February 2, 2026

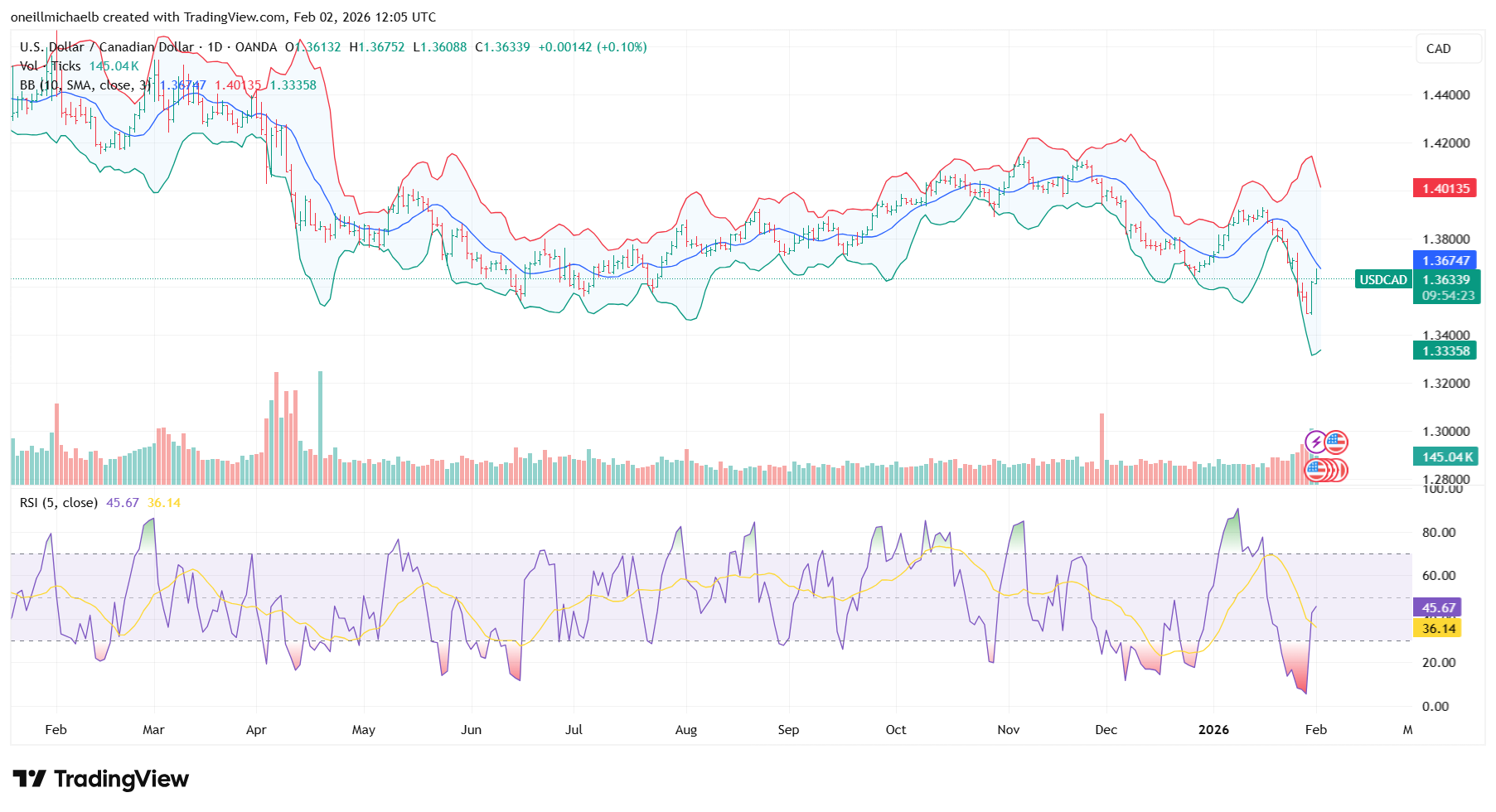

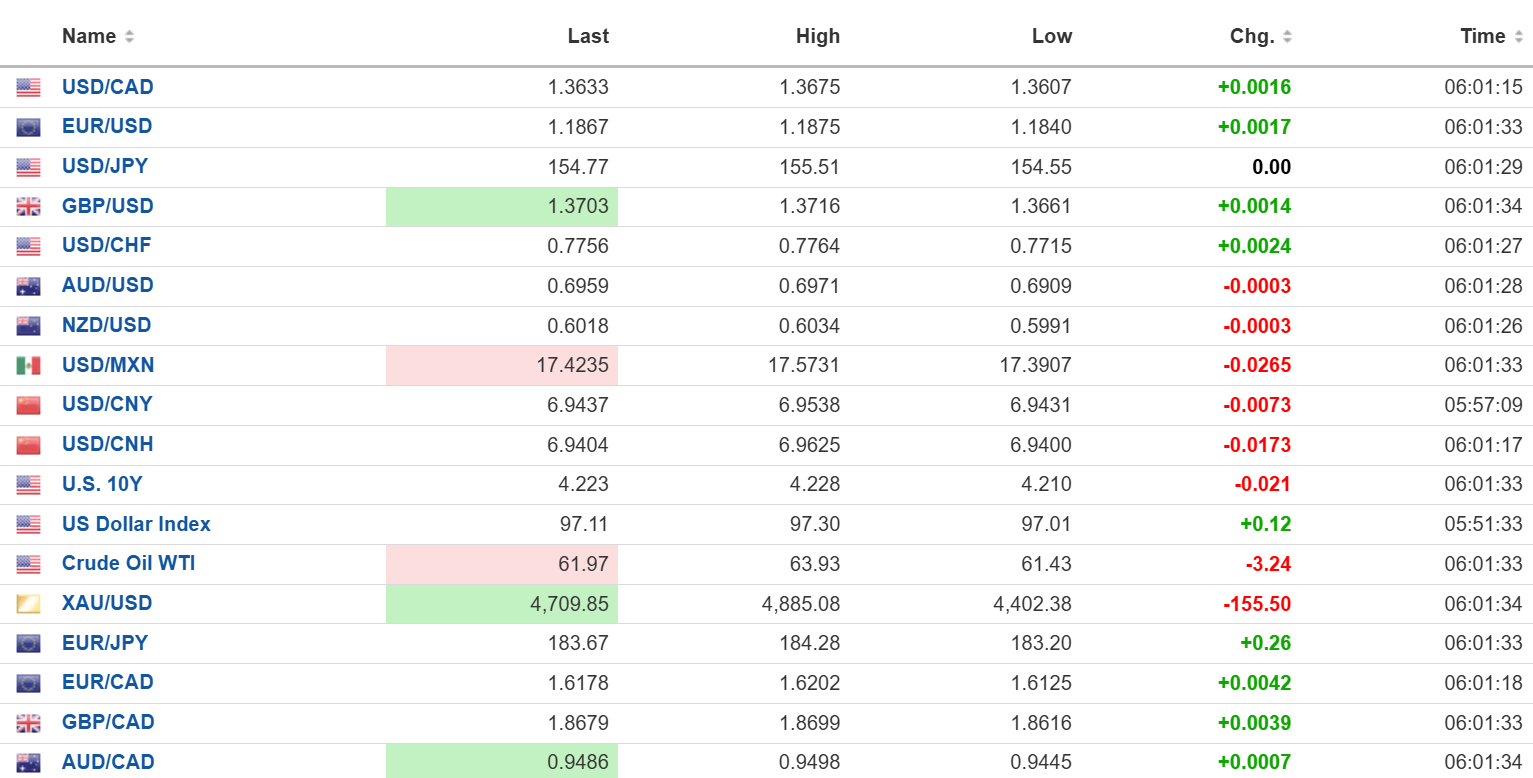

USDCAD open: 1.3633, overnight range 1.3607-1.3675, close 1.3618

USDCAD remains rather choppy after the latest bout of US dollar demand following Trump’s nomination of Kevin Warsh to replace Jerome Powell. The collapse in gold and silver prices also helped to reinforce the USDCAD floor at 1.3470.

Friday’s Canadian GDP data was not very impressive. Statistics Canada estimates that December GDP will come in at 0.1%. Uncertainty about Canada-US trade will continue to weigh on growth.

WTI oil retreated in a 61.43-63.93 range following reports that Iran and the US will meet later this week. Prices were also on the defensive due to the steep plunge in gold and silver prices. Opec’s decision to leave production quotas unchanged was expected and largely ignored.

US ISM Manufacturing PMI is expected at 48.3, compared to 47.9 in December.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish after prices failed to breach the January 19 downtrend line at 1.3670. that suggests’ Friday’s rally was merely a correction in an oversold environment. The hourly charts show a convergence of resistance in the 1.3660-1.3670 zone and only a decisive break above 1.3680 would negate the bearish trend.

The medium term techncials show that USDCAD has major support in the 1.3440-50 zone while 1.3680 should limit gain

For today, USDCAD support is at 1.3570 and 1.3550. Resistance is at 1.3670 and 1.3810

Today’s Range: 1.3570-1.3670

Traders See Trump’s Shadow-35.5 months more of turmoil

The shine is off gold and silver, with both metals dropping sharply before attempting to claw back losses in a volatile overnight session. Gold (XAUUSD) peaked at 5593.32 on Thursday and closed at 4865.35 on Friday. It continued to slide overnight, dropping to 4402.38 in Asia before drifting higher in Europe and reaching 4670.56 in early NY.

Silver (XAGUSD) dropped from Thursday’s peak of 121.31 to 71.40 today before bouncing to 80.68 in NY. Is it just a correction or the start of a new downtrend? As long as Trump is President, bet on a correction.

The precious metals turmoil, combined with the “is he a hawk or a dove” debate raging around Trump’s Fed Chair nominee Kevin Warsh, has undermined equities and provided some support to the greenback.

And then there’s AI. Nvidia announced plans to invest $100 billion in OpenAI last October. On Saturday, the WSJ reported that Nvidia Chairman Jensen Huang is having second thoughts. He now claims that the original $100 billion was not a binding commitment (and more like a Trump agreement). It was non-binding and never finalized.

Taking Stock

Asian equity markets finished deep in the red. The Hang Seng plunged 2.23%, the ASX 200 lost 1.02%, and the Topix fell 0.85%.

As of 5:40 am PT, the German DAX is up 0.72%, the French CAC-40 has gained 0.62%, and the UK FTSE 100 has risen 0.66%. S&P 500 futures are down 0.41%, the US Dollar Index is at 97.42, the 10-year Treasury yield is 4.244%, and gold (XAUUSD) is at 4715.43.

EURUSD

EURUSD is consolidating Friday’s losses in a 1.1824–1.1875 range and is trading near its session peak in NY. Eurozone manufacturing data was mixed. S&P Global wrote, “growth lacked vigour as new factory orders fell since December. Meanwhile, job losses were extended, and firms reduced their buying quantities, although the downturn in purchasing volumes was only marginal. Nevertheless, business confidence rose to its highest level since February 2022.”

Traders are less concerned about the data and are looking ahead to Thursday’s ECB monetary policy decision and whether recent euro strength is an issue.

GBPUSD

GBPUSD traded in a 1.3654–1.3716 band, with prices hitting the top after better-than-expected UK PMI data. Manufacturing PMI (actual 51.8) and business optimism reached 17-month highs. Prime Minister Starmer said his government will apply to join a multi-billion-euro EU defence fund.

USDJPY

USDJPY extended Friday’s rally and rose from 154.55 to 155.51 after a poll showed that Prime Minister Sanae Takaichi appeared to advocate a weaker yen. She extolled the benefits of a weaker yen but later walked back the comments. She said, “My intention was not to say whether yen appreciation or yen depreciation is good or bad, but to note that we want to build a strong economy that is resilient to exchange rate fluctuations.”

AUDUSD

AUDUSD traded defensively in a 0.6909–0.6971 range after being trashed when the greenback rallied on news of Kevin Warsh’s nomination for Fed Chair. Slumping commodity prices and mixed Chinese PMI data also weighed on prices. RBA monetary policy is expected to cut rates by 25 bps to 3.85% tomorrow, a view supported by the TD Inflation Gauge, which shows CPI rising to 3.6% y/y compared to 3.5% in December.

USDMXN

USDMXN is clawing back losses in a 17.3567–17.5731 range after the greenback rally stalled ahead of today’s US ISM Manufacturing PMI report.

China

PBoC Fix: 6.9695 vs exp. 6.9710 (Prev. 6.9678)

Shanghai Shenzhen CSI 300 fell 2.13% to 4605.98

NBS January Manufacturing PMI 49.3 (forecast 50, Dec. 50.1) Non-manufacturing PMI 49.4 (forecast 50.3, Dec 50.2)

RatingDog December PMI 50.3 (forecast 50.3, Dec 50.1)

Bloomberg quotes ANZ Banking group senior China analyst who argues that Based on various information, the top leadership is preparing to make more financial reforms. Policymakers could think that it’s a good timing right now because financial institutions have a strong consensus that the dollar is weakening.”

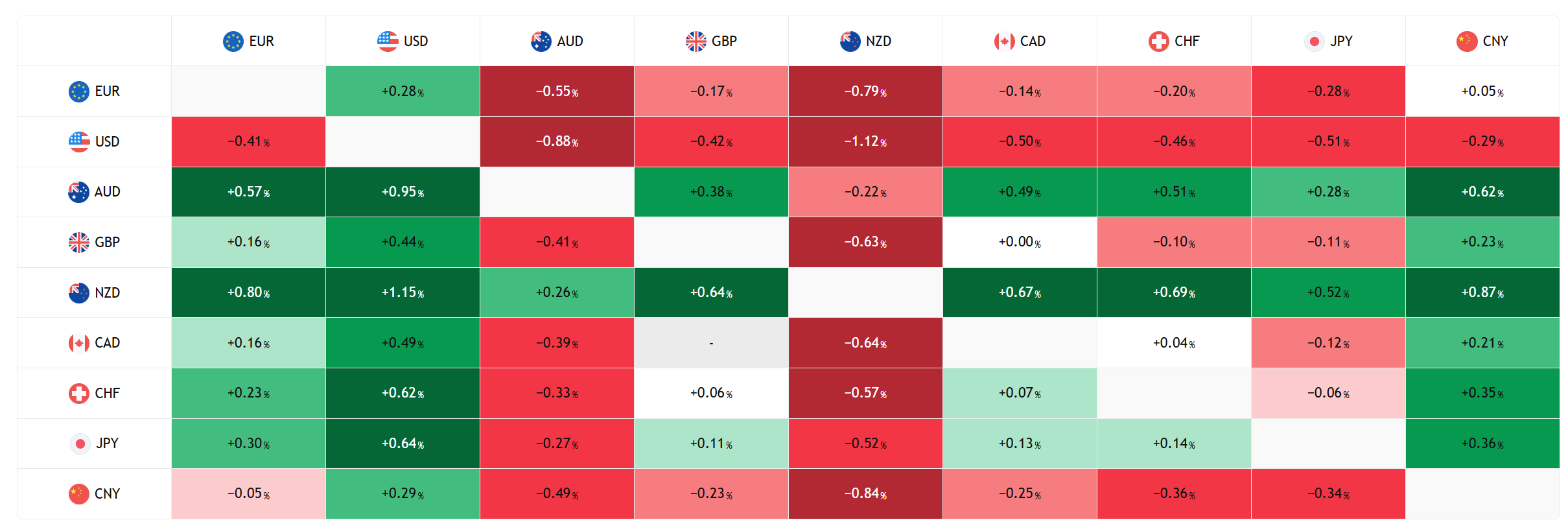

FX open high low

FX Heat Map (6:00 am) one week

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview