June 25, 2026

USDCAD open: 1.4234, overnight range 1.4223-1.4244, close 1.4233

USDCAD drifted overnight as traders were sidelined ahead of today’s key US inflation numbers. A higher-than-expected Core PCE -Price Index reading combined with fresh optimism around US AI and other tech stocks could drive USDCAD well north of 1.4300.

The Bank of Canada Summary of Deliberations, released yesterday, reconfirmed that policymakers believe rates can go up or they could go down.

The case for a rate cut is because the economy remains weak, with excess supply and labour market slack. The case for a rate hike is that the Iran-Israel conflict could keep energy prices elevated long enough for inflation to spread beyond gasoline. For now, the US/Iran war is over (if you believe Trump) which reduces rate hike risks. More importantly, a deterioration in CUSMA negotiations or new U.S. trade restrictions could warrant rate cuts to support growth.

WTI oil prices traded in a 68.91-70.21 range and they are in the middle of that band in NY. The HormuzStraitMonitor.com site shows ships are moving and stacked up.

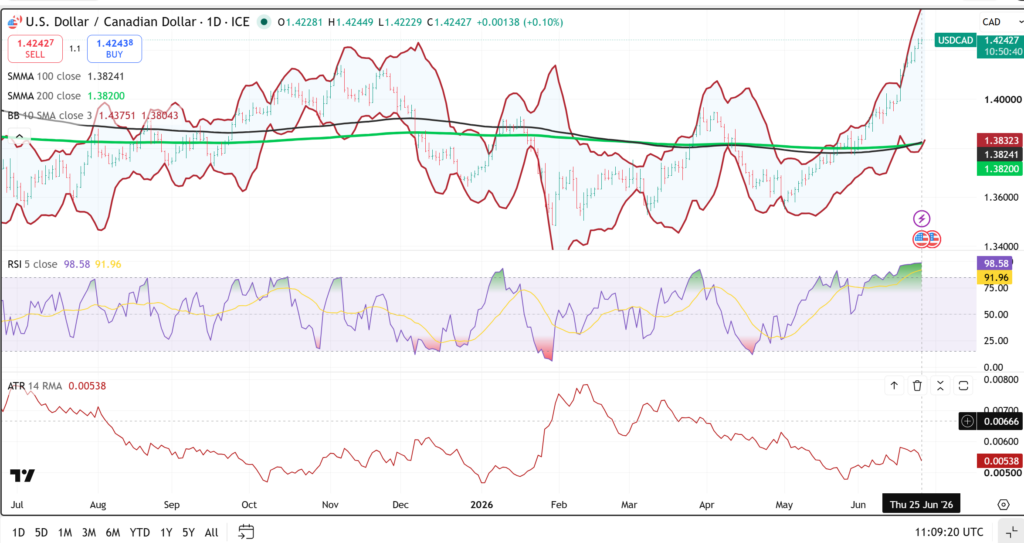

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish following the break above 1.4150. The 1-hour MACD and RSI confirm positive momentum. A sustained break above 1.4260 would target 1.4310, then 1.4350.

Longer term, the rally from the May lows remains intact and has accelerated following the breakout through the 1.4000 and 1.4150 resistance zones. Prices are now testing levels last seen in early April 2025, with the next major upside target located near 1.4280 and then 1.4350.

The daily MACD continues to strengthen and confirms the underlying uptrend. However, the daily RSI is at an exceptionally overbought reading of 98.58 that is rarely sustained for long periods.

For today: USDCAD support is at 1.4200 and 1.4150. Resistance is at 1.4280 and 1.4350. Today’s expected range is 1.4180-1.4280.

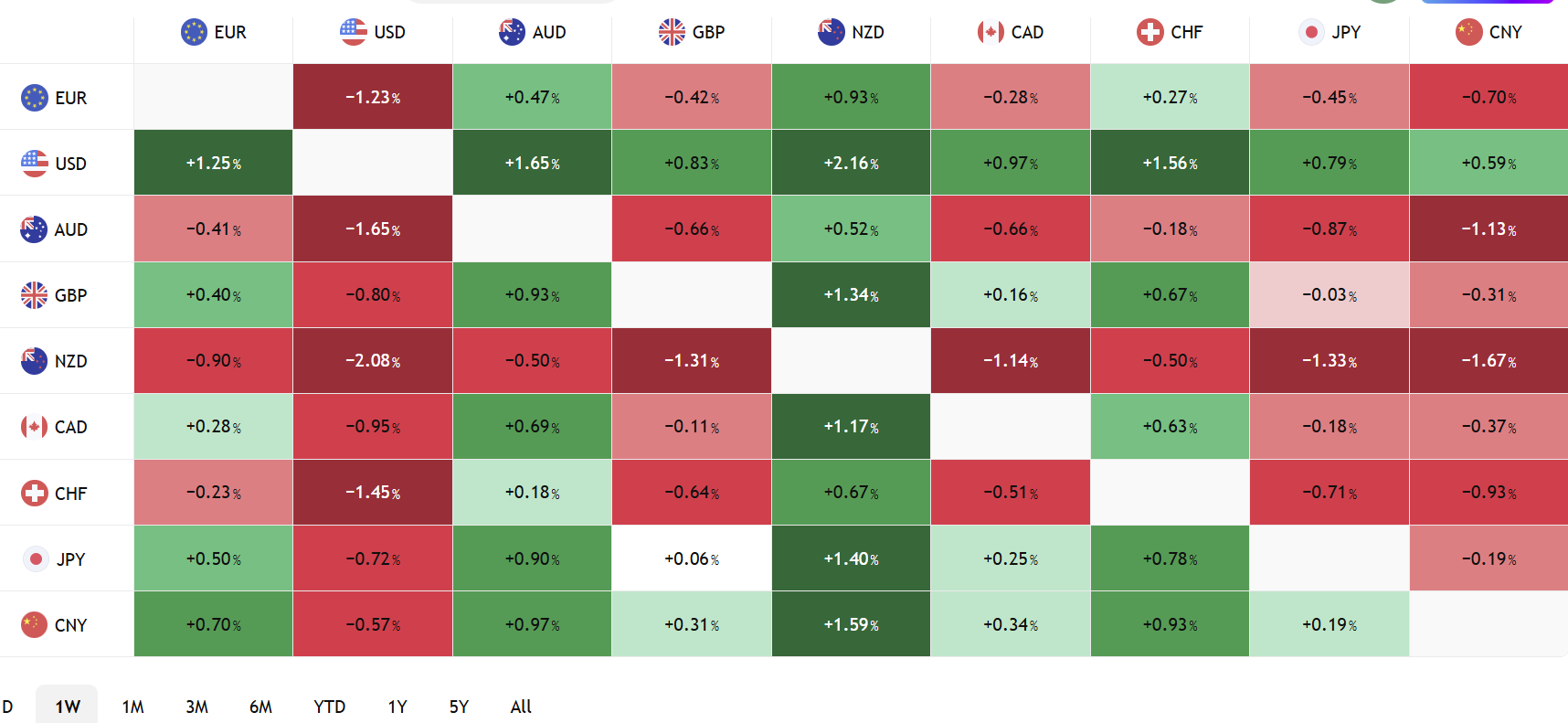

FX Heat Map

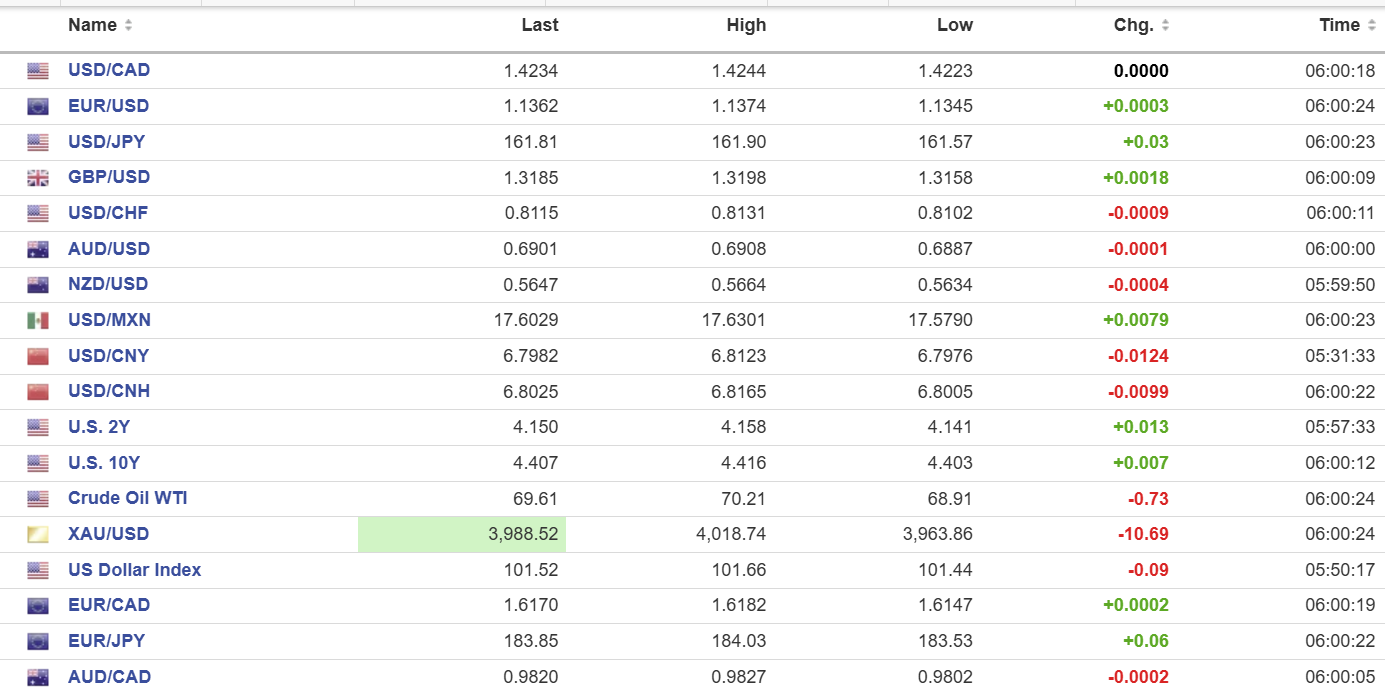

FX open high low 6:00 am

US Inflation Avoids Upside Surprise

The Powell-Fed’s favourite inflation measure Core Personal Consumption Expenditures Price Index (CORE-PCE) rose 0.3% m/m, as expected and 3.4% y/y.

It is important to note that Fed Chair Kevin Warsh is not a fan of that metric. He prefers the Dallas Fed Trimmed Mean PCE which is 2.5%, but it hasn’t been update yet, today.

Weekly jobless claims were 215,000 (forecast 225,000), Q1 GDP rose 2.% (forecast 1.6%) and May Durable Goods Orders ex-transportation rose 1.3% (forecast 0.6%). The data didn’t due much to suggest the US was in dire need of a rate hike.

Markets reacted by knocking Treasury yields and the US dollar lower.

War? What War?

Oil prices have dropped back to pre-Iran-US war levels after oil tankers resumed sailing through the Strait of Hormuz. President Trump is blaming “Big Oil” (Exxon, Chevron, Shell and BP) for high fuel prices and announced a probe into price gouging. Trump is obviously convinced that his decision to start a war with Iran (which, by almost every measure, the US lost) had nothing to do with oil shortages.

Taking Stock

Asian equities closed with Japan’s Topix rallying 1.33% on fresh tech stock earnings. Australia’s ASX 200 slumped 0.68% following a robust employment report which supports a hawkish RBA. Meanwhile, Hong Kong’s Hang Seng Index fell 1.43%.

As of 7:00 am, European bourses are higher. The German DAX is up 0.73%, the French CAC 40 is up 0.53% and the UK FTSE 100 has gained 0.39%. S&P 500 futures are up 0.76%, the 10-year Treasury yield is 4.405%, the DXY is 101.68, and gold (XAUUSD) is 3,982.61.

EURUSD | Range 1.1334-1.1374

EURUSD traded narrowly ahead of this morning’s US data dump and an improvement in risk sentiment. Micron Technology offered a quarterly sales forecast well above Wall Street expectations and AI and Tech optimism returned to the forefront. More importantly, traders are awaiting today’s US numbers and hoping for improved clarity on the US interest rate outlook.

GBPUSD | Range 1.3152-1.3198

GBPUSD nudged higher in a quiet session ahead of the US data. The seemingly annual UK Prime Ministerial leadership contests and divergent Bank of England and Fed interest rate policies are limiting GBPUSD gains.

USDJPY | Range 161.57-161.95

USDJPY extended its recent gains and the only sign of intervention was the usual chirping from BoJ officials “We stand ready to take appropriate action at any time, as necessary.” BoJ policymaker Naoki Tamura repeated his call to speed up the pace of rate hikes. US/Japan interest rate differentials are driving USDJPY gains and FX intervention can’t fix that.

AUDUSD | Range 0.6887-0.6908

Aussie largely ignored a better-than-expected employment report which showed 40,300 new jobs were created in May. That’s because it merely regained the ones that were lost in April. Traders were more focused on the risk of higher US inflation readings bolster the case for a Fed rate hike in September.

USDMXN | Range 17.5790-17.6572

USDMXN traded quietly but remained bid due to broad US dollar strength and narrowing Mexico/US interest rate spreads. Yesterday, Mexican inflation ticked slightly higher and today the jobless rate rose to 2.8% from 2.5% in April. More importantly, the Banxico monetary policy meeting is this afternoon and they are widely expected to leave rates unchanged at 6.5%.

CHINA

- PBoC Fix: 6.8209 vs exp. 6.8048 (prev. 6.8195).

- Shanghai Shenzhen CSI 300 rose 1.56% to 5,020.10

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview