February 5, 2026

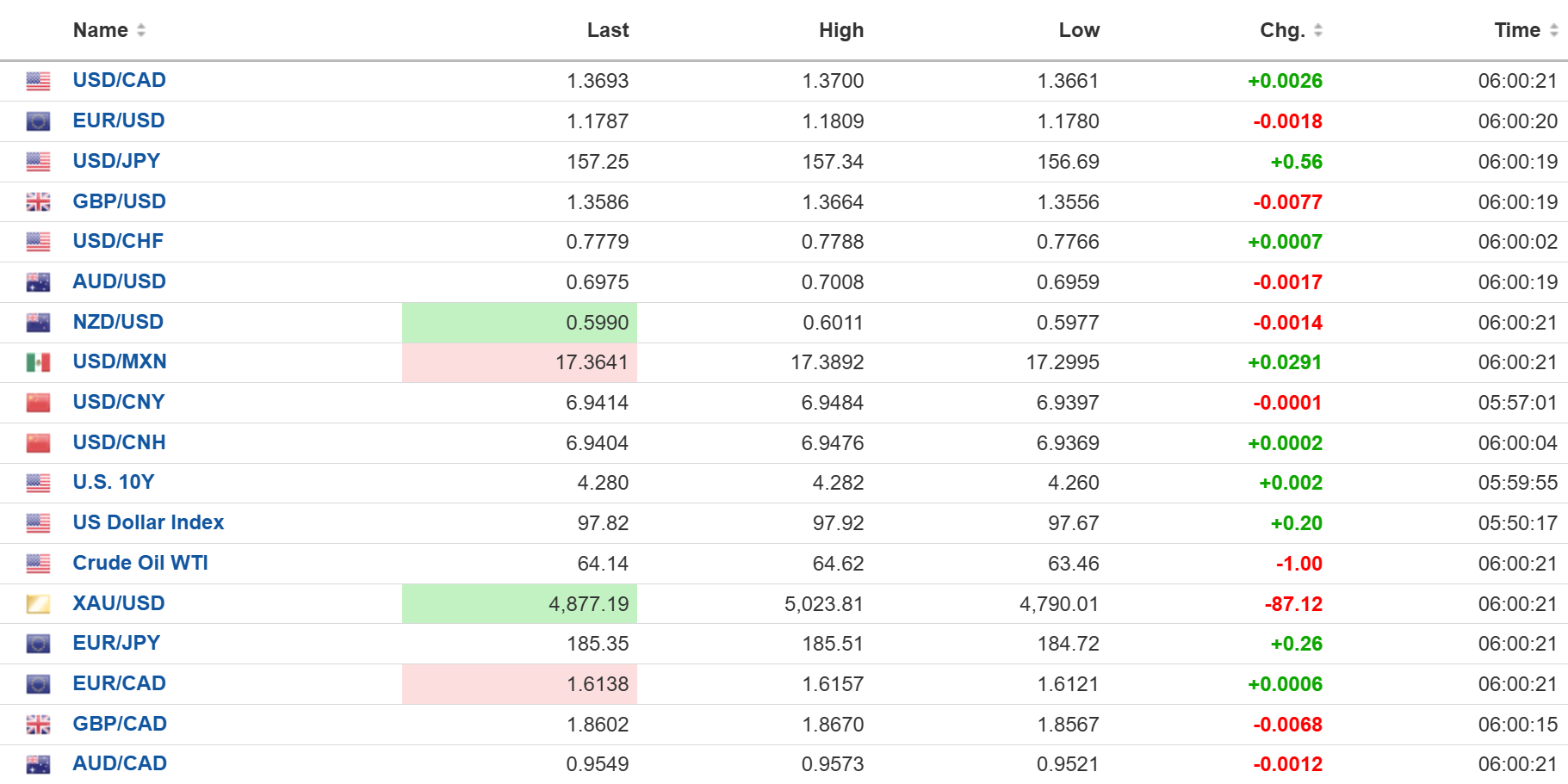

USDCAD open: 1.3693, overnight range 1.3661-1.3700, close 1.3664

USD/CAD traded firmer due to broad US dollar strength with a bit of commodity price weakness providing a bit of support.

The Federal government gave the auto industry a helping hand by announcing plans to scrap the zero-emissions vehicle mandate which forced car companies to build EV’s. They are also planning to reintroduce electric vehicle purchase rebates using funds from the magic money tree forest.

Bank of Canada Governor Tiff Macklem is slated to speak at Toronto’s Empire Club at 12:30 pm/ The speech is titled “Structural change – Canada at a crossroads.”

There are no Canadian economic reports today.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish while prices are above 1.3660, with a break of 1.3700 putting 1.3720 in play. A move below 1.3660 targets 1.3610.

The medium-term technicals suggest the rebound from 1.3500 is corrective rather than trend-changing while prices remain capped below 1.3880. However, sustained trade above the daily Bollinger mid-band near 1.3640 keeps near-term upside risks alive and leaves room for a test of 1.3800–1.3850.

For today, USDCAD support is at 1.3660 and 1.3620. Resistance is at 1.3720 and 1.3760.

Today’s Range: 1.3660–1.3740

Greenback Catches a Bid, Silver Tanks and Stocks Slide

The US dollar is chugging higher as global stocks tumble and the Epstein files threaten to take down the UK government. Greenback gains are powered by easing Middle East tensions, with Iran and the US set to hold talks in Oman today.

Silver (XAGUSD) took it on the chin due to improving risk sentiment and after hawkish comments by Fed Governor Lisa Cook, who argued that US rates need to remain elevated. Speculators were forced to close leveraged positions.

Trump had an “excellent” call with Chinese President Xi Jinping. Trump tweeted, “It was a long and thorough call, where many important subjects were discussed, including Trade, Military, the April trip that I will be making to China (which I very much look forward to!), Taiwan,” …yada yada yada. The SCMP said Xi told Trump that the Taiwan question was the “most important” issue.

Trump Confirms that Warsh is “His Man”

Any lingering thoughts that Fed Chair nominee Kevin Warsh is an interest rate hawk were kicked to the curb yesterday. Trump said that Warsh would not have been nominated if he had argued for higher rates. “If he came in and said, ‘I want to raise it,’ he would not have gotten the job, no.”

US Jobs Data in Spotlight

The BLS said that the nonfarm payrolls report, scheduled for Friday, will be released on February 11. Today’s Job Openings and Labor Turnover Survey (JOLTS) is expected to show an increase in job openings to 7.2 million from 7.146 million. Weekly Jobless Claims are expected to rise by 3,000 to 212,000.

Taking Stock

Asian equities closed lower except for the Hang Seng, which rose 0.14%. Australia’s ASX 200 lost 0.43% while Japan’s Topix was flat.

As of 5:30 PT, European bourses are in negative territory. The German Dax is down 0.76^, the French CAC 40 has lost 0.26% and the UK FTSE 100 index is down 0.45%. S&P 500 futures have dropped 0.52%, %, the US Dollar Index is at 97.73, the 10-year Treasury yield is 4.235%, and gold (XAUUSD) is at 4,861.10 after touching 5,023.81 overnight.

EURUSD

EURUSD chopped about in a 1.1780–1.1809 range and is at 1.1801 in NY following the ECB decision to leave rates unchanged at 2.0%, as expected. The statement said that the economy remains resilient despite challenges. German factory orders surprised to the upside, rising 7.8% m/m in December (forecast -2.2%), while Eurozone retail sales disappointed, rising just 1.3% y/y versus expectations for a 1.6% increase.

GBPUSD

GBPUSD dropped from 1.3664 to 1.35541 and is 1.3583 in NY, post BoE decision, when rates were left unchanged at 3.75% in a 5:4 decision. It is considered a “dovish hold” as Governor Andrew Bailey predicted UK inflation would hit its target ahead of schedule and said “there should be scope for further easing.

The ghost of Jeffrey Epstein fueled GBPUSD losses ahead of the BoE the losses and is haunting Prime Minister Starmer. He admitted knowing Peter Mandelson, was friends with Epstein before appointing him Amabassador to the US. Perhaps he thought it was “no big deal” because Trump also features prominently in the Epstein files and that the shared relationship would improve UK/US relations.

USDJPY

USDJPY added to this week’s gains, rising to 157.34 from 156.69. The gains are due to the belief that PM Sane Takaichi’s government will win a substantial majority in the February 8 election. If so, she plans to ramp up fiscal spending, which would make it difficult for the BoJ to raise rates.

AUDUSD

AUDUSD traded defensively in a 0.5977–0.6011 range and gave up all of its post-RBA rate hike gains. The drop was due to general US dollar strength and a fall in commodity prices. Australia’s trade surplus widened to 3.373 million, which was more than expected and well above the November surplus of 2.597 million.

USDMXN

USDMXN traded with a small bid, rising from 17.2995 to 17.3892 and is just above the middle of that band in NY. The gains were on the back of general US dollar demand. Banxico is expected to leave rates unchanged at 7.0% today because inflation remains sticky, but to keep the door open to future rate cuts.

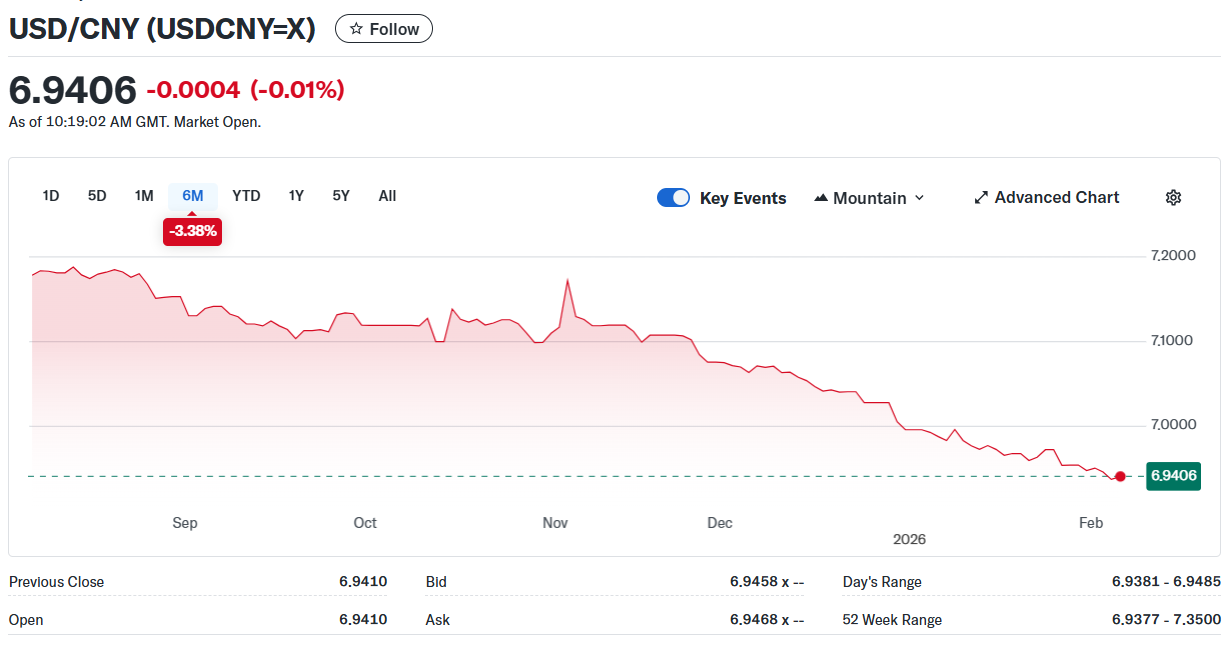

China

PBoC Fix: 6.9570 vs exp. 6.9468 (Prev. 6.9533)

Shanghai Shenzhen CSI 300 fell 0.62%% to 4670.42

FX open high low

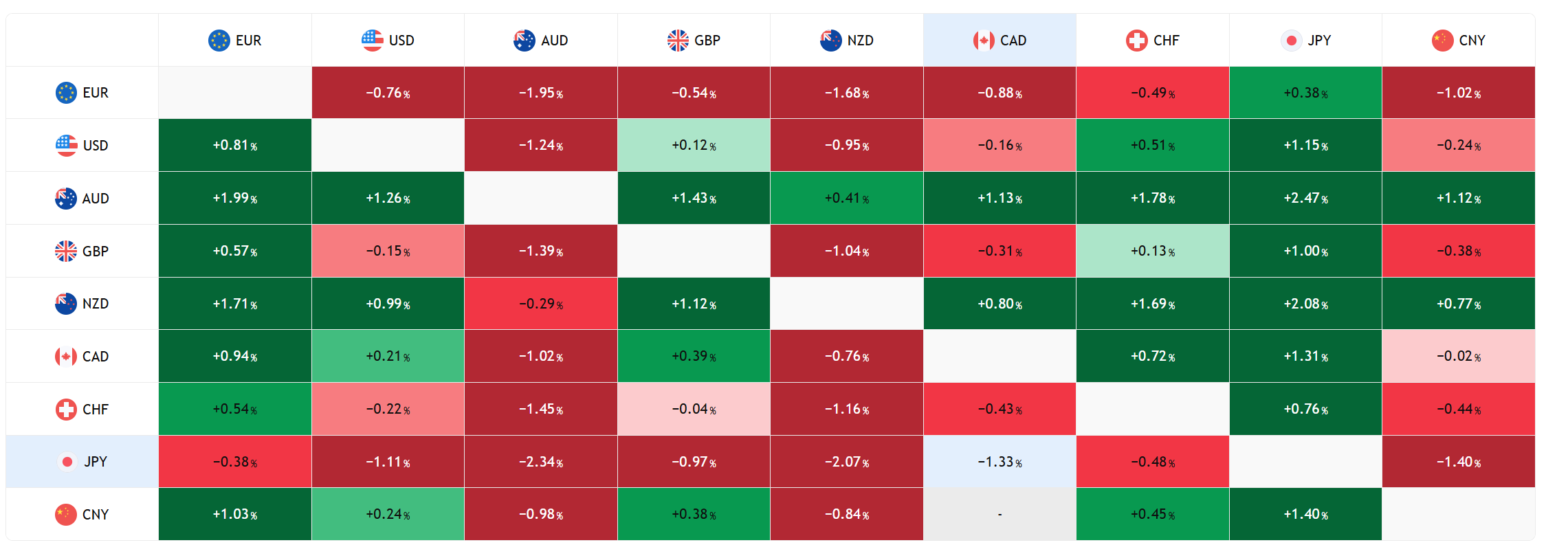

FX Heat Map (6:00 am) one week

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview