November 6, 2025

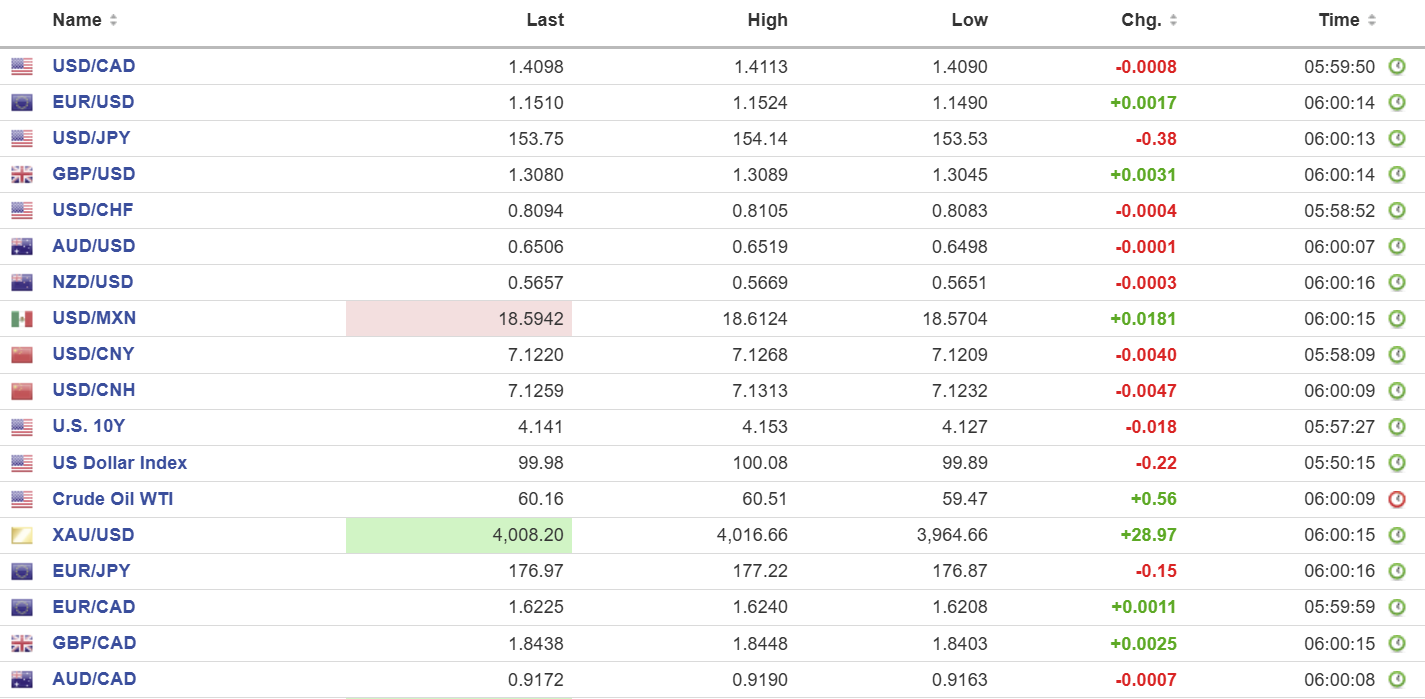

USDCAD open: 1.4097, overnight range 1.4090-1.4113, close, 1.4108

USDCAD put the brakes to this week’s rally yesterday thanks to a bout of positive risk sentiment from US data and higher prices on Wall Street.

Bank of Canada Governor Tiff Macklem testified before the House of Commons Finance Committee yesterday. His remarks were nearly identical to last week’s monetary policy statement. He emphasised that the bank rate of 2.25% is “about the right level” and reiterated that that tariffs have caused structural damage, limiting how much monetary policy can stimulate demand.

WTI oil prices drifted lower in a 59.47-60.51 range in line with the softer US dollar.

The US Challenger Report said the layoffs spiked to 153,074, the highest level for October since 2002, on cost-cutting and AI. The report said “Some industries are correcting after the hiring boom of the pandemic, but this comes as AI adoption, softening consumer and corporate spending, and rising costs drive belt-tightening and hiring freezes. Those laid off now are finding it harder to quickly secure new roles, which could further loosen the labor market.”

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish while trading above 1.4080 and looking to retest the peak of 1.4140, although USDCAD remains overbought. A move below 1.4080 could extend losses to 1.4050.

The medium-term technicals are bullish with USDCAD above the 200 day moving average at 1.3948 and the psychological 1.4000 level. The momentum indicators are still overbought which suggests a 1.4060-1.4160 consolidation range in the near term.

For today, USDCAD support is at 1.4080 and 1.4050. Resistance is at 1.4140 and 1.4170.

Today’s Range: 1.4060-1.4140.

Not Flying High

US airlines and the US dollar are no longer flying high. The US government shutdown forced the Transportation Secretary to slash flights by 10% at 40 US airports due to staff shortages. Apparently, people do not show up for work when they are not getting paid.

The greenback traded lower across the board yesterday following better-than-expected US ADP and ISM services PMI numbers for October. ADP reported a 42,000 increase in new jobs (forecast 25,000) while Services PMI reached an eight-month high of 52.4 (previous 50). The results served to lower the odds for a December rate cut, albeit very modestly.

Taking Stock

Asian equity markets embraced yesterday’s Wall Street rally with enthusiasm. Hong Kong’s Hang Seng soared 2.12%, Japan’s TOPIX rose 1.38%, and Australia’s ASX 200 dropped 0.13%.

As of 7:00 a.m., European bourses are negative, led by a 0.55% drop in the French CAC-40. The German DAX is down 0.12% and the FTSE 100 index is down 0.30%. S&P 500 futures are flat, and the US Dollar Index (DXY) is 99.98. The US 10-year Treasury yield is 4.134%, and gold (XAUUSD) is $4012.94.

EURUSD

EURUSD drifted higher in a 1.1490–1.1524 range with support coming from German industrial production numbers for September (actual 1.3% m/m, forecast 3.3%, August -3.7% m/m). ECB Vice President Luis de Guindos said policymakers were happy with the current level of interest rates and that any dip in inflation below the 2.0% target would be temporary.

GBPUSD

GBPUSD traded in a 1.3045–1.3095 band, peaking after the Bank of England left rates unchanged at 4.0% in a 5-4 decision. Governor Andrew Bailey and policymakers Megan Greene, Clare Lombardelli, Catherine L Mann, and Huw Pill voted to hold because of sticky inflation, even though the Bank said, “CPI inflation is judged to have peaked.” Analysts now expect a 25 bp rate cut in December.

USDJPY

USDJPY traded defensively in a 153.53–154.14 range due to general US-dollar weakness, but the downside was supported by steady-to-firm Treasury yields. Japan’s Services PMI was 53.1 in October (compared to forecast 52.4) and was not a factor. The Japanese government is working to finalize an economic stimulus plan before the end of the month.

AUDUSD

AUDUSD traded sideways in a 0.6498–0.6519 range. The pair is underpinned by the RBA’s decision to leave rates unchanged (as expected) and by broad US-dollar selling after yesterday’s ADP and ISM Services data. Australia’s trade surplus also widened to AUD 3.938 billion from AUD 1.11 billion last month.

USDMXN

USDMXN consolidated Wednesday’s losses in an 18.5704–18.6124 range ahead of Banxico’s monetary policy decision today. The central bank is expected to cut its benchmark rate to 7.25% from 7.5%.

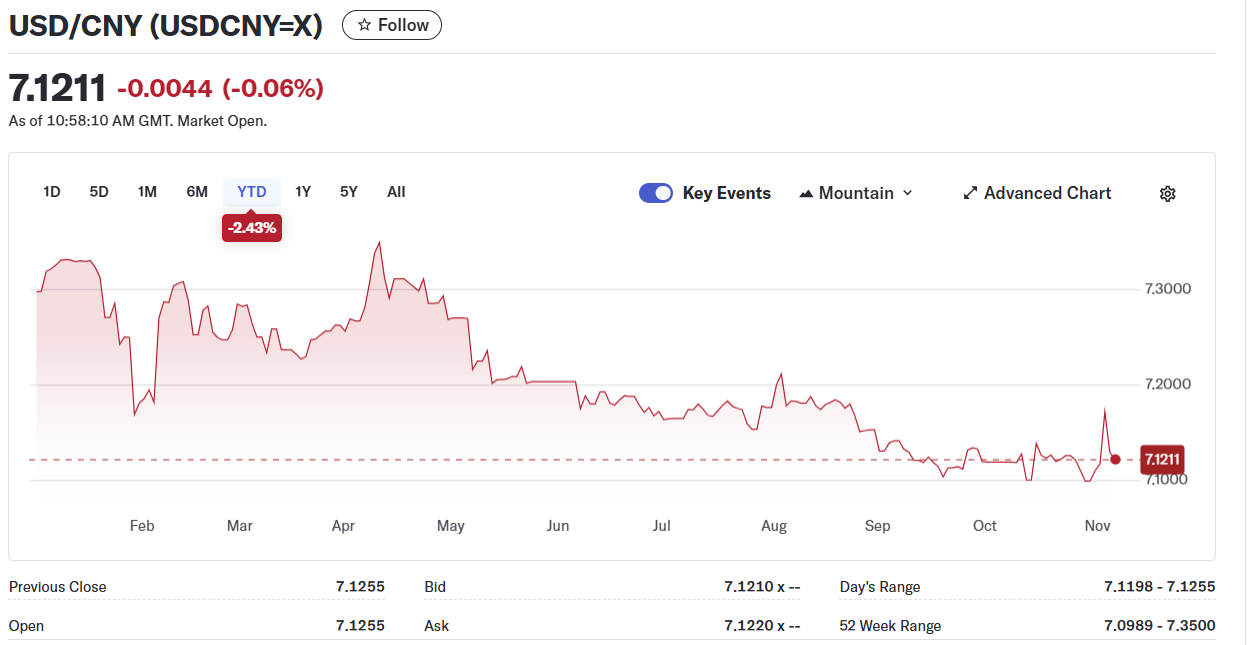

China

PBoC Fix: 7.0865 vs exp. 7.1222 (Prev. 7.0901)

Shanghai Shenzhen CSI 300 rose 1.43% to 4693.40

The International Air Transport Association (IATA) is adding the yuan to the basket of currencies available for payments through its clearing house, beginning next month.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics