July 30, 2025

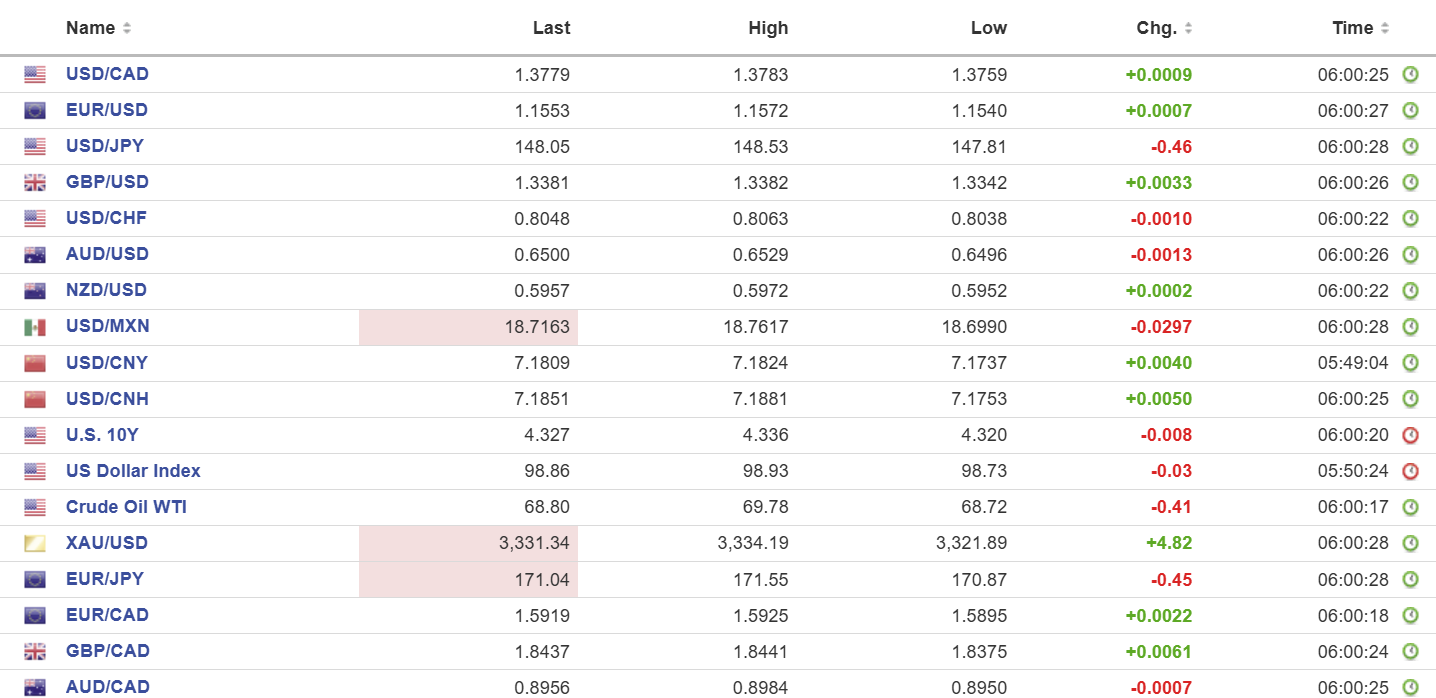

USDCAD open 1.3779, overnight range 1.3759-1.3791, close 1.3772

USDCAD is bid ahead of today’s Bank of Canada and FOMC monetary policy decisions. Neither bank is expected to lower interest rates.

BoC policymakers are handcuffed due to Trump’s looming August 1 tariff deal deadline.

Without another pause, tariffs on non-USMCA exports to the US will jump to 35%. The BoC releases its quarterly MPR today.

WTI traded in a 68.47-69.78 range as it consolidated gains following Trump reducing his deadline for Russia to agree to a ceasefire to just 10 days (as of today). US weekly crude inventories rose by 1.53 million barrels according to API.

Reportedly, $2.9 billion of 1.3770-80 USDCAD option strikes expire at 10:00 am today, which could make things entertaining.

USDCAD Technical Outlook:

The intraday technicals are bullish above 1.3760, which is the base of the week-long uptrend channel, and looking for a breach of resistance at 1.3800 to extend gains to 1.3860. A move below 1.3680 suggests further losses to 1.3690.

Longer term, the downtrend line that guided prices lower since March was broken yesterday with the move above 1.3760. Momentum has accelerated but there is strong resistance in the 1.3870 area.

For today, USDCAD support is 1.3760 and 1.3720. Resistance is 1.3810 and 1.3860. Today’s Range: 1.3760-1.3860.

FOMC Family Feud?

Global market action was rather hushed overnight ahead of today’s FOMC meeting. The Fed is widely expected to leave rates unchanged at 4.50% for the fifth consecutive time. A “no-change” result is sure to irritate Trump. Fed officials believe they will have a better impact on how Trump’s tariffs are impacting inflation and economic growth by the September 17 meeting, as they will see two more employment reports and get additional readings on inflation and housing.

The excitement from today’s meeting will occur if Fed Governor Waller and Fed Governor Bowman dissent and call for rate cuts. Both of them are auditioning for Powell’s job, and by pushing for lower rates, they hope to demonstrate loyalty to Trump.

Q2 GDP rose 3.0%, more than the forecast of 2.4% and core GDP rose 2.5% (forecast 2.4%). ADP reported that the US added 104,000 new jobs. The greenback ticked higher on the news and the US 10-year Treasury yield ticked up to 4.358% from 4.327%.

Taking Stock

Wall Street closed with small losses ahead of today’s Fed meeting, and Asian indexes were undecided. Australia’s ASX 200 rose 0.59%, while Japanese equity traders ignored tsunami warnings and lifted the Topix to a 0.40% gain. Hong Kong’s Hang Seng dropped 1.36%.

European equity traders twiddled their thumbs, although French traders may have twiddled faster as the CAC-40 index rose 0.50%, while the German DAX is unchanged and the UK FTSE 100 is down 0.25%. S&P 500 futures are also flat ahead of earnings reports from Meta and Microsoft today. The US dollar index (DXY) is steady at 98.86 as of 6:00 am EDT. Gold (XAUUSD) is 3331.93, and the US 10-year Treasury yield is 4.327% after dropping from 4.42% yesterday.

EURUSD

EURUSD traded in a 1.1540-1.1572 range as it consolidated yesterday’s losses due to EU officials signing a one-sided trade deal with the US. Weak German Q2 growth (actual -0.1% q/q) was offset by slightly better Eurozone Q2 GDP (actual 0.1% vs forecast 0.0%). Consumer Confidence was unchanged. In addition, US economic outperformance vs the Eurozone and the FOMC leaving US rates unchanged will weigh on the single currency.

GBPUSD

GBPUSD is near the top of its overnight 1.3342-1.3386 range, with prices underpinned by EURGBP selling. The UK also secured a better trade deal with Trump than what EU negotiators managed, and that is supporting prices. The short-term technical picture is negative while GBPUSD trades below 1.3550.

USDJPY

USDJPY is in the middle of its 147.81-148.53 band after an 8.8-magnitude earthquake in Russia’s Kamchatka Peninsula region triggered tsunami sirens in Japan. Lower 10-year Treasury yields also weighed on prices ahead of today’s Fed meeting and the Bank of Japan meeting tomorrow.

AUDUSD

AUDUSD sank from 0.6529 to 0.6494 and is at its low in NY. The currency has been under pressure since last Thursday when it peaked at 0.6624, and the selling pressure was exacerbated after weaker-than-expected Q2 inflation data (CPI 0.7% q/q, forecast 0.8%, previous 0.9%). Westpac Bank Chief Economist Luci Ellis said the results confirm an RBA rate cut to 3.60% from 3.85% on August 12.

USDMXN

USDMXN traded defensively in an 18.6990-18.7617 range after retreating from yesterday’s peak of 18.8300. Lower US Treasury yields helped to knock prices lower, but the downside is limited ahead of Trump’s August 1 tariff deal deadline when Mexico faces a 30% tariff on exports to the US. News that Mexico’s Q2 GDP rose 0.7% (forecast 0.4%, previous 0.2%) barely moved the needle.

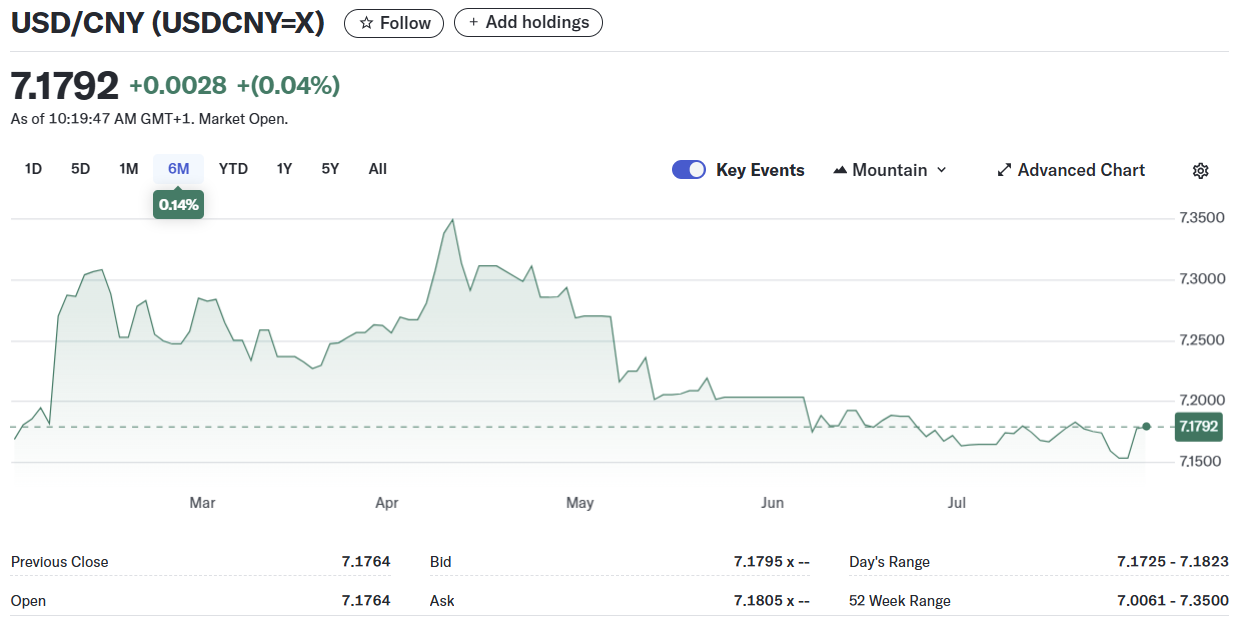

USDCNY

PBoC fix: 7.1441 vs exp. 7.1742 (Prev. 7.1511)

Shanghai Shenzhen 300 fell 0.02% to 4151.24

China trade negotiator Vice Minister of Commerce Li Chenggang said there was an agreement for a tariff pause extension. US Commerce Secretary Scott Bessent said nothing was agreed, as it is Trump that will make the decision.

The US continues to have major issues with China’s manufacturing overcapacity, purchases of Iranian oil, and selling dual-use technology to Russia.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau