July 15, 2025

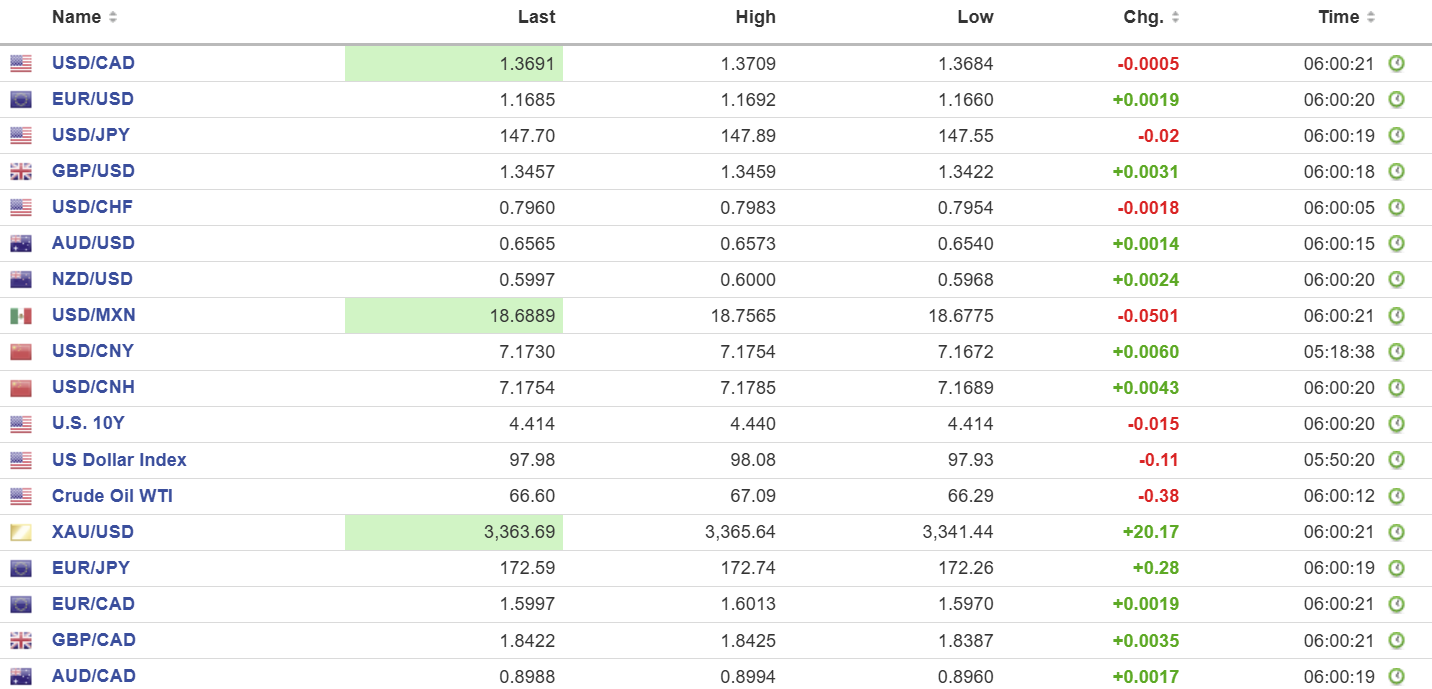

USDCAD open 1.3691, overnight range 1.3694-1.3709, close 1.3706

USDCAD traded narrowly and inside yesterday’s range overnight but dipped to 1.3677 post- US and Canada inflation reports.

In terms of Trump’s trade war, the US dairy industry may end up a winner. They are demanding that Canada remove protectionist supply management barriers that are designed to protect Quebec’s dairy industry at the expense of Canadian consumers.

Canada’s June inflation rose 1.9%, as expected (previous1.7% y/y) and just 0.1% m/m as expected, from 0.6% previously. The results did not make the BoC’s monetary policy decision any easier but with Trump’s August 1 tariff deadline, the BoC is sure to leave rates unchanged on July 30.

WTI oil prices peaked at 69.63 yesterday after Trump threatened more sanctions on Russia and countries buying Russian crude. They started falling after they discovered that the sanctions did not come into effect for 50 days and continued to fall overnight, dropping from 67.09 to 66.29.

USDCAD Technical Outlook:

The intraday technicals are mildly bearish after rejecting gains above the June downtrend line at 1.3710 and are looking to test the uptrend support line at 1.3660, which has contained downside moves for the past week.

A break above 1.3710 targets 1.3760 then 1.3800 while a move below 1.3660 suggests a retest of 1.3610 then 1.3550.

For today, USDCAD support is 1.3650 and 1.3620. Resistance is 1.3710 and 1.3750. Today’s Range 1.3640-1.3740

US Inflation Data

US CPI is 2.7% in June, as expected, compared to 2.4% y/y in May. Meanwhile Core-CPI rose 0.2% m/m, less than expected compared to but a tick higher than the 0.1% seen in June. Analysts are suggesting that the reason tariffs aren’t being reflected in the data is due to margin compression. Companies front-loaded purchases ahead of the tariffs and price increases have not trickled down to the end user.

Taking Stock

Asian equity traders were in a positive mood and the major indices closed higher. China’s GDP data helped lift the Hong Kong Hang Seng to a 1.60% gain, while dialed-back tariff rhetoric fueled gains in Australia’s ASX 200 (0.70%) and Japan’s Topix (0.09%).

European indices are in positive territory ahead of today’s US inflation report. The German Dax is up 0.19%, the French CAC 40 index has gained 0.11%, and the UK FTSE 100 is unchanged (as of 6:44 am). S&P 500 futures are up 0.44%. The US 10-year Treasury yield is 4.412%, while gold (XAUUSD) trades at 3362.23.

EURUSD

EURUSD traded in a 1.1660-1.1692 range due to concern around EU/US tariff talks and caution ahead of today’s US inflation numbers. EURUSD garnered a bit of support from a modestly better ZEW Survey and higher Eurozone Industrial Production data for May. The July downtrend remains intact while prices are below 1.1710.

GBPUSD

GBPUSD is on the defensive and traded in a 1.3422-1.3460 range, in part due to EURGBP demand due to short-term EURGBP interest rate spreads. Traders are concerned that UK rates may have to be cut faster than previously anticipated. A decisive break below 1.3390 targets 1.3150.

USDJPY

USDJPY rallied yesterday and consolidated the gains in a 147.55-147.88 range. The currency is underpinned by rising expectations that the BoJ will not be raising rates any time soon and Japanese political uncertainty. Prime Minister Shigeru Ishiba may lose his majority in Upper House elections on the weekend.

AUDUSD

AUDUSD rallied in a 0.6540-0.6573 range after Trump’s weekend tariff threats were downgraded to “just more noise.” Prices also saw a bit of support from better-than-expected China GDP data.

NZDUSD

NZDUSD traded firmer, rising from 0.5968 to 0.6000 on another shift in tone with Trump’s EU tariff threats and modest but broad-based US dollar selling pressure.

USDMXN

USDMXN consolidated yesterday’s gains in an 18.6775-18.7565 range with prices near the bottom of the band in early NY ahead of the US inflation data today.

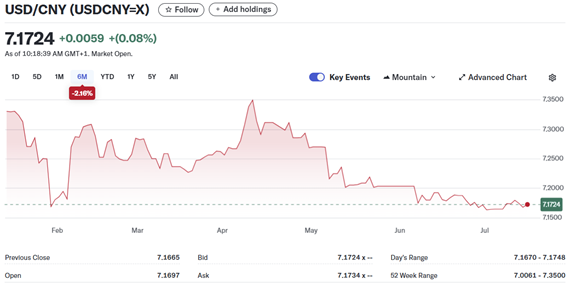

USDCNY

PBoC fix: 7.1498 vs exp. 7.1758 (Prev. 7.1491)

Shanghai Shenzhen 300 rose 0.03% to 4019.06

Q2 GDP 1.1% q/q (forecast 0.9%, previous 1.2%), Q2 GDP 5.2% y/y (forecast 5.1%, previous 5.4%)

Retail Sales 4.5% y/y (forecast 5.6%, previous 6.4%)

China’s economy showed resilience in the face of Trump’s tariff war, although Q2 data was bolstered by tariff-frontrunning.

The US Department of National Defence is challenging China’s rare earth supremacy. China’s grip on the market is due in part to its control of prices for the rare earth minerals. Those prices are artificially low to discourage alternative investments. The Defence Department announced it would pay a guaranteed minimum of 2X the current price for its sole domestic miner, MP Minerals.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance