December 3, 2025

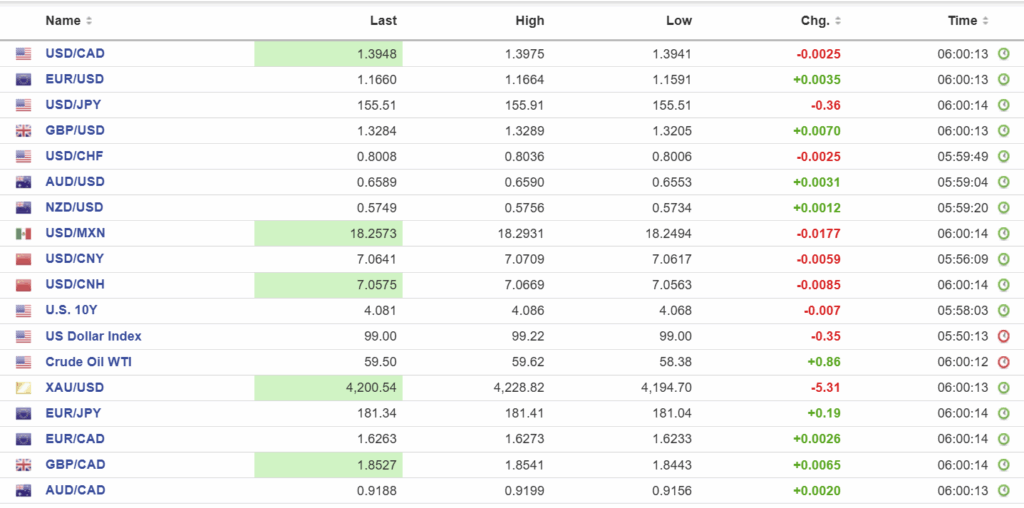

USDCAD open: 1.3948, overnight range 1.3939-1.3975, close 1.3968

USDCAD is riding the bearish dollar wave due to divergent monetary policy outlooks for December BoC and Fed meetings. The Fed is almost guaranteed to cut its benchmark rate by 25 bps while the BoC leaves its rate unchanged. Traders are also looking to 2026 and expecting that Trump’s pick for Fed Chair will be an advocate for easy monetary policies.

WTI oil prices climbed from 58.38 to 59.62 underpinned by the latest American Petroleum Institute data showing crude inventories fell by 2.48 million barrels last week, on top of the 1.9 million barrel drop the week before. In addition the lack of progress on the Ukraine Russia peace talks supported prices.

There are no Canadian economic reports of note today.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish below 1.3990 and looking to crack support in the 1.3900-1.3920 area to extend losses to 1.3860. However the intraday RSI indicates that USDCAD is oversold. A move above 1.3990 suggests a retest of the 1.4040 area.

The medium-term technicals are bullish but vulnerable especially as trading liquidity begins to lessen into the holiday season. USDCAD bears would assume control on a break below 1.3860 which would put 1.3720 in play.

For today, USDCAD support is at 1.3940 and 1.3900. Resistance is at 1.3990 and 1.4020.

Today’s Range: 1.3900-1.3990

Trump Stirring the Fed Pot

The WSJ says the Trump administration abruptly cancelled a round of interviews for the soon-to-be vacant Federal Reserve Chair position. The candidates were probably relieved. The interviews were reportedly to be conducted by the Hillbilly Vice President and were rumoured to include a pig-calling contest and a banjo duel. Straight out of Deliverance.

Trump also floated Kevin Vance as a possible Fed Chair during a cabinet meeting, which was enough to spark another wave of US dollar selling.

US Data Unlikely to Change Outlook for Fed

The ADP employment report for November showed a loss of 32.000 jobs compared to the forecast of 5,000 and well below the 42,000 increase in October. That release is followed by ISM Services PMI, forecast at 52.1 compared to 52.4 in October. Neither report is expected to alter the view that the Fed is shifting to a gentler policy stance.

Taking Stock

Asian equity markets ended mixed. Australia’s ASX 200 rose 0.19%, Japan’s Topix slipped 0.20%, and Hong Kong’s Hang Seng index fell 1.39%.

As of 5:30 am PT, European markets are grinding out tinny gains except for the UK FTSE 100 index which is down 0.14%. The German DAX is up 0.17%, the French CAC-40 is flat, and S&P 500 futures are up 0.25%. The US Dollar Index (DXY) is 98.90, the US 10-year Treasury yield is 4.063%, and gold (XAUUSD) is $4217.07

EURUSD

EURUSD climbed within a 1.1591-1.1675 range after Trump’s comments hinting that National Economic Director Kevin Hasset could replace Chair Powell. Mr. Hasset is viewed as “Trump’s man,” and traders assume he would steer the Fed toward a dovish path. At the same time, markets increasingly believe the ECB’s rate-cut cycle has run its course. Better-than-expected German and Eurozone Services and Composite PMI results added support, but the rally paused after slightly softer PPI data.

GBPUSD

GBPUSD drifted higher in a 1.3205-1.3316 band, supported by persistent US dollar selling triggered by expectations for a more dovish Fed stance in 2026. The move came despite UK Services PMI slipping to 51.3 from 52.3. S&P Economics Director Tim Moore noted that “survey respondents widely commented on business challenges linked to fragile client confidence, heightened risk aversion and elevated” uncertainty. GBPUSD gains will remain corrective unless prices break above 1.3330.

USDJPY

USDJPY eased within a 155.23-155.91 range. Japanese Services PMI edged up to 53.2 from 53.1. S&P Global Economics Associate Director Annabel Fiddes said the data showed “a further modest expansion of private sector output in Japan, as a solid increase in service sector activity offset a slight reduction in factory output.” She added that the steady improvement in activity and new business was accompanied by “stronger inflationary pressures,” which will keep pressure on the BoJ to consider tightening.

AUDUSD

AUDUSD is trading near the top of its 0.6553-0.6595 range despite weaker-than-expected Q3 GDP growth of 0.4% q/q versus the 0.7% forecast. Composite and Services PMI were close enough to expectations to be non-events. Broader US dollar softness and expectations that the RBA will leave rates unchanged helped keep AUDUSD supported.

USDMXN

USDMXN is near the bottom of its 18.2473-18.2931 range. Renewed selling pressure stemmed from Trumps comments about the Fed and the elevated Banxico interest rates.

China

PBoC Fix: 7.0754 (Prev. 7.0779)

Shanghai Shenzhen CSI 300 fell 0.05% to 4515.40.

China RatingDog November Services PMI 52.1 vs. forecast 52.1 (Prev. 52.6)

Composite PMI 51.2 (Prev. 51.8).

French President Macron starts 3-day visit to China. French trade is top of the agenda as Macron favours more protectionist policies for EU and tariffs on Chinese EV’s.

Morgan Stanley analysts claim global business sentiment towards China has risen but the China/Japan dispute and ongoing grief about Taiwan are a drag on the outlook.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics