June 18, 2026

USDCAD open: 1.4125, overnight range 1.4095-1.4134, close 1.4101

USDCAD spiked from 1.4027, pre-FOMC, to 1.4133 in early NY trading today thanks to speculation that the Fed will raise rates in September and the slide in oil prices.

Traders and analysts consider yesterday’s FOMC meeting ended with a hawkish bias due to increased inflation forecasts and dot-plot projections suggesting higher rates. They are ignoring Fed Chair Warsh’s disdain for the SEP and his decision to not submit a dot-plot projection.

The greenback has also caught a bit of a bid after Trump and Iran signed the ceasefire (Peace?) agreement which refocused traders from safe-haven demand for dollars to US economic outperformance demand for dollars.

WTI oil prices traded with a negative bias in a 74.16-76.42 range. Losses were curbed due to Wednesday’s EIA data showing US crude stocks fell by 8.262 million barrels, more than expected. However, Reuters is reporting that three Saudi-flagged supertankers have sailed through the Strait of Hormuz.

Today’s Industrial Product Price index rose 1.2% in May (forecast 1.8%) while the Raw Materials Price Index rose 0.7% compared to 2.6% in April

US releases weekly jobless claims fell by 4,000 to 226,000 and the Philly Fed manufacturing survey ticked up to 10.3 from -0.4 in May.

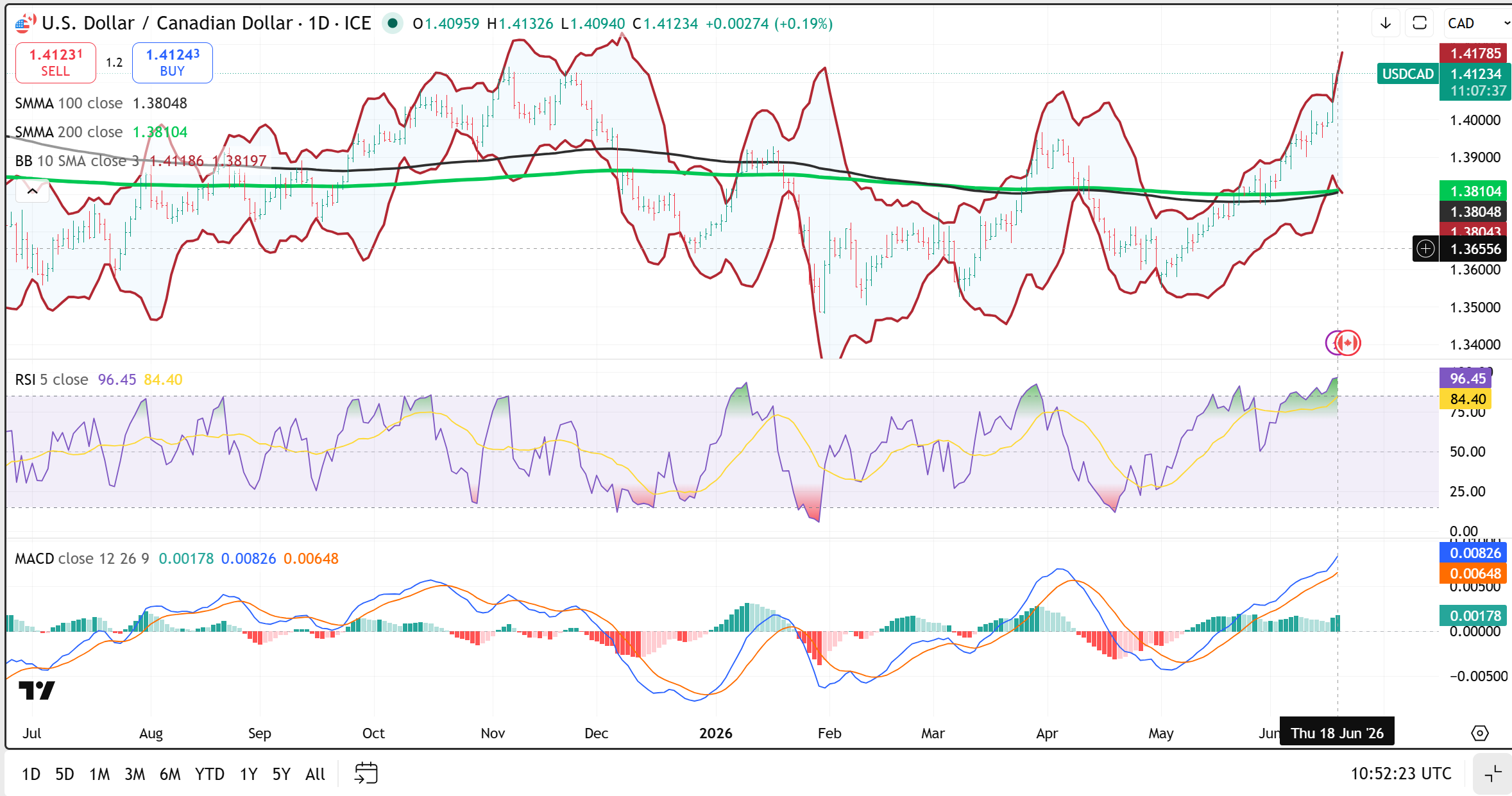

USDCAD Technical Outlook

The intraday technicals are bullish above 1.4095 after USDCAD broke out of the 1.4020 to 1.4095 consolidation zone and pushed to a fresh high near 1.4133. The 4-hour RSI and the daily RSI are signalling that the breakout is powerful but badly overstretched, which suggests a drop into the consolidation zone of 1.4020-1.4095.

Longer term, USDCAD is bullish above 1.3810, the 200-day moving average, with the ascending channel from the May low still firmly intact. The daily RSI, however, is once again extremely overbought, its most stretched reading of the run and warning that a corrective pullback is overdue.

For today: USDCAD support is at 1.4095 and 1.4020. Resistance is at 1.4150 and 1.4200. Today’s expected range is 1.4050-1.4150.

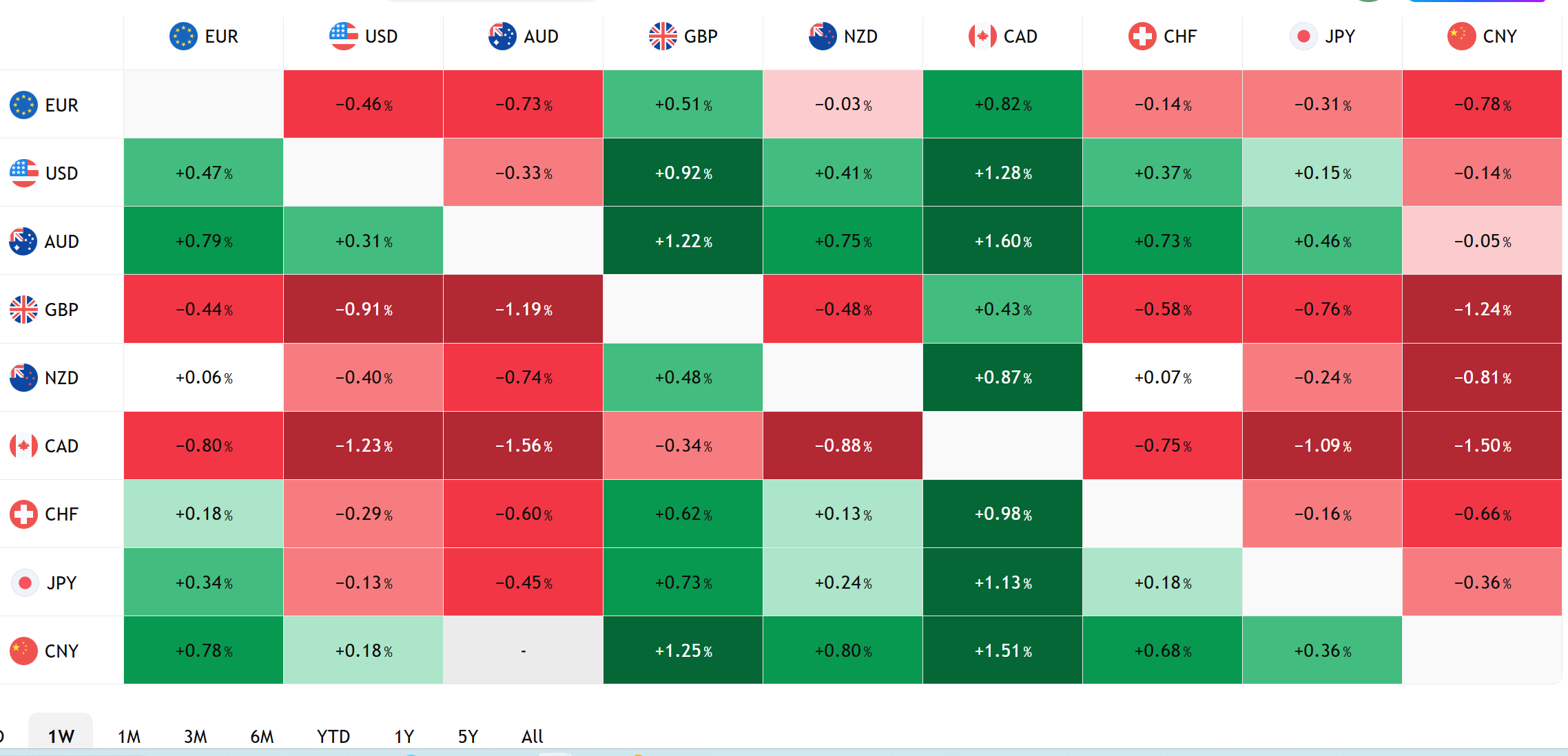

FX Heat Map

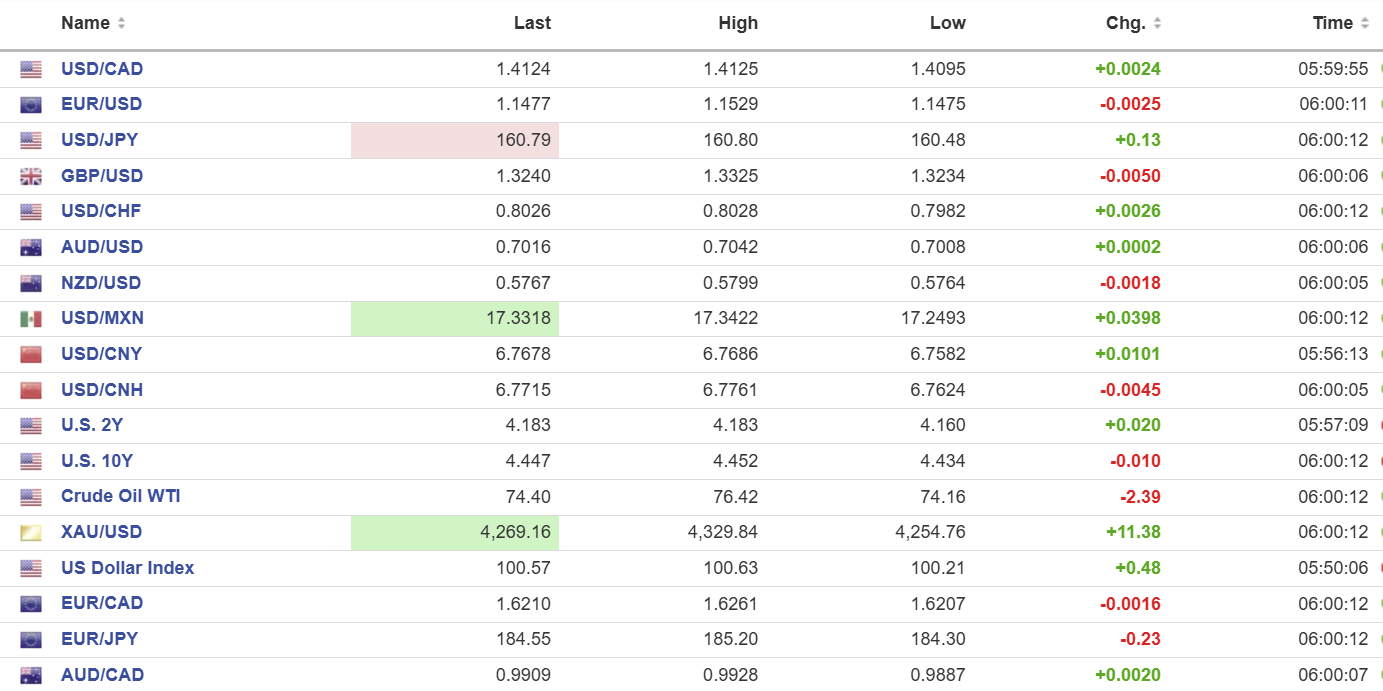

FX open high low 6:00 am

Market are Seeing Dots

The Fed held its benchmark rate steady in the 3.50% to 3.75% range at Wednesday’s meeting. No surprise there. It was the inside curveball that hit traders between the eyes in the form of the dot-plot projections sending a clear signal that rates may be trending higher. Furthermore, inflation expectations were raised meaningfully and getting inflation back under control is a priority. Traders now expect a rate hike in September.

The US dollar index soared from 99.59 yesterday to 100.73 in New York today, while global equity markets got thrashed.

Peace Now, Maybe Bomb Later

Trump and the Iranian president have signed an agreement to end the war in Iran. But even as he was scrawling his name, Trump threatened to resume attacks and kill Iranian leadership if they didn’t live up to the terms.

Taking Stock

Asian equity markets finished with a mixed tone. Japan’s Topix rose 1.37%, bolstered by the US and Iran signing a peace agreement. The Hong Kong Hang Seng Index fell 1.59% due to the belief the FOMC is hawkish, which also drove the Australian ASX 200 down 0.62%.

As of 5:30 am PT, the French CAC 40 is flat, the German DAX is up 0.12% while the UK FTSE 100 has dropped 0.91%. S&P 500 futures have gained 0.83%, the 10-year Treasury yield is 4.43%, the DXY is 100.65, and gold (XAUUSD) is 4,242.53..

EURUSD | Range 1.1463-1.1529

EURUSD dropped on the back of speculation that sticky inflation could force the Fed to hike rates to 4.00% as soon as September, far sooner than anyone expected. The downside may be limited thanks to the end of the US and Iran war knocking oil prices lower and with oil shipments through the Strait of Hormuz resuming. Elsewhere the central banks in Norway and Switzerland left their benchmark rates on hold.

GBPUSD | Range 1.3205-1.3325

GBPUSD is under pressure following the FOMC dot-plots suggesting higher US rates which is contrasting with today’s Bank of England monetary policy decision to leave interest rates unchanged at 3.75%. Policymakers lowered their forecast for inflation to be below 3% in Q3 from 3.3% which suggests that the BoE is on hold for the rest of the year. The UK employment report was better than expected with unemployment falling to 4.9% from 5.0%.

USDJPY | Range 160.48-160.89

USDJPY remained bid but in a narrow range. Prices were supported by expectations for the Fed to hike rates in September, but gains were tempered by officials threatening intervention.

AUDUSD | Range 0.7005-0.7042

Aussie suffered from broad US dollar strength but lingering support from recent hawkish comments by RBA Governor Michele Bullock has slowed the losses.

USDMXN | Range 17.2493-17.3557

USDMXN rallied on broad US dollar demand from fresh fears that the Fed may raise interest rates as soon as September. Trump’s comment that he would consider walking away from the USMCA deal didn’t help even though it is considered to be very unlikely.

CHINA

- PBoC Fix: 6.8130 vs exp. 6.7752 (prev. 6.8096)

- Shanghai Shenzhen CSI 300 rose 0.21% to 4,941.60

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview