February 24, 2026

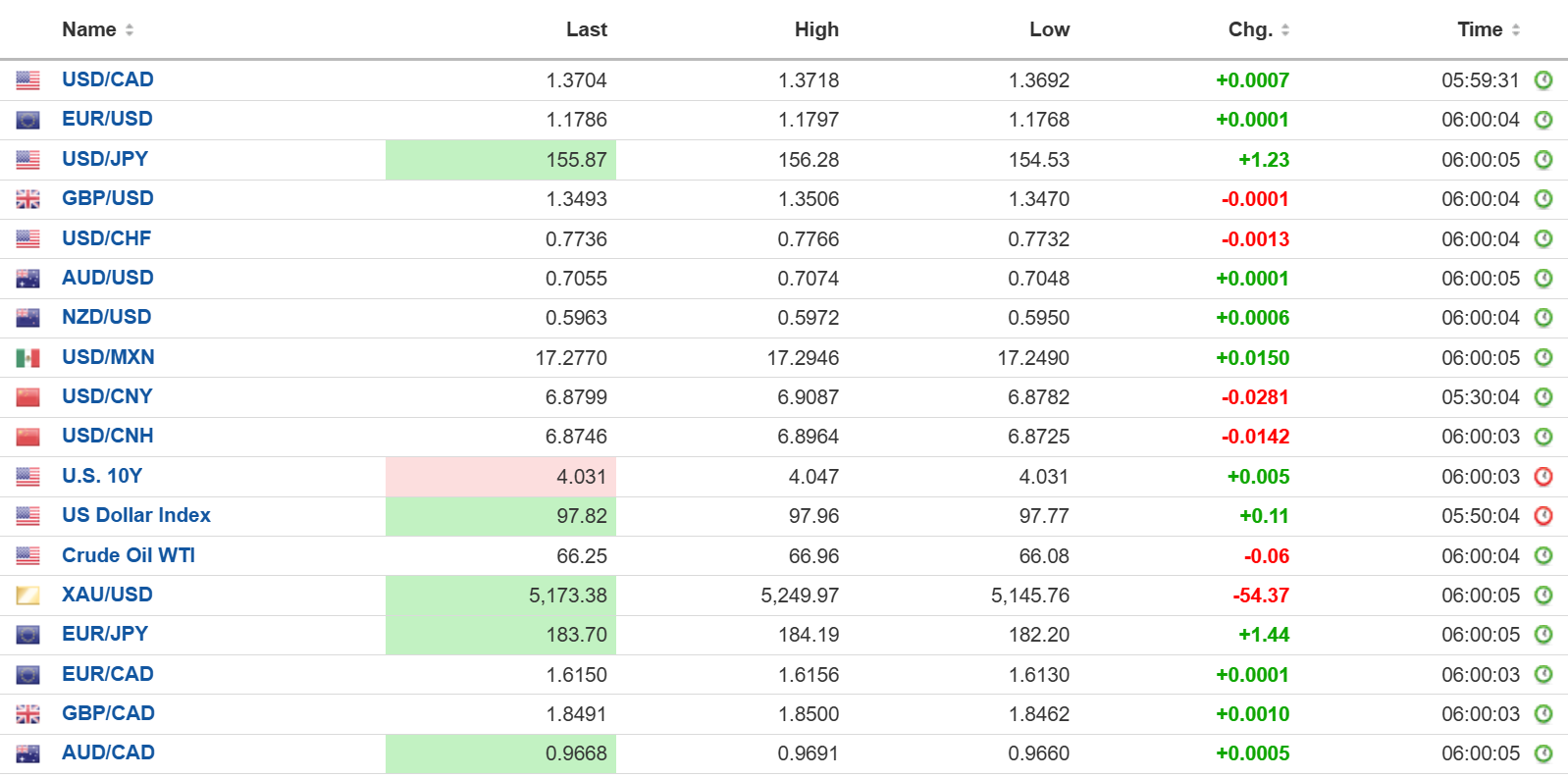

USDCAD open: 1.3704, overnight range 1.3692-1.3718, close 1.3698

USDCAD rallied yesterday as risk sentiment soured due to the AI-related tech stock meltdown on Wall Street. The gains were supported by the recent spate of soft Canadian economic data, which some analysts suggest, could force the Bank of Canada to trim rates. However, Macklem’s recent comments suggest such a move is unlikely. Domestic drivers for the currency pair are in short supply.

WTI oil prices remained bid and traded in a 66.06-66.96 range. Traders are awaiting the results of the next round of nuclear talks scheduled Thursday.

The dearth of actionable US and Canadian economic data leaves tariff news and equities to drive USDCAD direction.

USDCAD Technical Outlook and blizzard warning

The intraday USDCAD technicals are bullish while trading above 1.3650 and is targeting a break above 1.3730 for a test of the 1.3780–1.3800 resistance zone. However, momentum is stretched, with the fast RSI near extreme overbought territory. A break below 1.3650 would shift focus back to 1.3550.

The medium-term technicals are bearish below 1.3780 leaving prices trapped within a 1.3480-1.3780 band. A break below 1.3550 would reopen downside risk toward 1.3400, while a sustained break above 1.3800 would argue for a move toward 1.3900 and potentially 1.4000.

For today, USDCAD support is at 1.3680 and 1.3650. Resistance is at 1.3740 and 1.3780.

Today’s Range: 1.3670–1.3750

Tariffs and Black Swans

Today is the day that Trump’s latest tariff barrage takes place. The 15% levy that he announced on the weekend is actually 10% today but “probably going up to 15%.” Confused? So is the Trump administration. Democrats have introduced legislation that would require Trump to fully refund all illegal tariff revenue, plus interest, within 180 days. FedEx went a step further and filed a lawsuit in the US Court of International Trade seeking a refund.

Then there was the talk of a Black Swan. Nassim Taleb, the man who coined the term for a rare, unpredictable occurrence, warned that markets were underpricing structural risks while overstating the durability of the AI rally. That story crushed Wall Street and underpinned the US dollar.

Can We Talk?

Silence may be golden, but not today. A slew of Fed officials will be discussing their monetary policy outlooks. Chicago Fed President Austan Goolsbee, Atlanta Fed President Raphael Bostic, Boston Fed President Susan Collins, along with Governors Christopher Waller and Lisa Cook, are on tap.

The marquee event is Trump’s “Look How Great I Am” (formerly known as the State of the Union address) tonight. It is a no-brainer to expect something that is long on hyperbole, short on facts, and largely devoid of reality.

Taking Stock

Asian equity markets closed on a mixed note. China returned from its Lunar New Year holiday, and the Shanghai Shenzhen CSI 300 index rallied 1.01%. Hong Kong was roiled by fallout from Wall Street’s losses sparked by AI disruption fears and closed down 1.81%. Japan’s Topix rose 0.20%, while Australia’s ASX 200 closed flat.

As of 5:30 am PT, the French CAC-40 is up 0.15%, the German DAX is down 0.13% and the UK FTSE 100 is unchanged. S&P 500 futures are up 0.08%, the US Dollar Index is 97.93, the 10-year Treasury yield is 4.04%, and gold (XAUUSD) is 5,145.05

EURUSD

EURUSD is trading defensively in a 1.1768–1.1797 range due to renewed US and EU trade frictions. EU officials view Trump’s latest 10% tariff announcement as a breach of the US–EU trade deal and, for the time being, have put ratification on the back burner.

GBPUSD

GBPUSD traded quietly in a 1.3470–1.3506 range. Traders are hoping for clues to the March rate decision from BoE policymakers’ testimony to Parliament today. They are also digesting how the new tariff regime may impact sterling.

USDJPY

USDJPY surged from Monday’s close of 154.66 to 156.28. The rally was sparked by a report that Prime Minister Sanae Takaichi expressed reservations about rate hikes when she spoke to BoJ Governor Kazuo Ueda last week. The story is unverified but, if true, throws a monkey wrench into the monetary policy debate.

AUDUSD

AUDUSD consolidated yesterday’s losses in a 0.7048–0.7074 range. Prices remain underpinned by favourable Australian interest rates, currently 3.85%, and expectations that the RBA will raise rates again. However, that outlook may change tomorrow if domestic inflation cools as expected, with forecasts at 3.7% versus 3.8%.

USDMXN

USDMXN climbed steadily overnight, rising from 17.2490 to 17.2946 and trading near the middle of that band in early New York dealing. US equity market weakness on fresh AI disruption chatter fuelled risk aversion, overshadowing yesterday’s better-than-expected Q4 GDP growth of 1.8% year over year versus a 1.6% forecast.

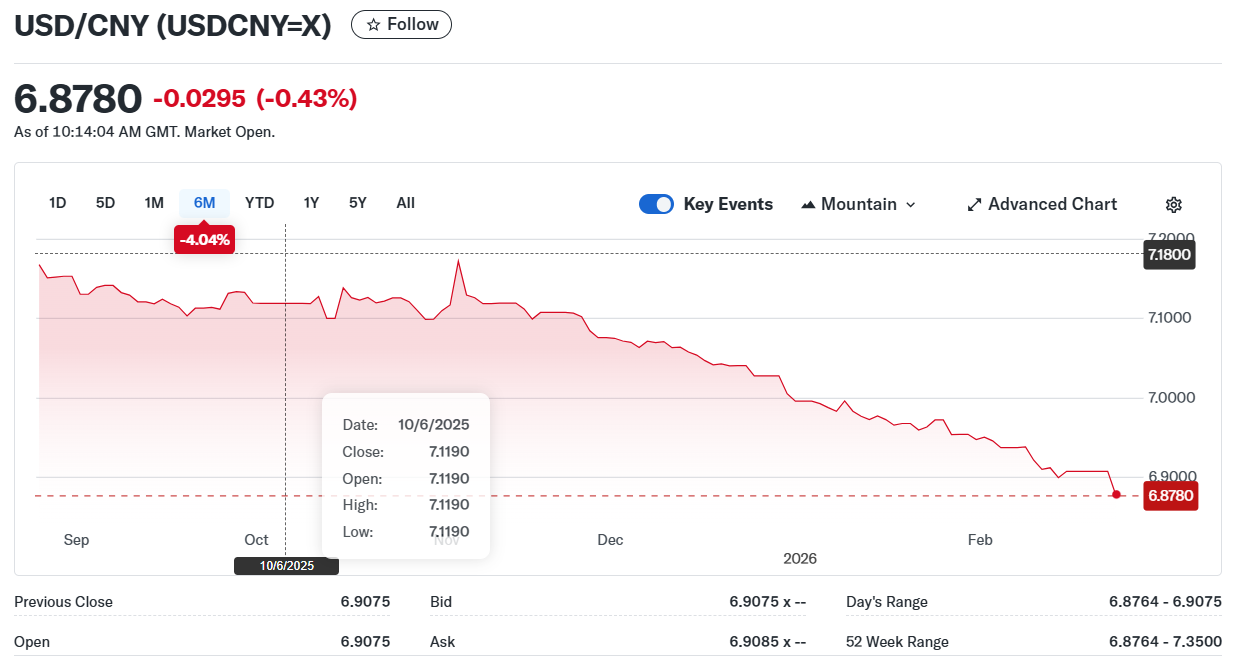

China

USDCNY Fix: 6.9414 vs exp. 6.9249 (Prev. 6.9398)

Shanghai Shenzhen CSI 300 rises 1.01% to 4707.54

The PBoC left its 1- and 3-year Loan Prime Rate (LPR) unchanged at 3.0% and 3.5% as expected. It is the 10th month in a row where rates have been left unchanged.

China adds Japanese companies to export control list claiming that they have ties to Japan’s military.

Consumer spending during Lunar New Year rose modestly. Japanese visitors to Japan fell by 50% with Thailand and South Korea becoming preferred destinations.

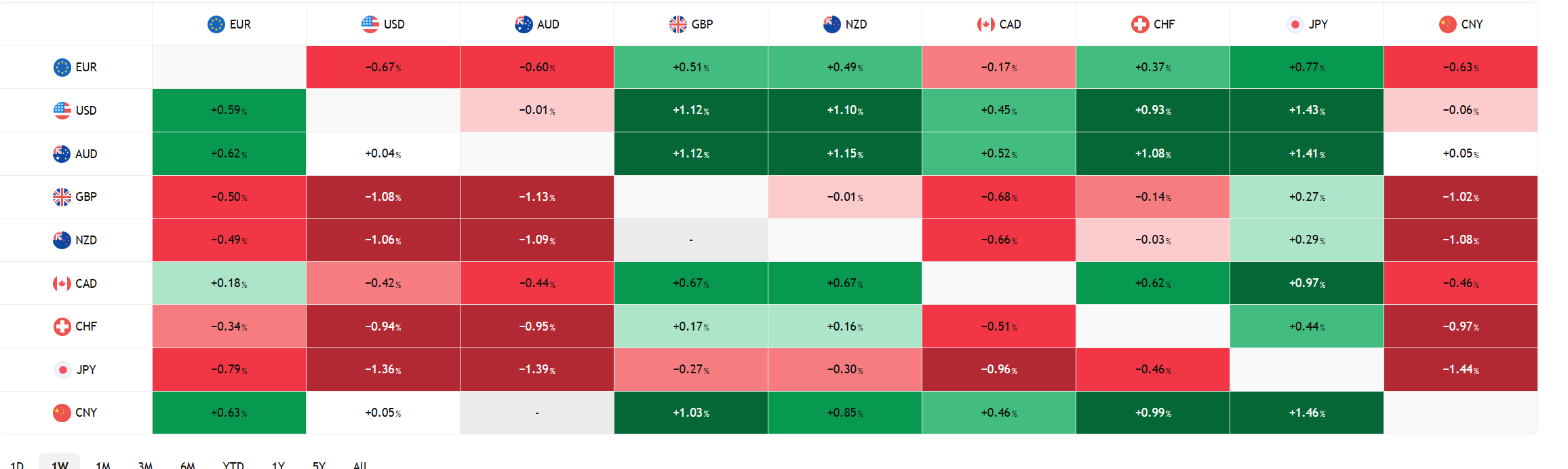

FX open high low

FX Heat Map (6:00 am) one week

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview