April 1, 2026

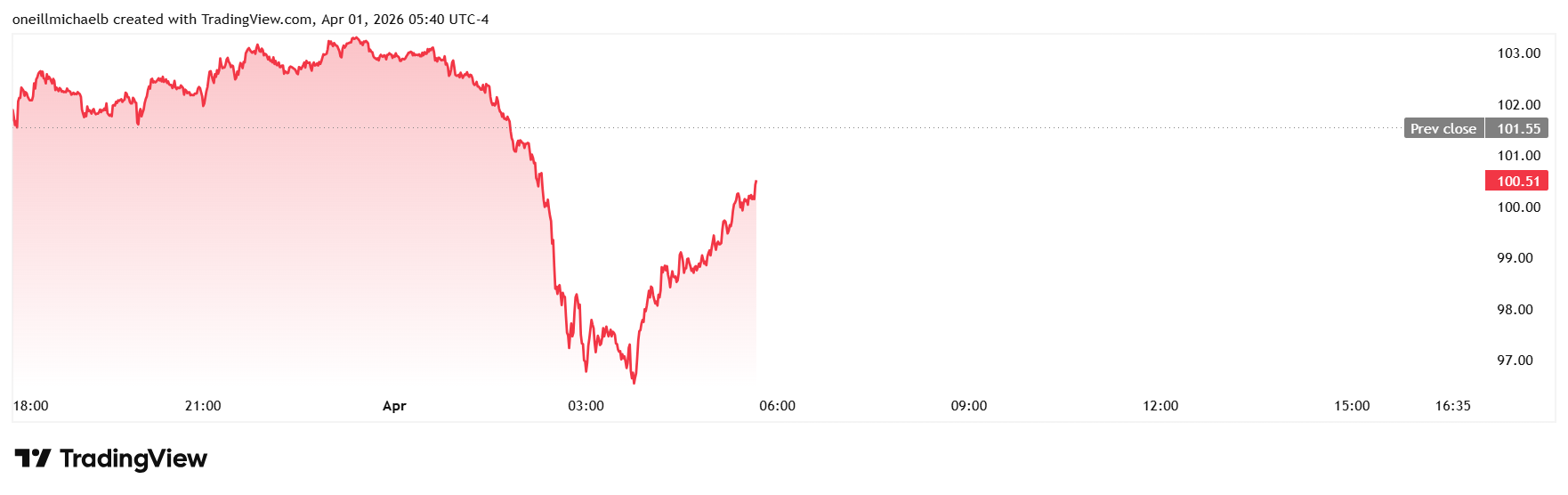

USDCAD open: 1.3889, overnight range 1.3887-1.3920, close 1.3916

USDCAD dropped 0.12% overnight on soaring optimism for an early end to Trump’s war in Iran, after the President said the war would be over in “two or three weeks.” Markets are taking him at his word, which history has proved, is never a good idea.

Trump is reportedly planning to address the nation at 9:00 pm to explain why America’s fiasco in Iran is Biden’s fault.

Some economists are impressed with Canada’s better than expected GDP growth of 0.1% in January and the flash estimate for February at 0.2%. Before popping the champagne, consider that GDP is only up 0.6% y/y and that is before Trump’s Iran war.

WTI oil prices dropped from yesterday’s peak of 106.82 to 96.51 overnight before rising to 100.44 in NY trading. That’s because Iran kept up its missile and drone attacks at Israel, Bahrain, and Kuwait and the Strait of Hormuz is still closed.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish above 1.3860, but momentum has clearly cooled after tagging the upper Bollinger Band near 1.3950–1.3965. The sharp drop in the 4-hour RSI from overbought to the low 30s suggests a positioning flush rather than a trend reversal. A break above 1.3965 targets 1.4000, while a move below 1.3860 targets 1.3810.

The medium-term USDCAD technicals are bullish above 1.3810, where the 100-day and 200-day moving averages converge However, the daily RSI is still-elevated which indicate the market is extended, but not exhausted.

For today, USDCAD support is at 1.3860 and 1.3810. Resistance is at 1.3920 and 1.3960.

Todays range 1.3840-1.3940.

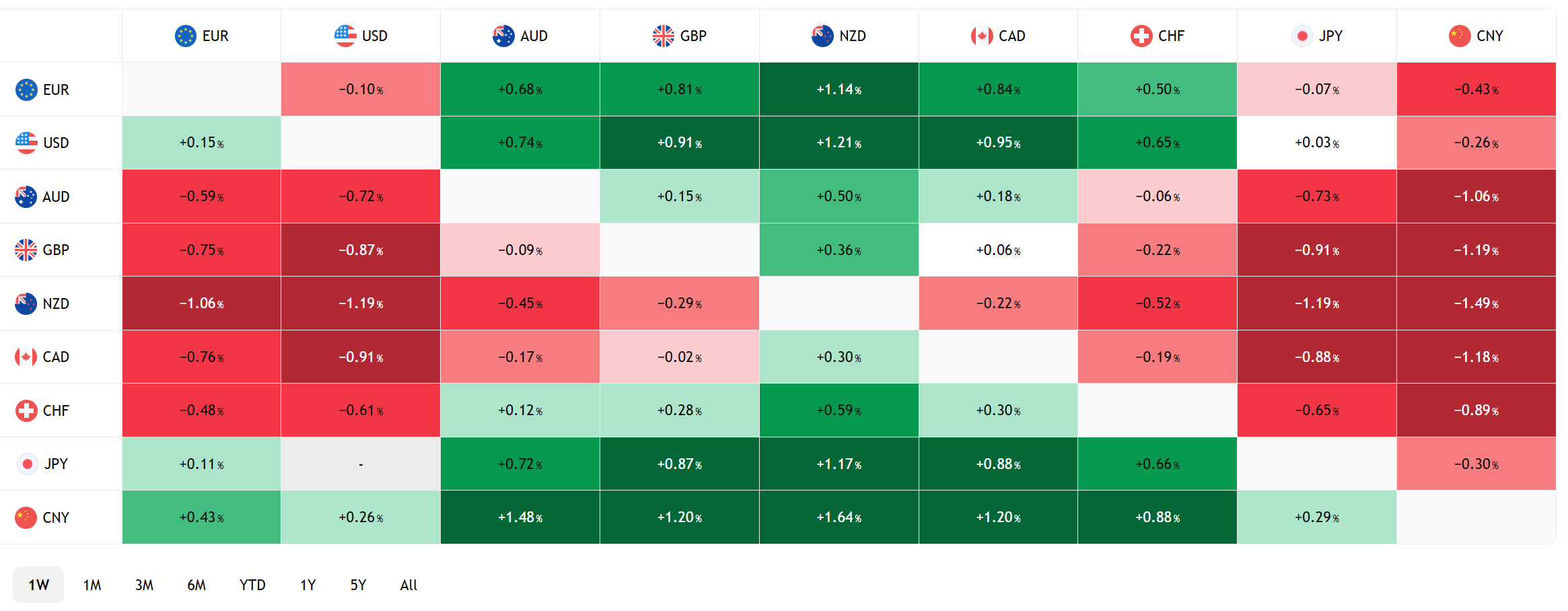

FX Heat Map (6:00 am) one week

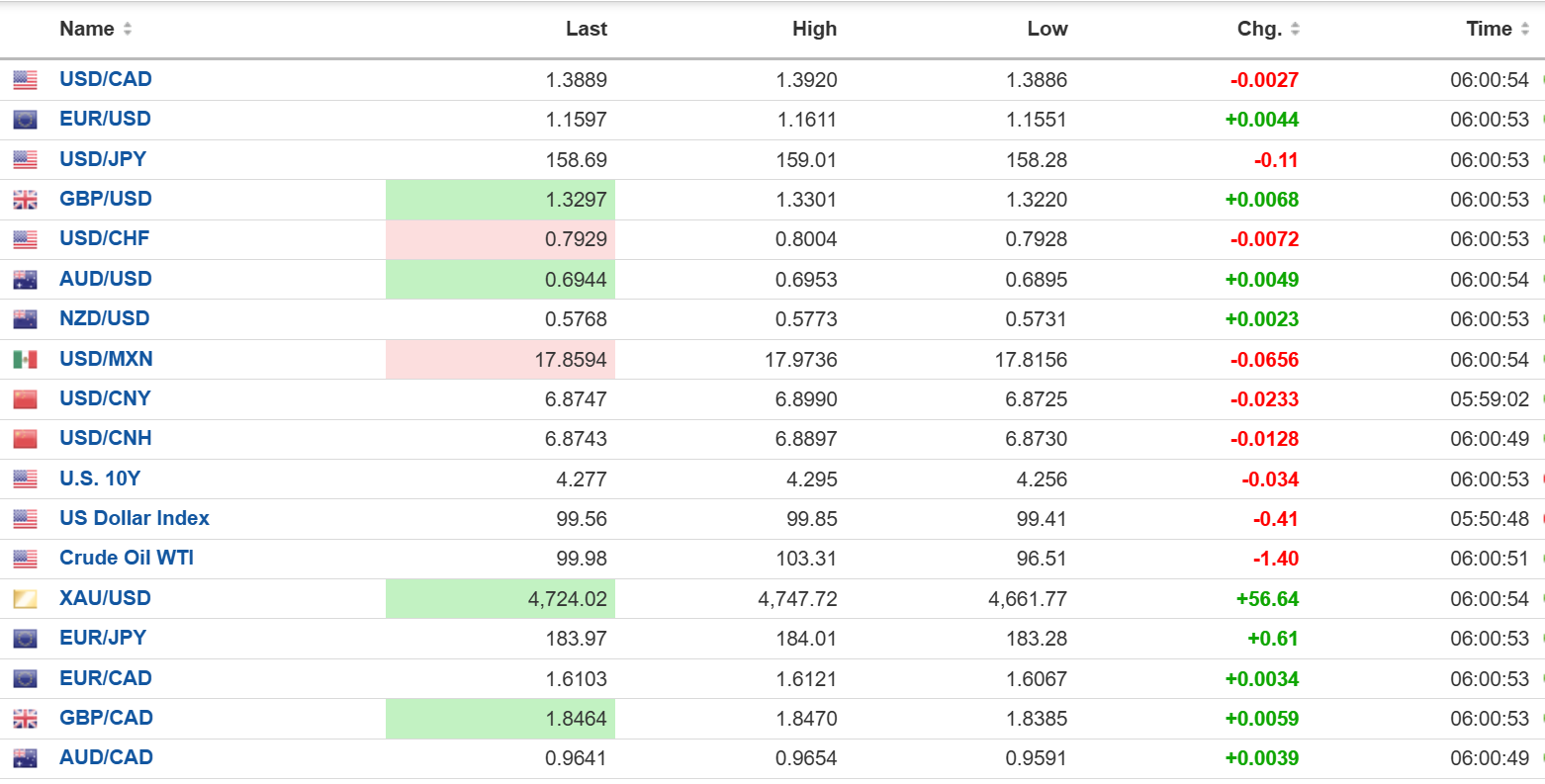

FX open high low 6:00 am

Data and War News in Competition

Global markets have traded like a yo-yo in a hurricane with every headline about Trumps war in Iran. Today, a slew of economic data will vie for dominance on the resurgence of the US economic growth outlook for market direction.

Treasury yields slid from the peak after traders determined that the risk of an economic slowdown and rising unemployment was more important to the Fed than a temporary inflation spike from the oil shock. That view was questioned this morning after ADP reported the US added 62,000 jobs in March and February’s numbers were revised up to 66,000 from 63,000.

US Retail Sales topped forecasts, rising 0.5% m/m (forecast 0.3%, January 0%) Still to come: ISM Manufacturing PMI is expected at 52.5 (previous 52.4) and Business inventories are forecast to be unchanged at 0.1%. 10-year Treasury yields ticked up to 4.291 from 4.276 on the news.

Taking Stock

Asian equities rallied on the heels of the Wall Street rally yesterday and closed sharply higher. Japan’s Topix soared 4.95%. The Hong Kong Hang Seng climbed 2.04%, and Australia’s ASX rose 2.24%.

As of 5:30 am PT, European markets are rising. The German Dax is up 2.61%, the UK FTSE 100 has gained 1.89% and the French CAC 40 is up 1.97%. S&P 500 futures have risen by 0.69%, the 10-year Treasury yield is 4.307%, the DXY is 99.48, and Gold (XAUUSD) is 4748.92.

EURUSD

EURUSD extended yesterday’s rally in a 1.1551-1.1611 range overnight. Optimism for the war in Iran ending soon, ongoing hopes that the Fed is still in easing mode and ECB rate hike concerns from higher inflation are weighing on prices. German and Eurozone Manufacturing PMI rose in March.The short-term technicals target 1.1800 if EURUSD can remain above 1.1560.

GBPUSD

GBPUSD traded in a 1.3220-1.3314 range and is at the top of the band in NY, with gains underpinned by broad US dollar weakness. UK Manufacturing PMI fell to 51.0 from 51.4, due to uncertainty around the Iran war, but the news was ignored. GBPUSD gains may be limited due to renewed expectations for BoE rate cuts. The short term technicals are bearish below 1.3410.

USDJPY

USDJPY traded erratically but lower in a 158.28-159.01 range, before prices bounced to 158.61 in NY. A slew of largely positive economic data competed with still elevated oil prices to determine direction. The Tankan report showed an improved business tone tempered by fears of worsening business conditions due to high oil prices.

AUDUSD

AUDUSD extended yesterdays gains, climbing from 0.6895 to 0.6953 due wide-spread US dollar selling pressures on hopes for an end to Trump’s war. Traders ignored the drop in Manufacturing PMI to 49.8 from 51.0 in February as it was mainly due to the Iran war. The rally is merely a correction while prices are below 0.7010.

USDMXN

USDMXN traded negatively in a 17.8156-17.9736 range and the outlook is bearish while trading below 18.0120.

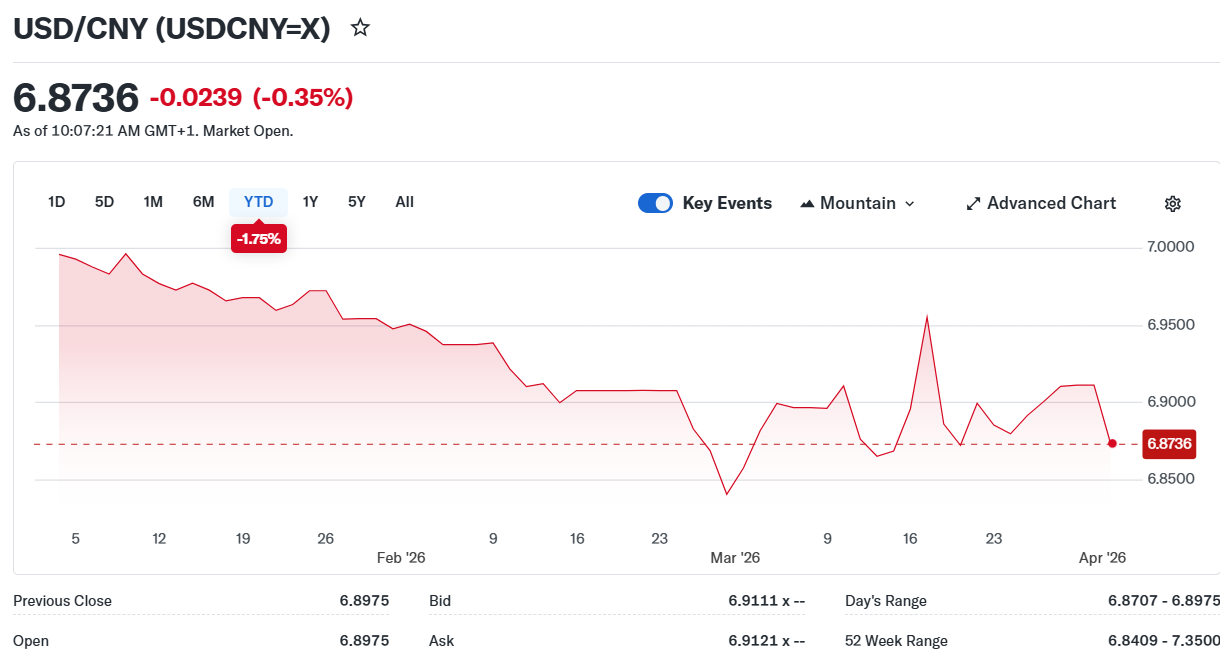

China

USDCNY Fix: 6.9025 vs exp. 6.8858 (Prev. 6.9194)

Shanghai Shenzhen CSI 300 rose 1.71% to 4,526.01

RatingDog Manufacturing PMI rose 50.8 in March, down from 52.1 in February. RatingDog Founder Yao Yu wrote: “Overall, the manufacturing sector sustained a moderate expansion in March, the macro environment presents a more complex picture for the manufacturing sector.”

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview