February 10, 2026

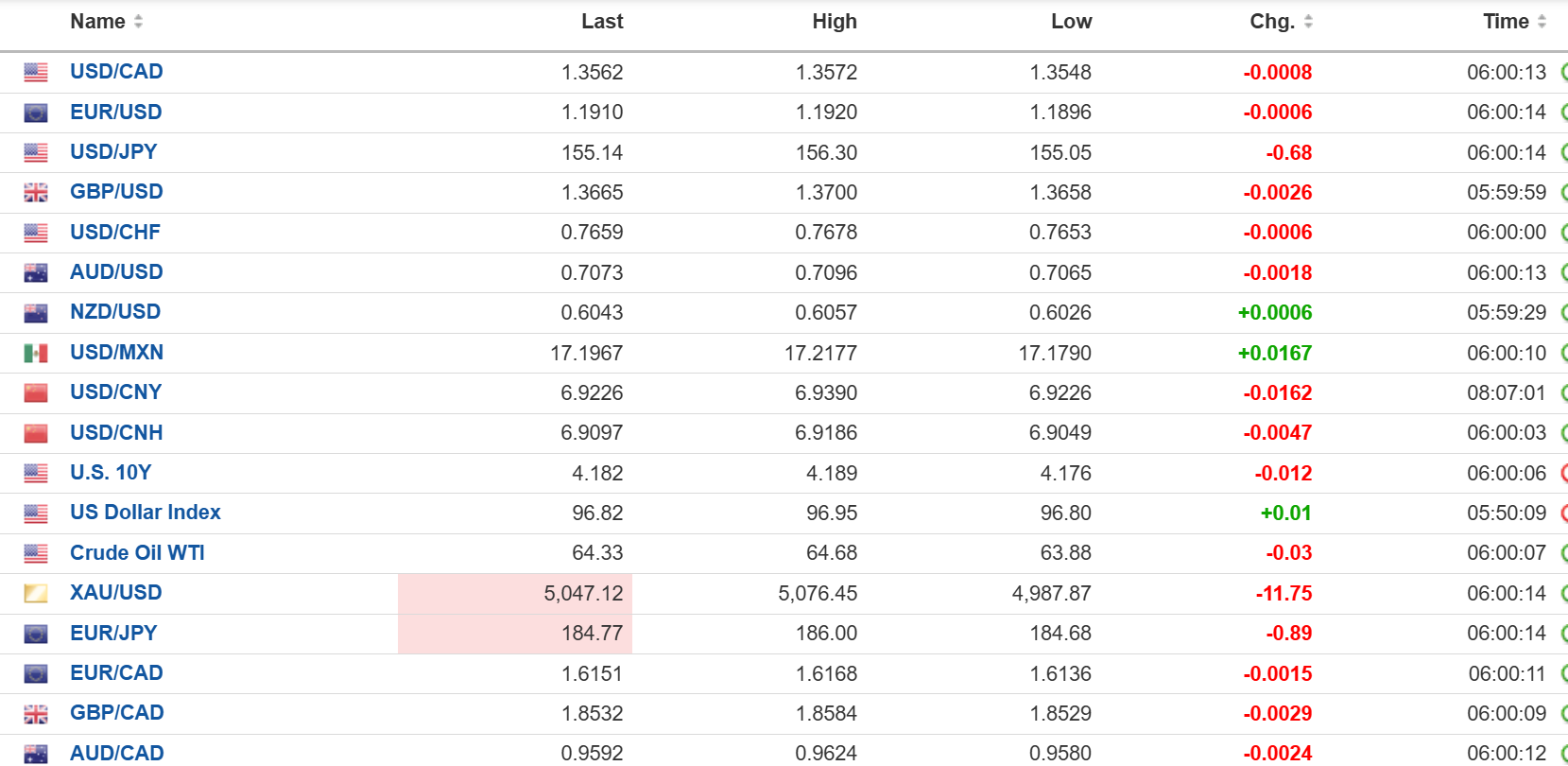

USDCAD open: 1.3562, overnight range 1.3548-1.3572, close 1.3558

USDCAD dropped yesterday and then traded sideways overnight. Traders shrugged off the latest drama and threats from the US and took heart from a report that German automakers are considering expanding in Canada. Earlier, Hyundai signed a memorandum of understanding about an auto manufacturing investment in Canada.

But the focus is not domestic-it’s American and the dollar-debasement trade. There is no shortage of articles suggesting foreign investors are divesting of US treasuries while hedge funds are loading up on short positions in US stocks. China told its domestic banks to curb exposure to Treasuries.

Yesterday, the Bank of Canada released its Q4 Markets Participants Survey. It painted a picture of the Canadian economy stuck in low gear rather than heading for either boom or bust. Growth is expected to hover around 1.5–2 percent through 2027. Inflation is seen settling comfortably near the Bank of Canada’s 2 percent target, removing price pressures as a policy constraint. As a result, interest rates are expected to remain unchanged through 2026, with only a gradual normalization thereafter.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish while prices are below 1.3615, with downside momentum still dominant after the recent breakdown. Failure to reclaim 1.3615–1.3630 keeps pressure on 1.3520, with a break lower exposing 1.3480. A recovery back above 1.3615 would ease immediate downside pressure and allow a corrective push toward 1.3660.

The medium-term technicals suggest the late-2025 rally has fully unwound. With USDCAD trading well below the 100-day (1.3886) and 200-day (1.3824) moving averages, the broader bias remains lower. While prices are below 1.3770, a decisive break under 1.3480 would target the lower Bollinger band near 1.3410.

For today, USDCAD support is at 1.3520 and 1.3480. Resistance is at 1.3615 and 1.3660.

Today’s Range: 1.3480–1.3510

Managing Jobs Data Expectations.

The US dollar is starting todays NY session on a mixed note, but it remains under pressure on concerns about a weak to ugly employment report tomorrow. That’s because White House economic adviser Kevin Hassett hinted as much. He said, “I think that you should expect slightly smaller job numbers that are consistent with high GDP growth right now. One shouldn’t panic if you see a sequence of numbers that are lower than you’re used to, because, again, population growth is going down and productivity growth is skyrocketing.” The consensus forecast for NFP is 70,000 compared to 50,000 in December.

US December retail sales were soft (actual 0.0% vs forecast 0.4%) and the employment cost index (Q4), dipped to 0.7% from 0.8%.

Taking Stock

Asian equities were mixed. Japan’s Topix surged 1.90%, Hong Kong’s Hang Seng rose 0.58%, and Australia’s ASX 200 closed flat.

As of 5:45 am PT, European bourses have given up earlier gains and are trading flat to negative. The UK FTSE 100 is down 0.46%, the German DAX is down 0.15% and the French CAC 40 and S&P 500 futures are up flat. The US Dollar Index is at 96.84, the 10-year Treasury yield is 4.159%, and gold (XAUUSD) is 5053.00.

EURUSD

EURUSD traded narrowly in a 1.1896–1.1920 range as it consolidates yesterday’s gains. The single currency is being underpinned by speculation of a weak US nonfarm payrolls report tomorrow, dovish comments from FOMC members, and talk of hedge funds and sovereign wealth funds selling US Treasuries and the US dollar. EURUSD is bullish above 1.1860 and looking for a break above 1.1960 to extend gains to 1.2050.

GBPUSD

GBPUSD climbed in a 1.3658–1.3700 range on broad US dollar weakness. UK political tensions eased somewhat after a number of Labour ministers voiced support for Prime Minister Starmer. Mr. Starmer did not know Epstein, but he was caught up in the muck because he appointed Peter Mandelson as UK Ambassador to the US and knew that Mandelson was tainted. GBPUSD needs to decisively break above 1.3705 or else risk a retest of 1.3580.

USDJPY

USDJPY retreated in a 155.05–156.30 range. Traders are now thinking that Prime Minister Sanae Takaichi’s fiscal stimulus plans will boost the economy and, if that’s the case, it would enable the BoJ to raise interest rates.

AUDUSD

AUDUSD consolidated yesterday’s gains in a 0.7065–0.7096 range. A hawkish outlook for RBA monetary policy, the rising CNY, and firm commodity prices are underpinning prices. NAB business confidence ticked up to 3 in January (December 2) while business conditions dipped to 7 from 9.

USDMXN

USDMXN traded sideways in a 17.1790–17.2177 range after dropping from 17.2819. The losses stemmed from lingering improved risk sentiment after global stocks recovered from losses last week, and firmer headline inflation yesterday (January 0.38% vs previous 0.28%), which validates Banxico’s decision to pause rate cuts.

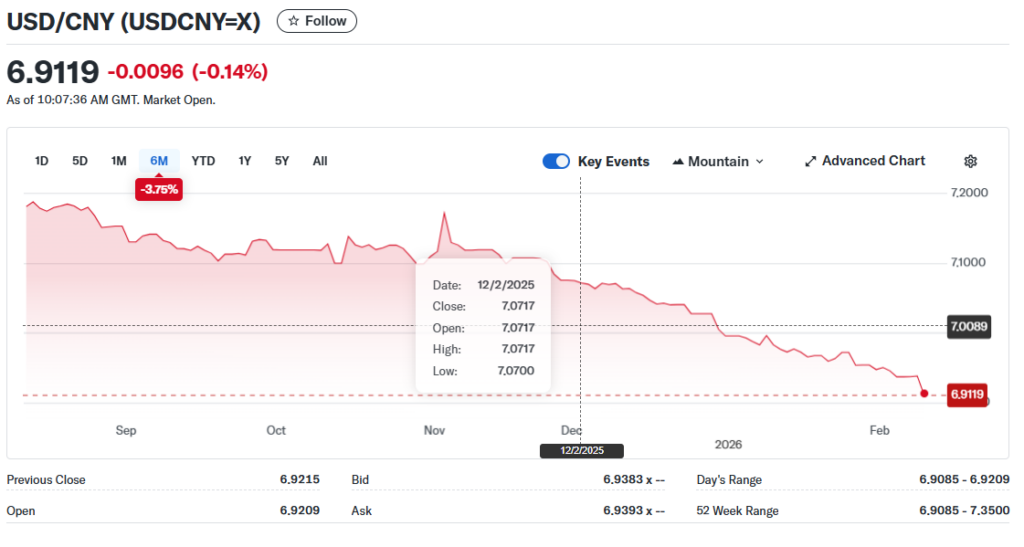

China

PBoC Fix: 6.9458 vs exp. 6.9135 (Prev. 6.9523)

Shanghai Shenzhen CSI 300 rose 0.11% to 4724.30

Trump and President Xi Jinping reportedly meeting in the first week of April.

FX open high low

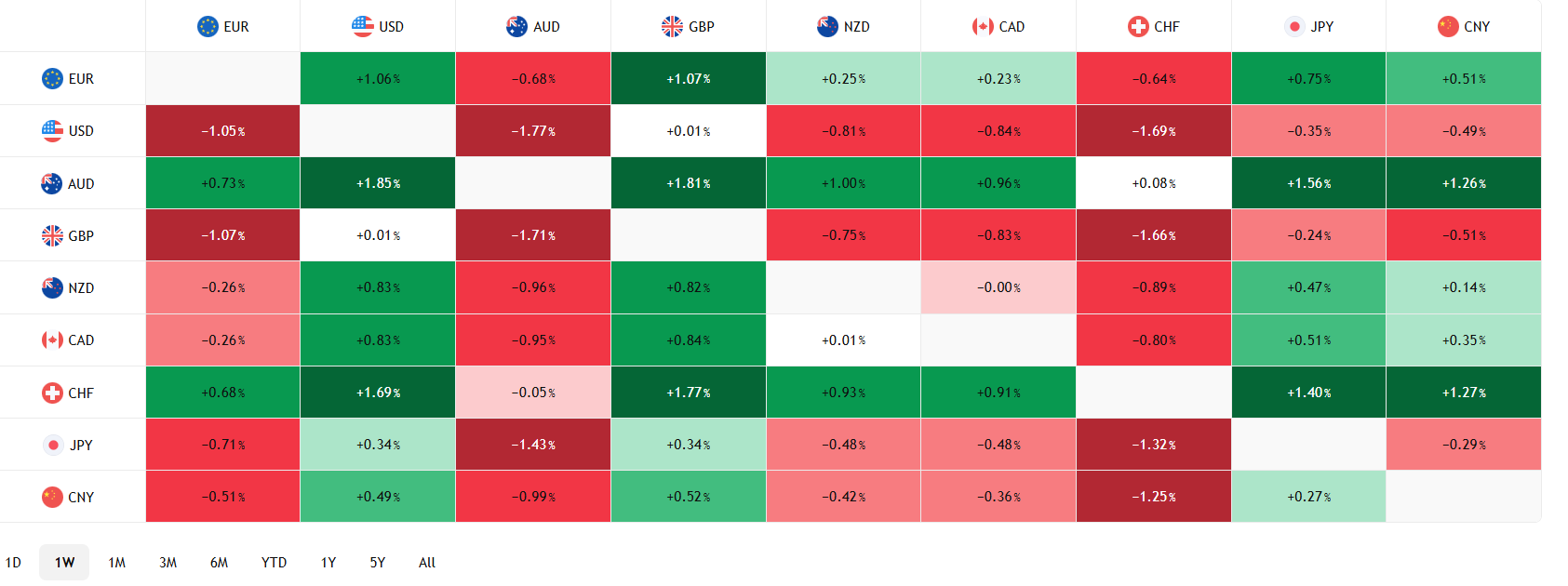

FX Heat Map (6:00 am) one week

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview