December 23, 2025

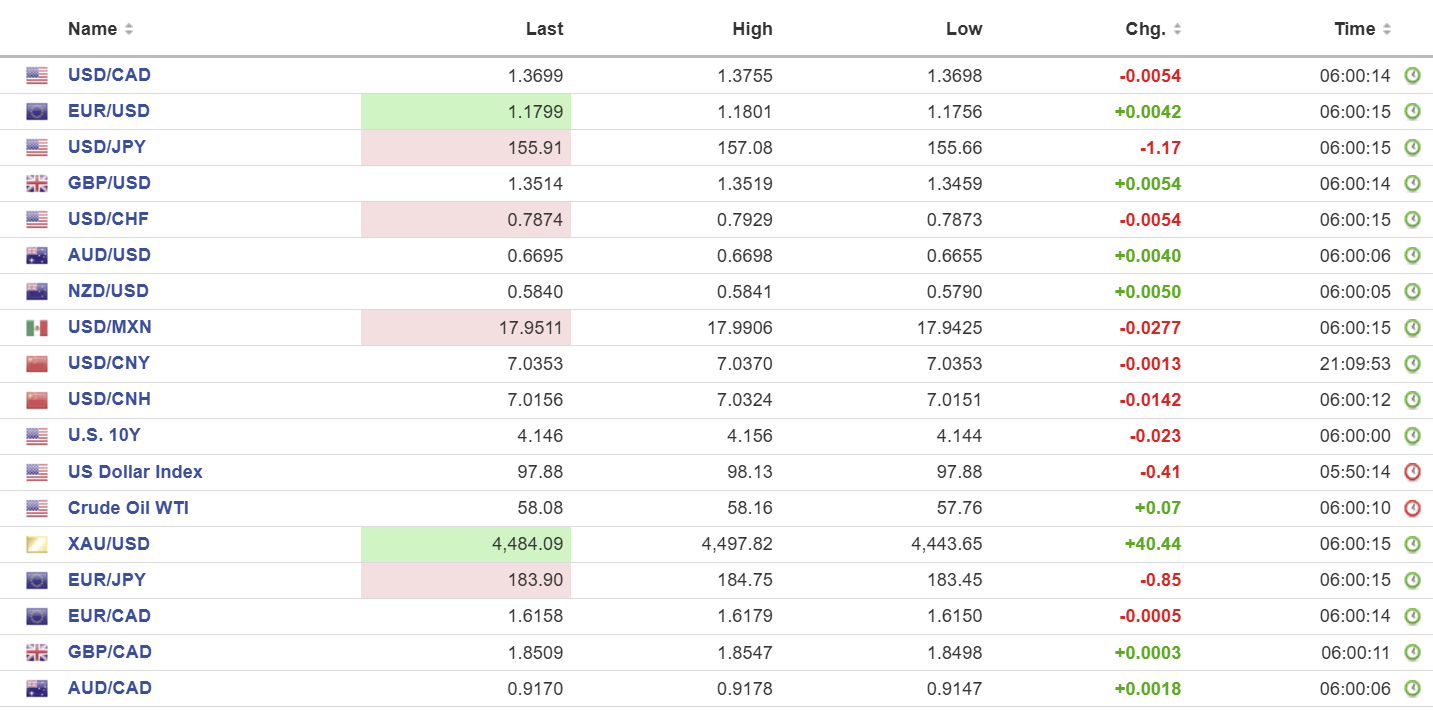

USDCAD open: 1.3699, overnight range 1.3689-1.3755, close 1.3747

Merry Christmas and Happy New Year. This is the final update of 2025, resuming January 5, 2026

USDCAD slid to levels last seen in July on the back of a sliding greenback, higher gold and steady oil prices in holiday-thinned markets. Shrinking CAD/US 10-year interest rate differentials are adding fuel to the sell-off. At -67.1 the spread is its narrowest in a year.

Today’s Canadian highlight, other the snow and freezing temperatures across much of the country was the release of October GDP data which dropped -0/3%, as expected. The postal strike and a teachers strike weighed on the results. Stats Canada expects November GDP will rebound to 0.1%.

WTI oil prices extended yesterdays gains in a 57.76-58.16 range. Prices remain bid as Trump continues to defend American national security by hijacking oil tankers with Venezuelan crude on the high sees, a term that used to be called piracy. The only difference is the flag flying from the American ships is the Stars and Stripes and not the Jolly Roger.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish and looking to break below support at 1.3680 to extend losses to 1.3610. However, the intraday RSI is oversold and failure to break support points to a retest of resistance at 1.3760.

The medium-term technicals are negative, confirmed by the break below the September uptrend line alongside the retreat below the 100 and 200-day moving averages. The downside target is 1.3600

For today, USDCAD support is at 1.3680 and 1.3630. Resistance is at 1.3750 and 1.3790

Todays Range 1.3640-1.3740

Data Today, But Only A Few Will Play

The US released a mass of mostly stale data. Q3 GDP rose 4.3% (forecast 3.3%) while Durable Goods Orders fell 2.2% (forecast -1.5%) The market reaction was muted as the Fed has already acted, and many traders have closed for the season.

Mean Girls

A bully always picks smaller, weaker victims, and Donald Trump is the quintessential bully. Perceived slights or insults are met with overwhelming force, backed by the might of the US government and tame, timid politicians. TV shows, news commentators, even comedians have faced his wrath. And the bully is flexing his muscles again. He has declared Greenland is essential for US security, Venezuela is needed for oil, and he just hates Canada. Greenlanders wish to remind America how they fared in Afghanistan, while Venezuelans are pointing to America’s success in Vietnam.

Taking Stock

Asian equity markets closed with gains. Japan’s Topix rose 0.64%, Hong Kong’s Hang Seng gained 0.43%, and Australia’s ASX 200 rose 0.91%.

As of 6:45 am, European bourses are trading mixed around flat. The German Dax is up 0.10%, while the French CAC-40 is down 0.22% and the UK FTSE 100 is flat. S&P 500 futures are nearly unchanged, the US Dollar Index is soft at 97.88, the US 10-year Treasury yield is 4.144%, and gold (XAUUSD) is 4491.07.

EURUSD

EURUSD rallied in a 1.1756-1.1801 range and is at the top of that band in NY. ECB Board member and noted hawk Isabel Schnabel warned that Eurozone rates could rise, but not in the foreseeable future.

GBPUSD

GBPUSD accelerated and rose from 1.3459 to 1.3515 on the back of broad-based US dollar weakness. Prices continue to be supported by the somewhat hawkish outlook for rates from the Bank of England and the Fed’s dovish bias.

USDJPY

USDJPY retreated from 157.08 to 155.66 on fears that the Bank of Japan may take advantage of thin FX conditions to intervene. Officials have been making noises about “excessive moves and one-side moves” almost daily, which traders have ignored. Japan’s Prime Minister rejected “irresponsible bond issuance,” saying the country’s debt was still too high.

AUDUSD

AUDUSD rose from 0.6655 to 0.6698, where it sits in NY, due to general US dollar weakness. Prices were also supported by the release of the minutes from the December 9 RBA monetary policy meeting, which were considered hawkish due to the discussion about the need for a rate hike to keep the economy in balance.

USDMXN

USDMXN dropped from 17.9906 to 17.9425 on renewed US dollar selling pressure vs the majors on increased odds that the Fed cuts rates again in January. The peso has gained 13% YTD, supported by expectations for a more cautious monetary policy approach by Banxico and a dovish pivot by the Fed.

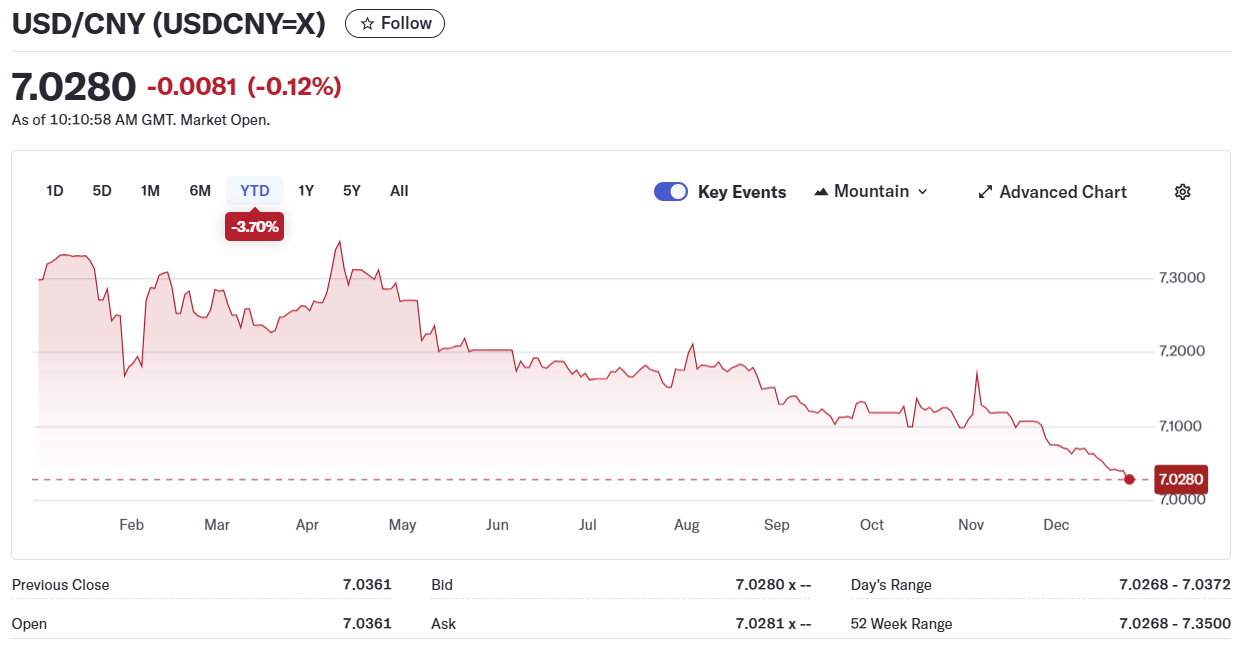

China

PBoC Fix: 7.0523 vs exp. 7.0267 (Prev. 7.0572)

Shanghai Shenzhen CSI 300 rose 0.20% to 4620.73

Russian LNG shipments to China rise 143% in November or 23.5% of China’s total imports.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics