October 1, 2025

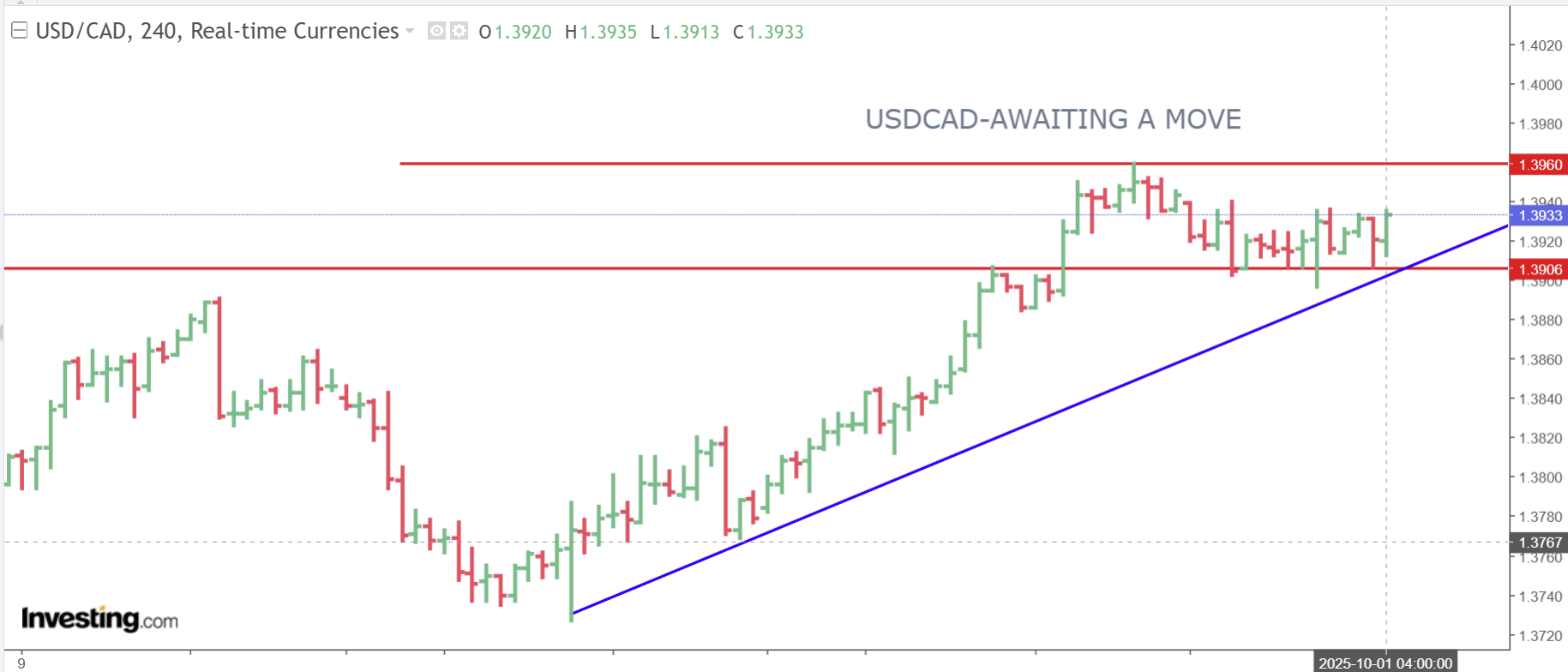

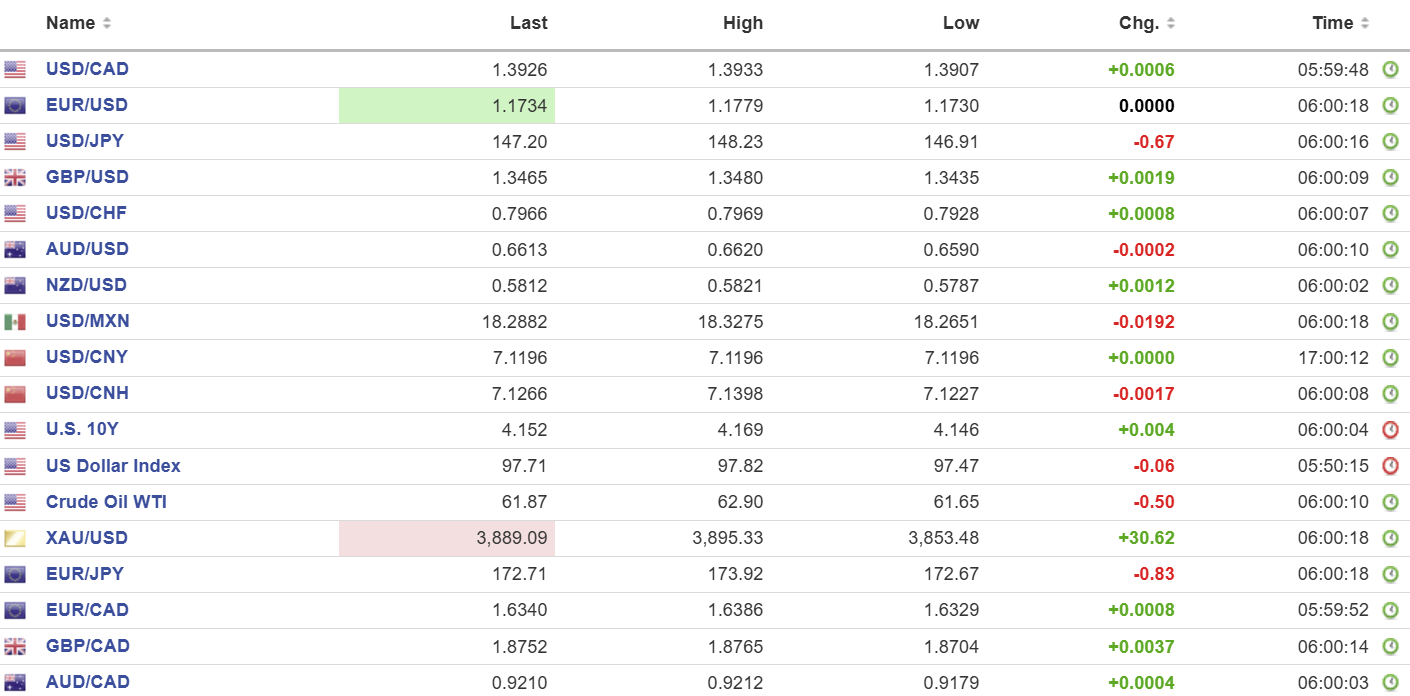

USDCAD open 1.3926, overnight range 1.3907-1.3933, close, 1.3921

USDCAD is trading defiantly in the face of general US dollar selling pressures vs the major G-10 currencies. That’s probably because although the Canadian economy has avoided a recession (for now), the employment market remains very weak, retail sales are soft and the out-put gap is widening pointing for the need for additional Bank of Canada rate cuts.

The BoC Summary of Deliberations from the September 17 meeting are released today and they will reiterate the economic weakness which necessitated the latest rate cut.

WTI oil prices dropped to 61.65 from 62.90 after rumours of a 500,000/bpd production increase that would begin in November were firmly denied by Opec. Prices were further supported by the API news that US crude inventories fell by 3.67 million barrels last week. Nevertheless, the downtrend is intact.

US ISM manufacturing PMI data is due.

USDCAD Technical Outlook:

The intraday technicals remain bullish above 1.3870 and the support zone in the 1.3850-60 area. Overbought momentum indicators are thwarting gains above the 1.3950-60 resistance zone, with additional resistance form the 200-day moving average lurking at 1.3991.

The medium-term technicals are cautiously bearish while prices are below the 1.4000 zone. A topside break targets 1.4130 then 1.4270.

For today, USDCAD support is 1.3900 and 1.3860. Resistance is 1.3950 and 1.4000. Today’s Range: 1.3870-1.3960.

Government Closed

The US government shut down because the Republicans and Democrats could not agree to a funding deal. Federal services will begin closing and hundreds of thousands of government employees are furloughed. For the most part, being furloughed is like getting a paid vacation except there are no paychecks during the shutdown—the wages are paid retroactively when the government reopens.

For markets, the US shutdown means that key government economic reports like weekly jobless claims and nonfarm payrolls will be unavailable.

For the most part, financial markets have ignored the news. The US dollar is modestly lower. The 10-year Treasury yield is unchanged while gold prices surged. S&P 500 futures have retreated.

Taking Stock

Asian equity indices closed lower while Chinese equity markets were closed for Golden Week holidays. Japan’s Topix fell by 1.37%, partially due to a mixed Tankan report, and Australia’s ASX 200 was flat.

As of 7:40 am PDT, European equities are higher led by the UK FTSE 100 index which has climbed 0.64%. The German DAX has risen 0.29%, and the French CAC-40 index is up 0.37%. S&P 500 futures have lost 0.45%, U.S. dollar index (DXY) is 97.52, gold (XAUUSD) surged to 3876.59, and the U.S. 10-year Treasury yield dropped to 4.101 from 4.169%. in Asia.

EURUSD

EURUSD traded in a 1.1730-1.1779 range but retreated from the peak to 1.1740 in early NY trading. Yesterday’s comments by ECB President Christine Lagarde didn’t do anything to suggest rate cuts were on the horizon. Instead, she said “the risks to inflation appear quite contained in both directions.” Today’s release of harmonized CPI for September, which rose to 2.2% y/y from 2.2%, was expected and due to higher energy costs. The short-term EURUSD technicals are bullish above 1.1650.

GBPUSD

GBPUSD caught a small bid and rose from 1.3435 to 1.3480 with traders dismissing news that Manufacturing PMI fell to a 5-month low of 46.2. S&P wrote, “Manufacturers are facing an increasingly challenging environment, with intakes of new business and levels of production hit by weak market sentiment, a dearth of new export work and a high-cost environment exacerbated by tax and labour cost rises.” GBPUSD is getting support from the FTSE 100 index hitting another intraday record high.

USDJPY

USDJPY retreated from 148.23 to 146.91 before bouncing to 147.21 in NY. Broad-based US dollar weakness and hawkish BoJ expectations along with a side of yen safe-haven demand due to the US government shutdown weighed on the pair. USDJPY was also undermined after the quarterly Tankan survey improved for the second time in a row. It suggests that the economy is shrugging off trade tensions, which is more ammunition for the BoJ to justify a rate hike.

AUDUSD

AUDUSD bounced in a 0.6590-0.6620 range with prices supported by general US dollar weakness following the US government shutdown. Australia’s September PMI index was 51.4 which showed manufacturing production expanding but at a slower pace than last month.

USDMXN

USDMXN traded lower in a 18.2651-18.3275 range as it continues to give back last week’s gains. Traders have embraced Banxico’s gradual and cautious approach to monetary policy which is weighing on prices. The latest bout of US dollar weakness is icing on the cake.

USDCNY

CLOSED FOR GOLDEN WEEK

PBoC fix: 7.1055 vs exp. 7.1166 (Prev. 7.1089)-CLOSED

Shanghai Shenzhen CSI 300 rose 0.45% to 4640.69-CLOSED

China’s golden week holidays start today with its National Day holiday.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics