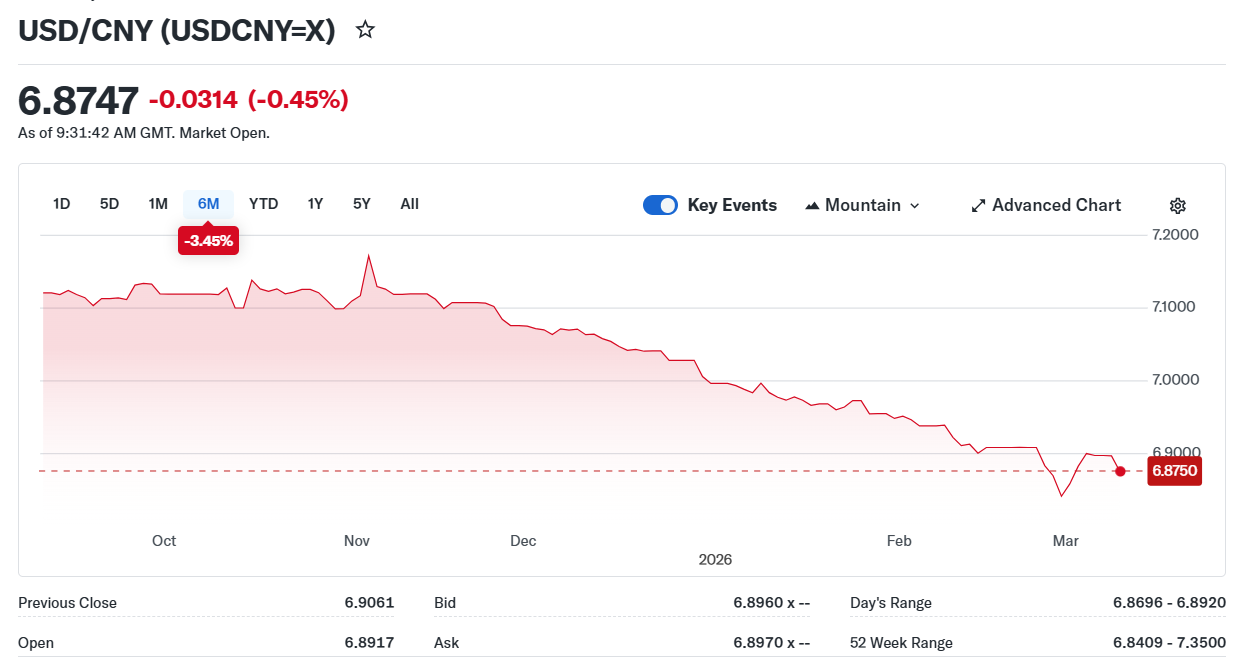

USDCNY Fix: 6.8982 vs exp. 6.8891 (Prev. 6.9158)

Shanghai Shenzhen CSI 300 rose 1.28% to 4,674.76

China’s trade surplus widens sharply to $213.62b in February, compared to $114.11b previously. Exports surged by 21.9%, due to electronics and textiles, and clothing while imports rose 19.8% compared to 5.7%.

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview