August 15, 2025

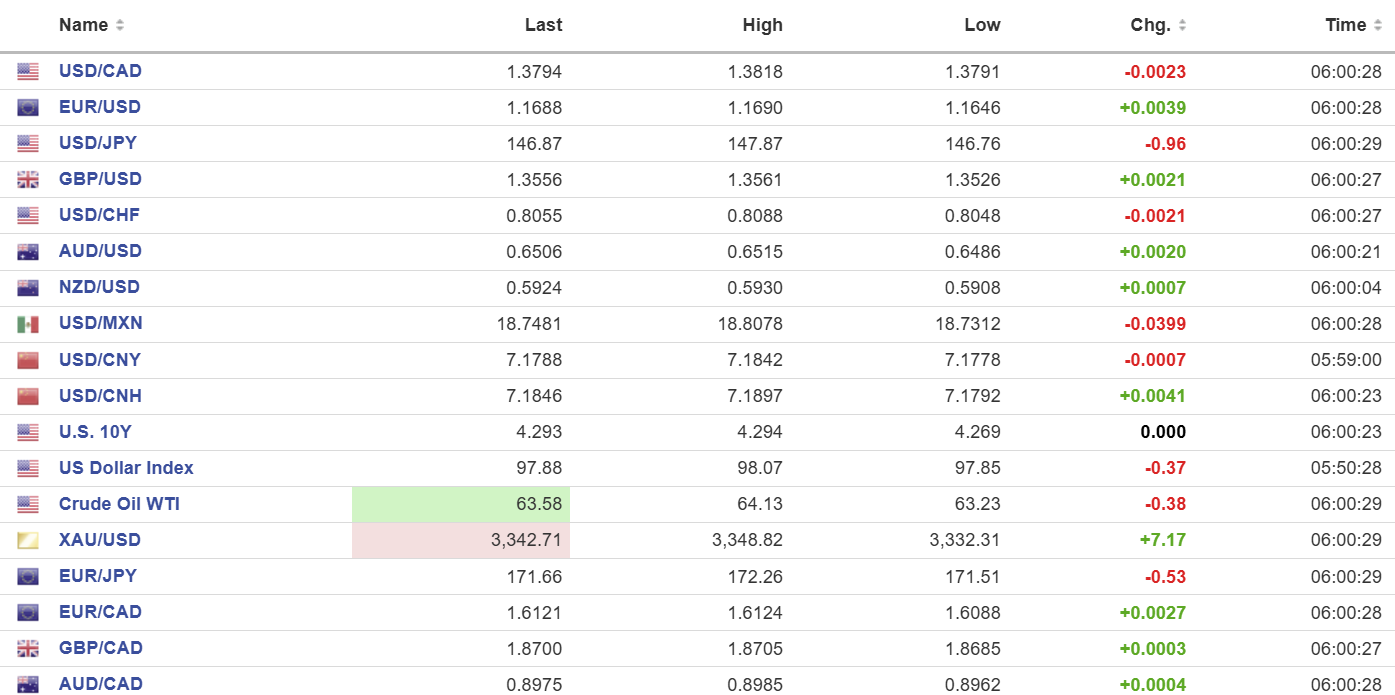

USDCAD open 1.3794, overnight range 1.3788-1.3818, close 1.3818

USDCAD is tracking broad US dollar moves vs the majors while traders ignore domestic influences, Yesterday’s US PPI report showed inflation rising with sparked sharply higher Treasury yields and reduced odds for aggressive Fed rate cuts for the rest of the year. Further evidence of rising US prices is on tap today with the Michigan Consumer Inflation expectations survey.

China’s Ministry of Commerce filed a complaint to the World Trade Organization (WHO) over Canada’s imposition of a 25% tariff on Chinese-made steel and aluminum and a 100% tariff on Chinese-made electric vehicles (EVs). China believes Canada is a US lackey and riding America’s tariff coattails. Of course, China still believes that locking up Canadian citizens because they are annoyed at the Federal government and its tariffs on Canadian agricultural products such as canola, peas, and pork are completely fine and justified.

WTI oil is near the bottom of its overnight 63.23-64.13 range with the selling pressure stemming from the soft Chinese retail sales and industrial production reports.

Canadian data includes Manufacturing sales and wholesale sales for June.

USDCAD Technical Outlook:

The intraday technicals are slightly bullish above 1.3770 and are looking for a decisive break above the 1.3830-50 zone to extend gains to 1.3950. A move below 1.3770 shifts the focus to 1.3710.

The medium-term technical picture remains bearish while prices are below the 1.3950 area (61.8% Fibonacci retracement of September 2024 to February 2025 range). A decisive move above 1.3950 would negate the view. A move below 1.3720 targets 1.3650.

For today, USDCAD support is 1.3740 and 1.3700. Resistance is 1.3850 and 1.3890. Today’s Range: 1.3740-1.3820

Data Trumps Trump

President Trump meets with Russian President Putin at Joint Base Elmendorf-Richardson in Anchorage, Alaska at 3:30 pm EDT. Trump wants Putin to agree to end the war in Ukraine or else face “severe consequences.” Putin merely wants to keep full control of Ukraine’s eastern regions, including Luhansk, Donetsk, Zaporizhia, and Kherson, parts of which Russia annexed in 2022, along with Crimea, which it annexed in 2014.

It is unlikely anything will be decided today, especially since Ukraine President Volodymyr Zelenskyy was invited to the sit-down.

Americans are still shopping despite tariffs. Retail Sales rose 0.5% as expected but the June number was revised higher as was the control group. Essentially, it means the Fed has no need to rush and cut rates.

Still to come, the University of Michigan Consumer Sentiment Index and its inflation expectations component, along with Industrial Production, Capacity Utilization, and Business Inventories.

Taking Stock

Asian equity markets finished the week on a positive note, except for Hong Kong’s Hang Seng index, which fell 0.98% due to weaker-than-expected Chinese data. Japan’s Topix recouped all of yesterday’s losses and rose 1.63%, while Australia’s ASX 200 rose 0.73%.

European bourses are mixed as of 5:35 am PDT, led by the French CAC-40 index rise of 0.55 %, while the German DAX and the UK FTSE 100 are flat. S&P 500 futures are up 0.010%. The 10-year Treasury yield hung on to yesterday’s gains and is 4.29%. Gold (XAUUSD) is 3337.98 and the US dollar index (DXY) is steady at 97.92

EURUSD

EURUSD drifted higher overnight, rising from 1.1646 to 1.1692 as the impact of yesterday’s higher-than-expected US PPI inflation data fades ahead of today’s US economic reports. Traders are also cautious ahead of the Trump/Putin meeting, and there were no Eurozone economic reports on tap today.

GBPUSD

GBPUSD is at the top of its 1.3526-1.3562 range in quiet trading ahead of today’s US data but remains within spitting distance of its one-month peak of 1.3590. Prices continue to be supported by better-than-expected UK GDP results. The intraday technicals are bullish, but a failure to decisively breach 1.3590 will see a retest of support in the 1.3490-1.3500 area.

USDJPY

USDJPY traded lower within a 146.76–147.87 range, giving back its post-PPI gains from yesterday. Stronger-than-expected Q2 GDP (actual 1.0% vs. forecast 0.4% and an upwardly revised 0.6% to the previous result) has increased the likelihood of a BoJ rate hike. Additionally, the spike in the US 10-year Treasury yield from 4.20% yesterday to 4.29% today is exerting further pressure on the pair.

AUDUSD

AUDUSD inched higher in a 0.6486-0.6515 range due to a slightly softer US dollar, with traders ignoring the latest soft economic data from China. AUDUSD continues to be supported following the somewhat robust employment data.

USDMXN

USDMXN rallied to 18.8570 from a low of 18.6255 yesterday after the hotter-than-expected US PPI data lowered (slightly) the odds for aggressive Fed rate cuts in 2025. That rally stalled overnight, and the currency is trading at 18.7378 in NY. A break below minor support at 18.7350 will extend losses to yesterday’s low.

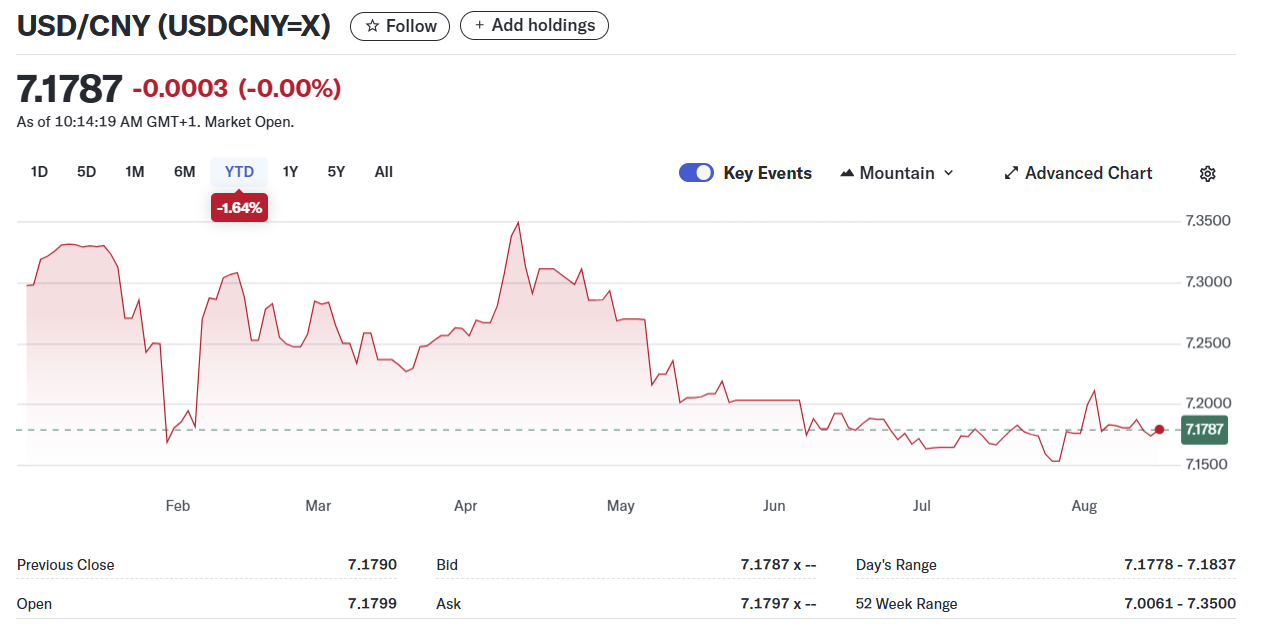

USDCNY

PBoC fix: 7.1371 vs exp. 7.1852 (Prev. 7.1337)

The Shanghai Shenzhen CSI 300 rose 0.70% to 4202.36.

July Industrial Production rose 5.7% y/y (forecast 5.9%, June 6.8% y/y) Retail Sales rose 3.7% y/y (forecast 4.6%, June 4.8%). House Price index -2.8% m/m, June -3.2%.

China’s MOFCOM filed a WTO lawsuit against Canada for import restrictions on steel and other products.

A Xi Jinping speech from February was just released to the public today. The South China Morning Post reports that the speech “included vows the country would guarantee a level playing field for private firms, safeguard entrepreneurs’ lawful rights and interests, and step up efforts to solve their long-standing challenges, including overdue payments.”

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics