November 17, 2025

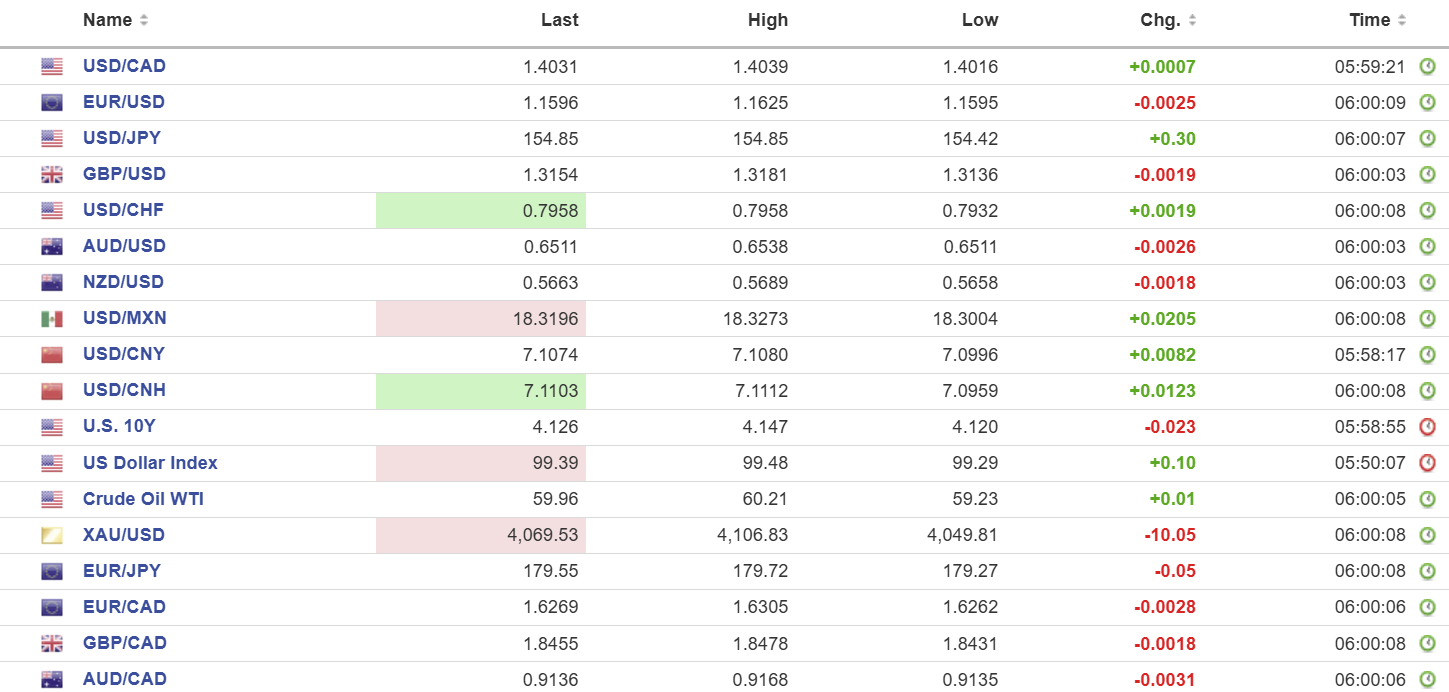

USDCAD open: 1.4032, overnight range 1.4016-1.4039, close, 1.4023

USDCAD traded with a mild bid due to the risk of steady to higher US interest rates. Fed officials do not seem in any hurry to cut interest rates (except Governor Stephen Miran) supported by the lack of actionable economic data for 46 days. A data dependent, decision making Fed cannot make decisions without data. Data starts trickling in this week, but the reports are still two months old.

The Mark Carney government faces the final non confidence vote on the budget today. The Conservatives and Bloc said they would vote against it but Carney only needs two votes to win. The Green Party leader (and only member of parliament) said she would not support it either, but she is open to negotiations. Carney won’t need her as two NDP MP’s are planning to abstain.

Canadian inflation ticked higher in October, rising 0.2% (as expected) compared to 0.1% in September.

WTI oil prices traded in a 59.23-60.21 range. Prices are supported by reports that India and China are buying more Middle Eastern crude, but gains are capped because Opec has no interest in reducing production.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish but consolidating in a narrow 1.4010-1.4050 trading band. A move below 1.4010 suggests a retest of support at 1.3960 while a topside break targets the 1.4100 area.

The medium term technicals confirm an uptrend grind while prices are above the 100 day moving average (1.3853) and 200 day moving average (1.3931) but gains are hampered by a cluster of resistance in the 1.4080-1.4100 zone.

For today, USDCAD support is at 1.4010 and 1.3980. Resistance is at 1.4040 and 1.4070.

Today’s Range: 1.3990-1.4080.

Data Starts to Dribble

The US economic data pipeline starts to unclog today when the Census Bureau releases the August Construction Spending report (forecast -0.1%, previous -0.1%). Tuesday they release the full Manufacturers shipments, inventories and orders data for August along with US Trade data. Wednesday, the release of the FOMC minutes from the October 29 meeting are on tap. The September employment report from the Bureau of Labor Statistics is due Thursday.

The New York Empire State Manufacturing Index rose to 18.7 in November (October 10.7)

Fed Officials Drive Rate Cut Odds Lower

The CME FedWatch tool pegs the odds for the Fed to cut rates at 44.6% and recent comments by a host of Fed officials are the reason. Dallas Fed President Lorie Logan said it would be hard to support another cut. Atlanta Fed President Raphael Bostic warned that the economy is not moving in the direction of targets. The lone voice for a rate cut is Governor Stephen Miran who claims the data supports rate cuts, despite Fed departments not issuing any data for the past 46 odd days.

Taking Stock

Asian equity markets closed with losses except for Australia’s ASX 200 which finished the session flat. Japan’s Topix fell 0.37% while Hong Kong’s Hang Seng dropped 0.71%.

As of 5:30 am PT, European bourses are in negative territory. The German DAX is down 0.73% followed by the French CAC 40 which is down 0.52% and the UK FTSE 100 which has lost 0.29%. S&P 500 futures are flat with traders awaiting Nvidia earnings after the close on Wednesday. The U.S. Dollar Index (DXY) is 99.45, the U.S. 10-year Treasury yield is 4.14% and Gold (XAUUSD) is 4069.14

EURUSD

EURUSD traded uneventfully in a 1.1595-1.1625 range and is sitting near the bottom of that band in early NY trading after the European Commission unveiled its Autumn forecasts. Forecasters expect that the Euro area will grow at a faster pace in 2025 (real GDP 1.4% vs previous forecast of 0.9%), but 2026 growth is expected to slow to 1.2%. Switzerland secured a trade deal with the US which cut tariffs from 39% to 15%. The deal was spurred along by generous gifts to the President including a golden table clock by Rolex.

GBPUSD

GBPUSD had a choppy session in a 1.3136-1.3181 range. The currency continues to be buffeted by upcoming budget concerns which have roiled the gilt market. The UK Rightmove House Price Index fell 1.8% m/m in November and 0.5% y/y. Traders are looking ahead to Wednesday when CPI and PPI data is released.

USDJPY

USDJPY rallied in a narrow 154.42-154.87 range with prices supported by weak Japanese data and the ongoing spat with China. Japan’s Q3 GDP fell 1.8% compared to 2.3% in Q2 but the Q3 result was better than expected. The Q3 GDP price index rose 2.8% q/q which was lower than forecast (3.1%) and in Q2 (actual 2.9%). Chinese Premier Liu Jinsong refused to meet with Japan’s Prime Minister Sanae Takaichi at the G20 because Beijing is still mad at Takaichi’s comments about Taiwan.

AUDUSD

AUDUSD bounced in a 0.6509-0.6538 band. Monetary policy was restrictive enough to contain inflation, which underpinned the currency. Prices are tracking broad US dollar sentiment with traders awaiting this week’s US economic reports.

USDMXN

USDMXN drifted sideways in an 18.3004-18.3273 range. Mexican trade officials are meeting with the U.S. Trade Representative’s office as part of the process for the 2026 review of the US Mexico Canada trade deal. Mexico is also dealing with anti-government protests.

China

7.0816 vs exp. 7.0956 (Prev. 7.082)

Shanghai Shenzhen CSI 300 fell 0.65% to 4598.95.

China warned people not to travel to Japan and 491,000 people cancelled air tickets.

Chinese Premier Li Qiang said he has no plans to meet with Japanese Prime Minister Sanae Takaichi at G-20 meeting due to the ongoing spat.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics