September 24, 2025

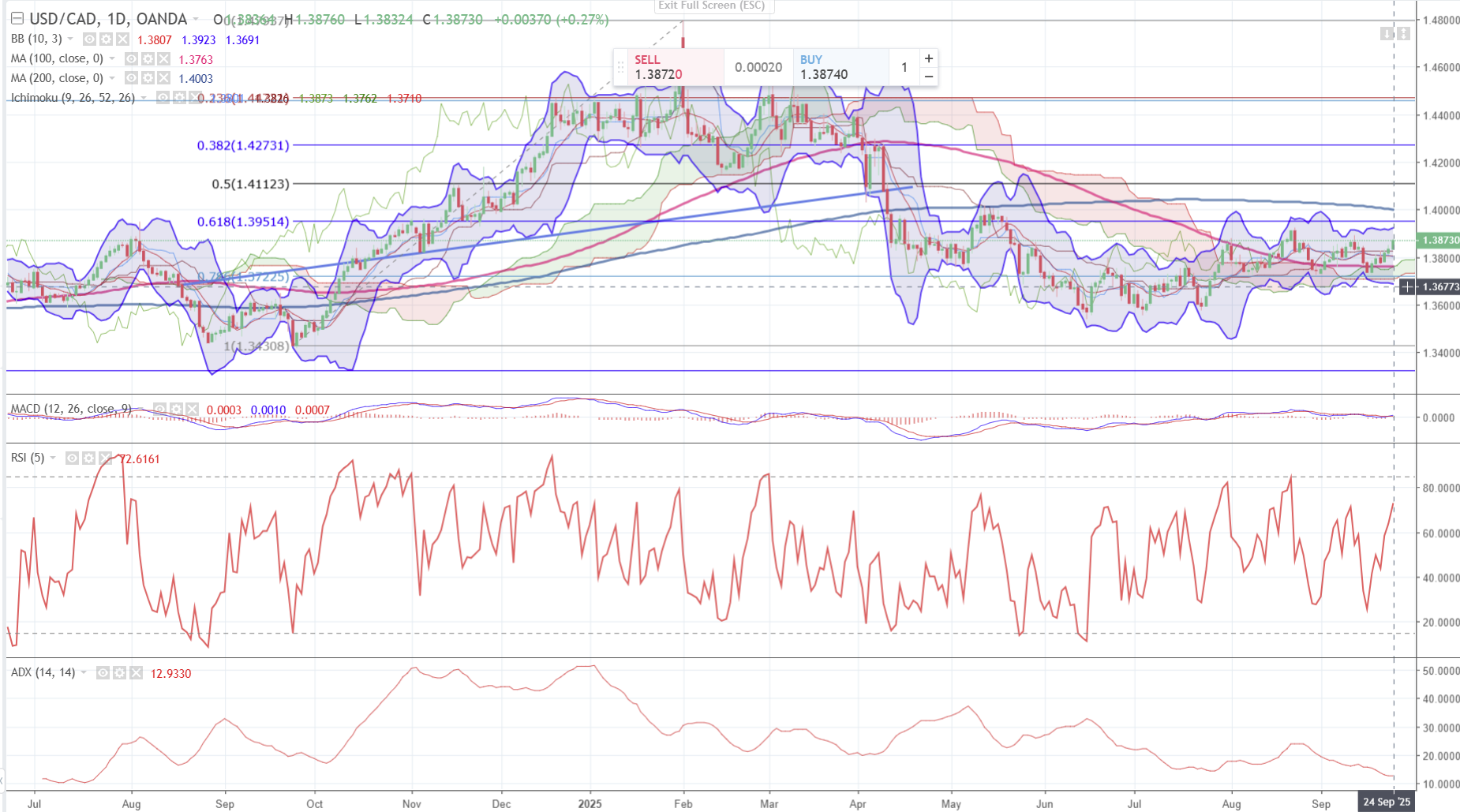

USDCAD open 1.3870, overnight range 1.3838-1.3879, close, 1.3837

USDCAD is grinding out gains due to wide-spread US dollar strength and Bank of Canada Governor Tiff Macklem’s downbeat outlook for the economy. The Governor said that tariffs are permanently lowering growth by cutting exports and slowing job creation. His remarks support another rate cut on October 29.

WTI oil prices traded with a bit of a bid in a 63.26-64.19 range. The mix of rising tensions between Trump and Putin following Trump’s UN speech, and low global inventories.

USDCAD may be sticky around the 10:00 am option expiry window when $1.2 billion of 1.3850 strikes roll off.

Today’s US data includes New Home Sales. The Canadian calendar is empty.

USDCAD Technical Outlook:

The intraday technicals are bullish supported by the break above the 1.3850-60 area but momentum indicators suggesting overbought conditions suggest a drop to 1.3810 may be needed before 1.3950 gets tested.

The medium-term technicals are moderately bullish but it is overbought according to momentum indicators. A failure to break above 1.3950 argues for more 1.3600-1.3950 consolidation.

For today, USDCAD support is 1.3840 and 1.3810. Resistance is 1.3910 and 1.3950. Today’s Range: 1.3810-1.3910

Trump Scolds UN

President Trump told the gathered mass of UN diplomats what he thought of the organization.

The scolding was long overdue. He mocked the UN for writing “strongly worded letters” then never following up. He complained that some UN members were giving in to Hamas and planning to unilaterally recognize Palestine. He took shots at China and India for funding Putin’s war and said that if the UN did not get away from the green energy scam, they would fail. He defended his tariffs and complained about a broken escalator in the building.

He may have “accidentally-on-purpose” put French President Emmanuel Macron in his place when he forced the French leader to stand on a curb and wait for the Presidential motorcade to pass.

Powell Puts Fails to Put Rate Doves in Their Place

Fed Chair Jerome Powell said that the economy was resilient but admitted that the pace of economic growth had slowed from the beginning of the year. He added that the base case is that tariff-related effects on inflation will be short lived, but near-term risks are tilted to the upside. Powell’s comments did nothing to change the belief of another 25 bp rate cut on October 29.

Taking Stock

Asian equity traders shrugged off the negative close on Wall Street and bought stocks. Japan’s Topix rose 0.23% and the storm-battered Hang Seng rose 1.37%. Australia’s ASX 200 lost 0.92% on the back of higher-than-expected inflation data.

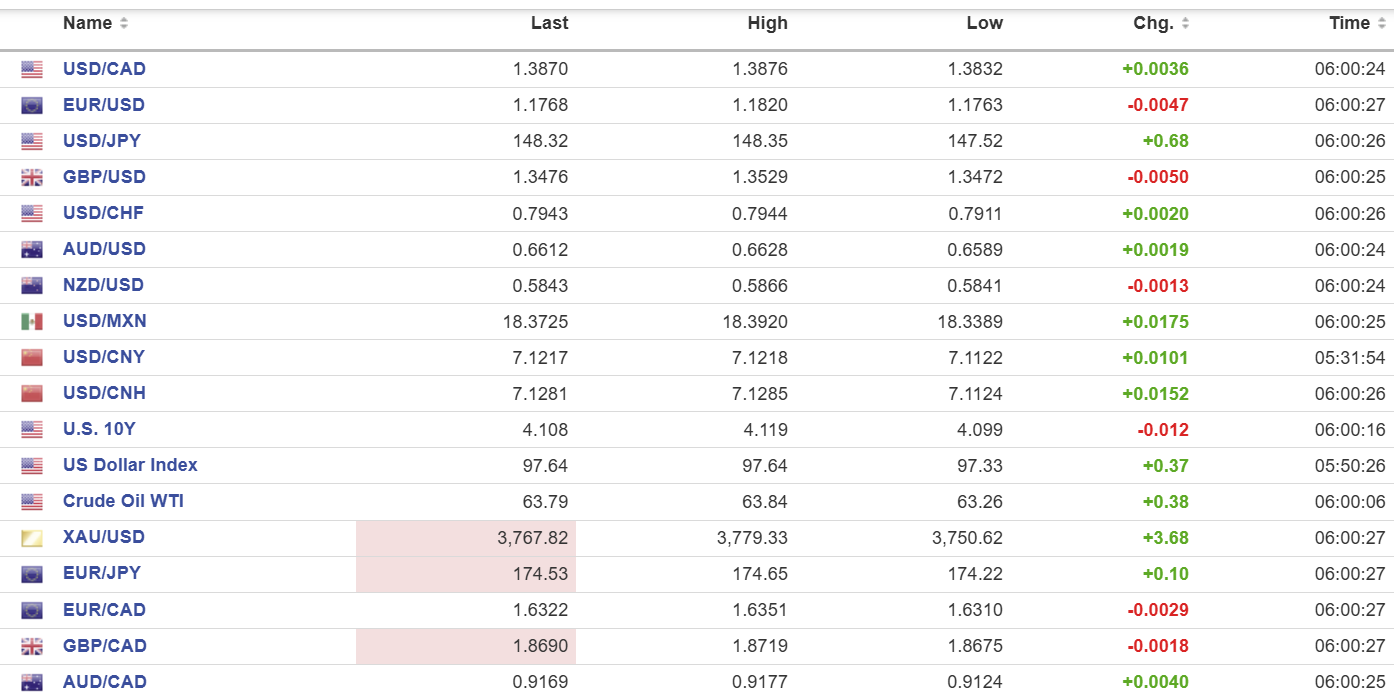

As of 7:30 am EDT, European equities are negative. The French CAC-40 index is down 0.45%, the German Dax has lost 0.10% and the UK FTSE 100 index has fallen by 0.13%. S&P 500 futures are bucking the trend and posting a gain of 0.19%. The US dollar index (DXY) is 97.73, after trading in a 97.33-97.75 range overnight. Gold (XAUUSD) is 3764.86 and the US 10-year Treasury yield sits at 4.119%.

EURUSD

EURUSD rallied defensively in a 1.1755-1.1820 range as another weak German Ifo survey offset any positive sentiment from yesterday’s PMI data. Traders have largely dismissed Trump’s comments that countries should shoot down Russian planes that violate NATO airspace. The Ifo Survey wrote, “Sentiment among companies in Germany has deteriorated. The Business Climate Index fell to 87.7 points in September, down from 88.9 points in August. In manufacturing, the index declined. Companies assessed their current situation as slightly worse, and expectations became more cautious. In the service sector, the business climate deteriorated noticeably.”

GBPUSD

GBPUSD is at the bottom of its overnight 1.3470-1.3529 range due to broad US dollar strength and a rather dour economic outlook courtesy of the Organization for Economic Co-operation and Development. The OECD predicts that the UK will have the highest inflation in the G-7 and slow economic growth due to a tighter fiscal stance.

USDJPY

USDJPY bounced in a 147.52-148.40 range which has contained prices all week. Prices rallied from the low on the heels of a disappointing Japanese Manufacturing PMI index which fell from 49.7 in August to 48.4 in September. The Composite Index rose to 51.1 compared to 52.0 previously. Gains were limited by ongoing concerns that the BoJ will be raising interest rates this year.

AUDUSD

AUDUSD rallied from its Asia low of 0.6589 to 0.6606 in Europe before sliding to 0.6606 in NY. The rally got a bit of support after inflation ticked up to 3.0% in August from 2.8% in July.

USDMXN

USDMXN is at the top of its 18.3389-18.3990 range due to broad based US dollar strength. Mexican inflation for the first half of September rose by 0.18% compared to -0.2% previously.

USDCNY

PBoC fix: 7.1077 vs exp. 7.1080 (Prev. 7.1057)

Shanghai Shenzhen CSI 300 rose 1.62% to 4566.07.

China pledges not to seek developing country privileges in future WTO dealings which is a rather magnanimous stand for the second largest economy in the world which is no longer “developing.”

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics