July 2, 2028

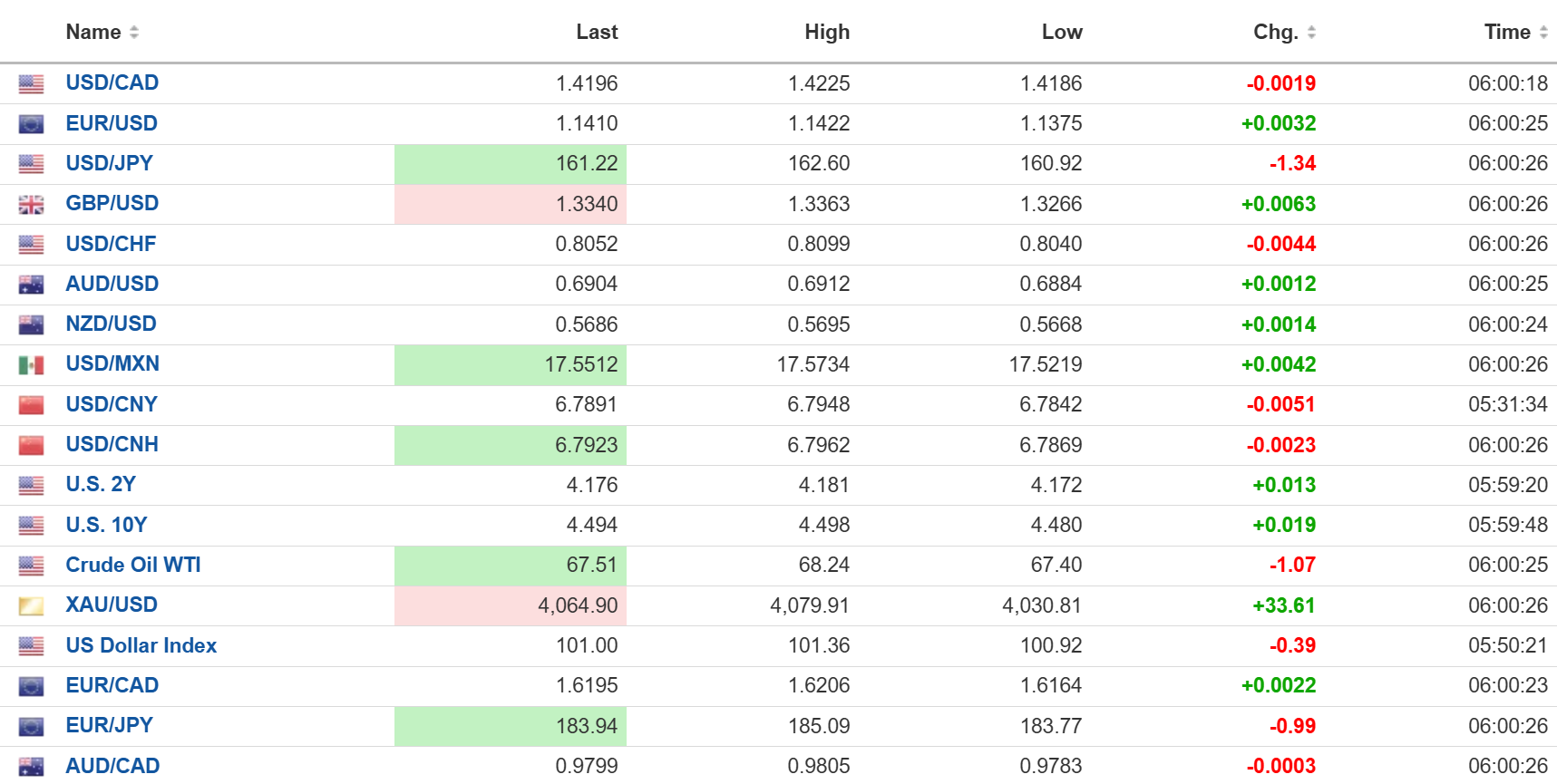

USDCAD open: 1.4196, overnight range 1.4150-1.4225, close 1.4219

USDCAD is drifting lower after tame US employment data downgraded any urgency for the Fed to raise rates. Nevertheless, the Canadian economy remains weak despite the 0.5% gain in GDP in April especially since it is only expected to have grown by 0.1% in May.

USDCAD completely ignored the American decision to not extend the CUSMA trade deal. Canada is in no rush to negotiate another agreement with this administration, given that “deal,” “contract,” and “obligation” are entirely meaningless terms to Trump.

WTI oil prices are down to pre-Iran/US war levels, falling from 70.20 on Friday to 67.29 this morning. Thirty-four ships have sailed through the Strait of Hormuz in the past 24 hours as countries rush to refill depleted oil stocks before Trump attacks Iran again.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish while trading above 1.4160, with a decisive break above 1.4250 targeting 1.4290. A break below 1.4160 suggests a retest of support at 1.4120. Prices are consolidating in the middle of the hourly 1.4169-1.4248 band, with the 4-hour RSI and the MACD histogram flat, suggesting near-term momentum has stalled.

The longer-term outlook is bullish above 1.4100, which guards the uptrend from the May low, with the 200-day moving average rising at 1.3829. The daily RSI has eased from extreme overbought levels and the daily MACD histogram has turned marginally negative, warning that the rally is losing steam and vulnerable to a deeper correction toward 1.3990 if 1.4100 gives way. A break above 1.4275 puts 1.4400 in play.

For today: USDCAD support is at 1.4150 and 1.4120. Resistance is at 1.4250 and 1.4290. Today’s expected range is 1.4100-1.4180.

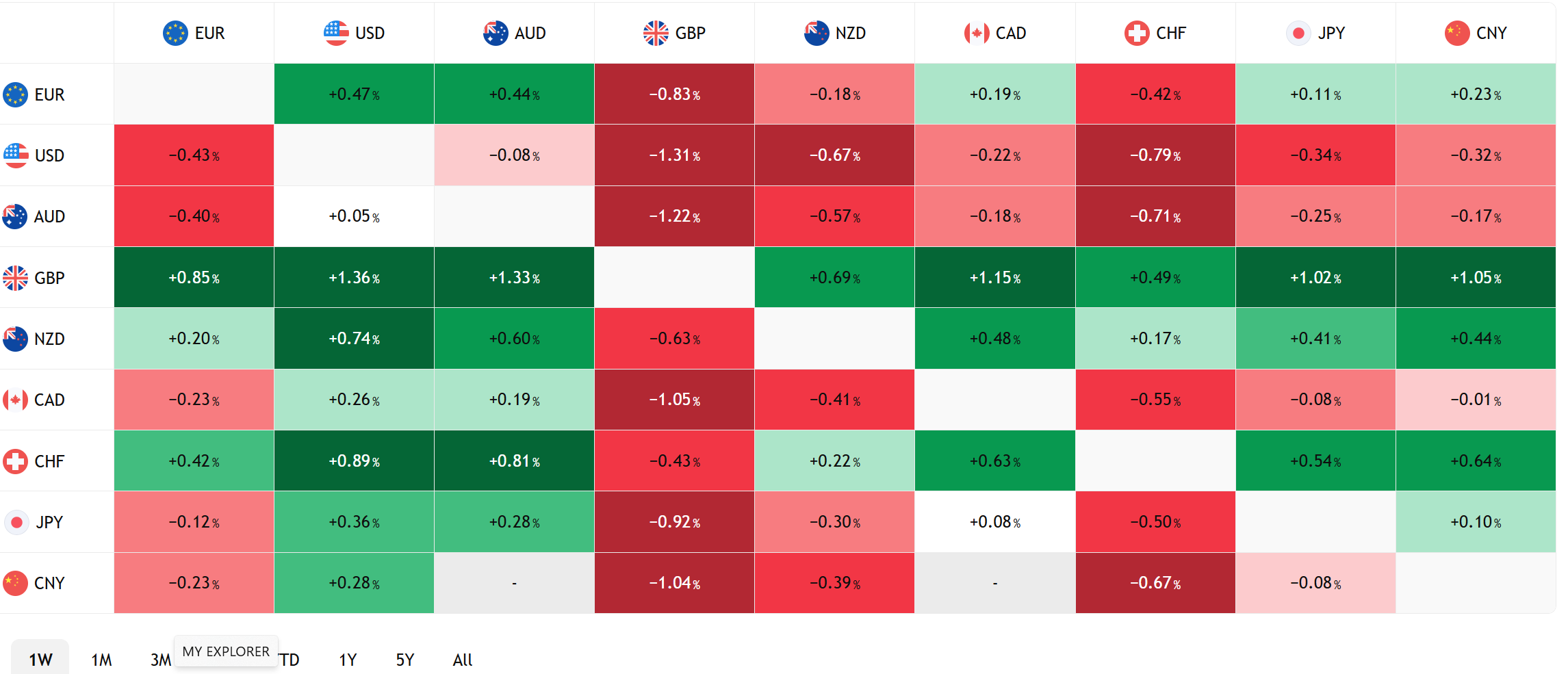

FX Heat Map

FX open high low 6:00 am

No Rate Hike Needed

US nonfarm payrolls rose far less than expected (actual 57,000, forecast 110,000) and May’s result was revised down by 43,000 to 129,000. The unemployment rate ticked down to 4.2% from 4.3%.

Weekly jobless claims were 215,000 compared to expectations of 220,000. All together, today’s jobs numbers, Tuesday’s dramatic 53% drop in Challenger job cuts and Monday’s JOLTS data reinforces a resilient “low-fire, steady-demand” dynamic for the US economy and suggests that the Fed can comfortably leave rates unchanged.

The US dollar slid across the board on the data, Treasury yields eased , gold rose, and European and US stock futures rallied.

Risk Sentiment Improves Slightly

The US and Iran-Intermediary talks in Qatar ended with what Trump said was progress even as his advisers gave him options for “all-out” war. Apparently, Trump was distracted by his ongoing US monument refurbishment plans and his stock portfolio report showing a personal gain of close to $2.0 billion from leveraging his position of “Insider-trader in Chief.”

Fed Chair Kevin Warsh made an appearance at the ECB Forum in Sintra but didn’t provide any guidance on US monetary policy.

Taking Stock

Asian equities closed flat to mixed. Hong Kong’s Hang Seng climbed 0.76% while Australia’s ASX 200 and Japan’s Topix were flat.

As of 5:45 am PT, European bourses are in the green. The German Dax is up 1.45%, the French CAC 40 has gained 1.27% and the UK FTSE 100 has risen 0.84%. S&P 500 futures are up 0.35%, the 10-year Treasury yield is 4.465%, the DXY is 100.64 and gold (XAUUSD) is 4,124.44

EURUSD | Range 1.1375-1.1473

EURUSD clawed back yesterday’s losses and is near the top of its overnight and yesterday’s peak. Eurozone unemployment was unchanged at 6.2% in May. Eurozone inflation data was softer than expected. Harmonized Index of Consumer Prices (HICP) and Core-HICP rose 2.8% y/y and 2.4% y/y, which suggests the ECB may leave rates unchanged at its July 23 meeting. The annual ECB forum saw President Christine Lagarde suggesting that the central bank would return to basics and could dispense with complex forward guidance.

GBPUSD | Range 1.3266-1.3383

GBPUSD got a “Burnham Bounce.” The man anointed to be the next Prime Minister managed to convince markets (to a degree) that he wasn’t an irresponsible “spend and borrow” politician, with a plan to redistribute wealth. Instead, he would stick to “strict fiscal discipline and adhere to the UK’s current borrowing and spending limits.” GBPUSD also got support from lower oil prices although caution ahead of today’s US data limited gains.

USDJPY | Range 160.93-162.60

USDJPY traders pushed the BoJ a tad too far and the result was a nearly 1.0% plunge in the currency pair. Authorities have not confirmed they intervened but the magnitude of the drop and the USDJPY level at the time point to either BoJ officials slamming bids or the more subtle “checking rates” ploy. Nevertheless, it still was not much of a result, but that could change tomorrow, with the US on holiday.

AUDUSD | Range 0.6884-0.6942

Aussie traded sideways torn between the disappointment of soft data recently and improved risk sentiment from falling oil prices and “progress” with Iran and US peace talks.

USDMXN | Range 17.4353-17.5044

USDMXN shrugged off the American decision to not extend the USMCA agreement in favour of annual talks. The reality is that an agreement with Trump’s America on trade is worthless as it has been proven time and time again since the infamous “Liberation Day” tariff announcement last year.

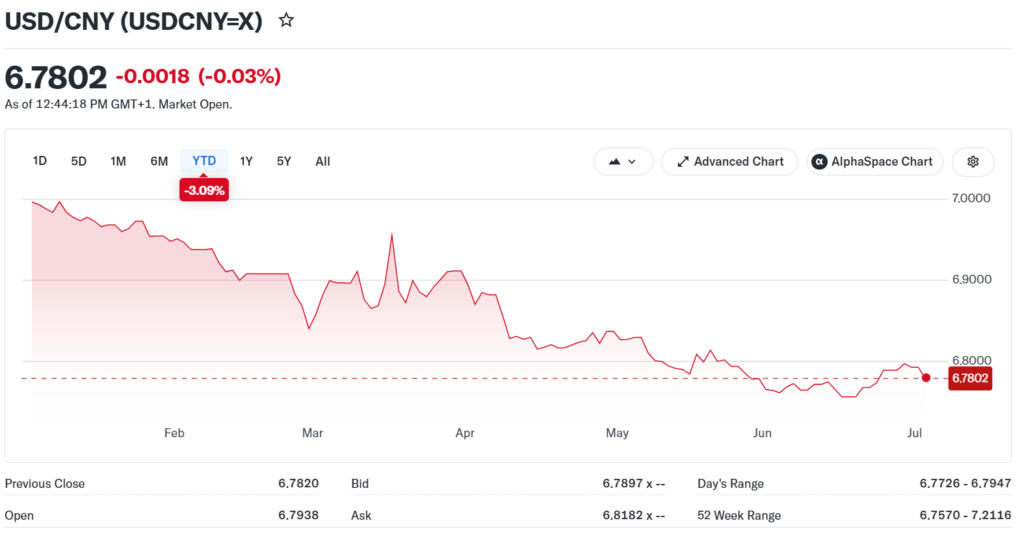

CHINA

- PBoC Fix: 6.8109 vs exp. 6.7877 (prev. 6.8175)

- Shanghai Shenzhen CSI 300 fell 2.96% to 4,812.30

Fall-out from recent trade restrictions aimed at Chinese tech companies by the US, helped fuel the slide.

Yesterday, RatingDog PMI came in at 51.7, a tick lower than the 51.8 result in May. It was the 7th consecutive month of expansion. The report said “Overall, the manufacturing sector maintained a steady expansion in June, supported by sustained new order growth, easing cost pressures and improved labour market conditions.”

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview