October 31, 2025

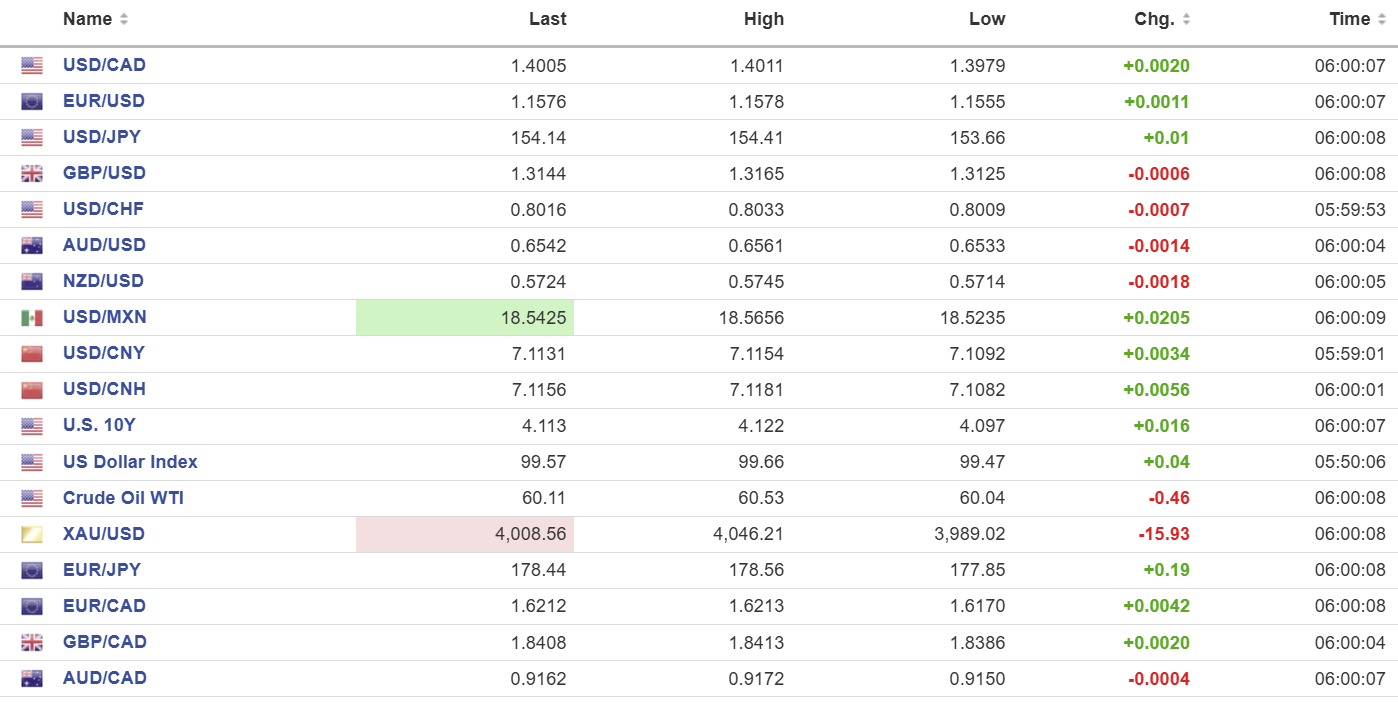

USDCAD open: 1.4005, overnight range 1.3979-1.4032, close, 1.3987

Last Friday, USDCAD closed in NY at 1.4003 and this Friday it opened around the same level which just goes to prove, miss a week and you don’t miss anything. The Fed did the expected and cut its benchmark rate by 25 bps, and even though Fed Chair Powell said that a December cut is far from a done deal, the odds are still 66.8% for a cut.

USDCAD spiked to its session peak of 1.4032 on the back of the latest GDP report. GDP shrank by 0.3% in August (forecast flat) compared to -0.3% in July. The August data shows the economy took a significant step backward, driven by a combination of strike-related disruptions, environmental challenges, and genuine weakness in key industrial sectors.

Prime Minister Mark Carney met with China President Xi Jinping. Carney said he was happy with the meeting according to Bloomberg, “We now have a turning point in the relationship — a turning point that creates opportunities for Canadian families, for Canadian businesses and Canadian workers.”

In turn, Mr. Jinping said that “China is willing to work with Canada to push China-Canada ties to return to the correct track of being healthy, stable and sustainable as soon as possible.”

WTI oil traded narrowly in a 60.00-60.53 range with prices weighed down by the robust US dollar and soft manufacturing data from China. Opec is expected to raise production in December.

There are plenty of option expiries today including $965 million of 1.3950 strikes, $505 million of 1.3970 strikes and $535 million of 1.4000 strikes maturing at 10:00 am.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish following yesterday’s rally above resistance in the 1.3970 area which now targets the minor downtrend line from the October 14 peak which is at 1.4040. A break above that level targets 1.4110

The medium-term technicals are bullish with the end of July uptrend channel intact while prices are between 1.3850 and 1.4140.

For today, USDCAD support is at 1.3970 and 1.3930. Resistance is at 1.4040 and 1.4080.

Today’s Range: 1.3960-1.4040

Greenback Consolidating Gains

The US dollar caught a bid yesterday afternoon, and it continued higher overnight.

Firmer Treasury yields, a thaw in China/US trade tensions, and Fed Chair Powell’s hawkish tone combined to encourage a reduction of short dollar positions. The greenback was also underpinned by positive US tech stock earnings. It is month-end, and the expectation is that portfolio managers will need to sell US dollars at the 11:00 am fix.

Taking Stock

Asian equity indexes finished the session with losses except for Japan’s Topix, which rose 0.94%. Hong Kong’s Hang Seng lost 1.43%, and Australia’s ASX 200 was flat.

As of 5:40 AM, PDT, the UK FTSE 100 index is down by 0.23%, the German DAX has lost 0.26%, and the French CAC-40 index is off by 0.16%. S&P 500 futures are up 0.82%, and the U.S. Dollar Index (DXY) is 99.64. The U.S. 10-year Treasury yield is 4.092%, and Gold (XAUUSD) is 4031.07

EURUSD

EURUSD consolidated yesterday’s losses in a 1.1555–1.1578 range. German retail sales data was softer than expected, as was Eurozone harmonized inflation. The ECB left interest rates unchanged yesterday. The main refinancing rate remains at 2.15%, the deposit facility rate at 2.00%, and the marginal lending facility at 2.40%. The press conference reiterated that policymakers were cautious and monitoring incoming data.

GBPUSD

GBPUSD traded negatively in a 1.3125–1.3165 range due to general US dollar demand, caution ahead of next week’s Bank of England meeting, and ongoing worries about the November 26 autumn budget. Wednesday’s hawkish Fed tilt is also weighing on GBPUSD.

USDJPY

USDJPY traded in a 153.66–154.41 band, with the low seen following a bit of verbal intervention by Finance Minister Satsuki Katayama. It was the usual blather about disorderly moves being monitored, and USDJPY quickly recouped its losses.

AUDUSD

AUDUSD traded in a 0.6531–0.6561 range, with prices suffering from resurgent US dollar demand, which overshadowed earlier optimism after China/US trade tensions eased. Australia’s Producer Prices Index rose 1.0% q/q ending in September and 3.5% year-to-September. Traders are also awaiting the results of the November 4 RBA meeting.

USDMXN

USDMXN consolidated this week’s gains in an 18.5235–18.5683 band due to somewhat contrasting central bank interest rate policies. Banxico is still cutting rates, while Fed Chair Powell is weighing leaving rates unchanged for the rest of the year.

China

PBoC Fix: 7.0880 vs exp. 7.1171 (Prev. 7.0864)

Shanghai Shenzhen CSI 300 fell 1.47% to 4640.67

NBS October Manufacturing PMI 49 (forecast 49.6, September 49.8)

The broad-based decline in the manufacturing PMI is a six-month low, while non-manufacturing is 50.1.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics