September 3, 2025

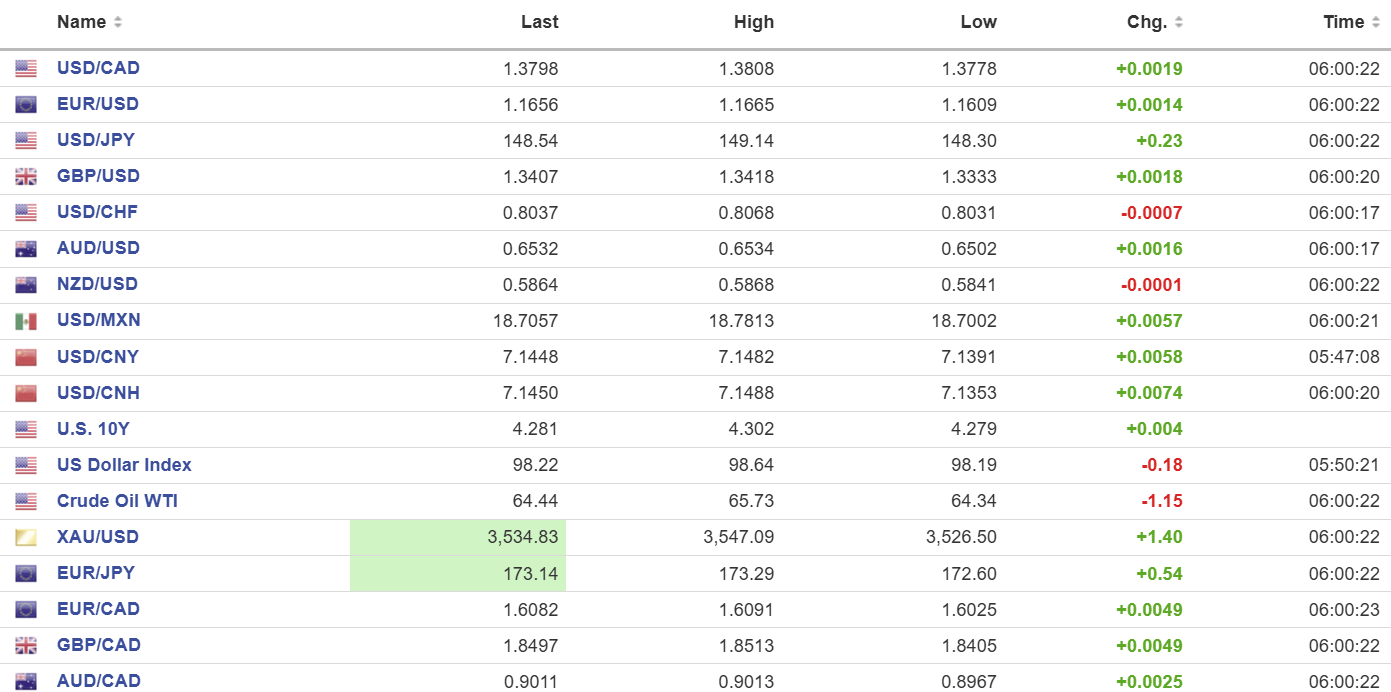

USDCAD open 1.3797, overnight range 1.3778-1.3808, close, 1.3784

USDCAD is trading with a bid even as other G-10 currencies show signs of recouping yesterday’s losses. USDCAD-specific drivers are hard to come by, but the ongoing deterioration of the Canada/US trade relationship is underpinning prices. Yesterday, the S&P Global PMI report showed Manufacturing PMI rose to 48.3 from 46.1. Economics Director Paul Smith wrote “Canada’s manufacturing economy continued to struggle in the face of tariffs and uncertainty in August.”

Tariff issues were front and center yesterday after Diageo PLC, the maker of Crown royal whiskey announced it was closing it Amherstburg plant and moving it to the US. The company claims the decision was made to improve its North American supply chain. The reality is it’s another win for Trump. Ontario Premier Doug Ford was unhappy with the decision and said that Diageo management were “a few French fries short of a Happy meal” and that they were “dumber than a bag of hammers.”

WTI retreated from 65.73 to 64.04 due to rumours that Opec may announce another production increase on September 8.

Today’s US data includes JOLTS job openings and Factory orders for July.

USDCAD Technical Outlook:

The intraday technicals are bullish while trading above 1.3750 and looking for a break above 1.3820 to extend gains to 1.3860. A move below 1.3750 suggests a retest of support at 1.3710.

The medium-term picture is bearish below 1.3900 and looking for a move below 1.3910 to extend losses to 1.3550.

For today, USDCAD support is 1.3760 and 1.3713. Resistance is 1.3820 and 1.3860. Today’s Range: 1.3760-1.3850.

“Headless Chicken” Market

Traders are bouncing off the walls like the silver ball in an old school pinball machine. It’s all noise ahead of Friday’s nonfarm payrolls report which will shift the focus from rising bond yields, Trump’s tariff woes, and Lisa Cook’s “firing.” Friday’s NFP numbers will determine if Powell’s pivot was the right move, especially if the revisions are far less than expected and if the economy adds more jobs than expected or if average hourly earnings are rising. On the other hand, the data could be so weak that markets start pricing in a 50 bp rate cut.

Taking Stock

Asian equity indexes followed Wall Street’s lead and closed with losses. Australia’s ASX 200 fell 1.82% due to economic data reducing the likelihood of an RBA rate cut. Japan’s TOPIX lost 1.07% and Hong Kong’s Hang Seng fell 0.60%.

As of 5:30 am PDT, retreating bond yields has helped the German DAX to a 0.73% gain, the French CAC 40 is up 0.88% and the UK FTSE 100 has climbed 0.44%. S&P 500 futures are up by 0.42% and the US Dollar Index (DXY) is 98.27. Gold is firm at 3546.38 and the US 10-year Treasury yield is 4.275%.

EURUSD

EURUSD consolidated yesterday’s losses in a 1.1609-1.1665 range overnight. Eurozone PMI data (Services and Composite) were slightly weaker than expected but both remained above 50, which is considered expansion territory. Producer prices rose 0.4% m/m in July, which was lower than the 0.8% in June. Traders are cautious due to French political issues and a proposed EU/Mercosur (Argentina, Bolivia, Brazil, Paraguay and Uruguay) trade deal which France does not want.

GBPUSD

GBPUSD rebounded from yesterday’s low and rallied from 1.3333 to 1.3418 where it sits in early NY. The 30-year Gilt retreated after hitting a new post-1998 high which helped the currency. Concerns about Chancellor Reeves’ spending plans eased as she is not tabling the Autumn budget until November 4. Prices got a bit of support from better-than-expected UK Services PMI which came in at 54.2 (forecast and July 53.6). S&P Global wrote “Business activity expectations meanwhile hit a ten month high in August, providing a clear signal that growth prospects for the UK service economy have moved up from the lows seen this spring.”

USDJPY

USDJPY traded choppily but with a bid in a 133.33-134.18 range powered by rising US Treasury yields and political uncertainty in Japan. Traders are also cautious ahead of upcoming trade talks in the US at the end of the week.

AUDUSD

AUDUSD is attempting to recoup all Monday’s losses and has risen from 0.6502 to 0.6534 underpinned by robust data that lowers the risk for an RBA rate cut at its September 30 meeting. Services PMI rose to 55.8 (forecast and previous 55.1) while Q2 GDP surprised to the upside, rising 1.8% (forecast 1.6%, previous 1.4%).

USDMXN

USDMXN traded defensively in a 18.7002-18.7813 range overnight. It has been a choppy two days due to confusion around Trump’s tariffs being ruled illegal to caution ahead of this week’s US employment reports (ADP, JOLTS, jobless claims and NFP). Consumer confidence data is on tap.

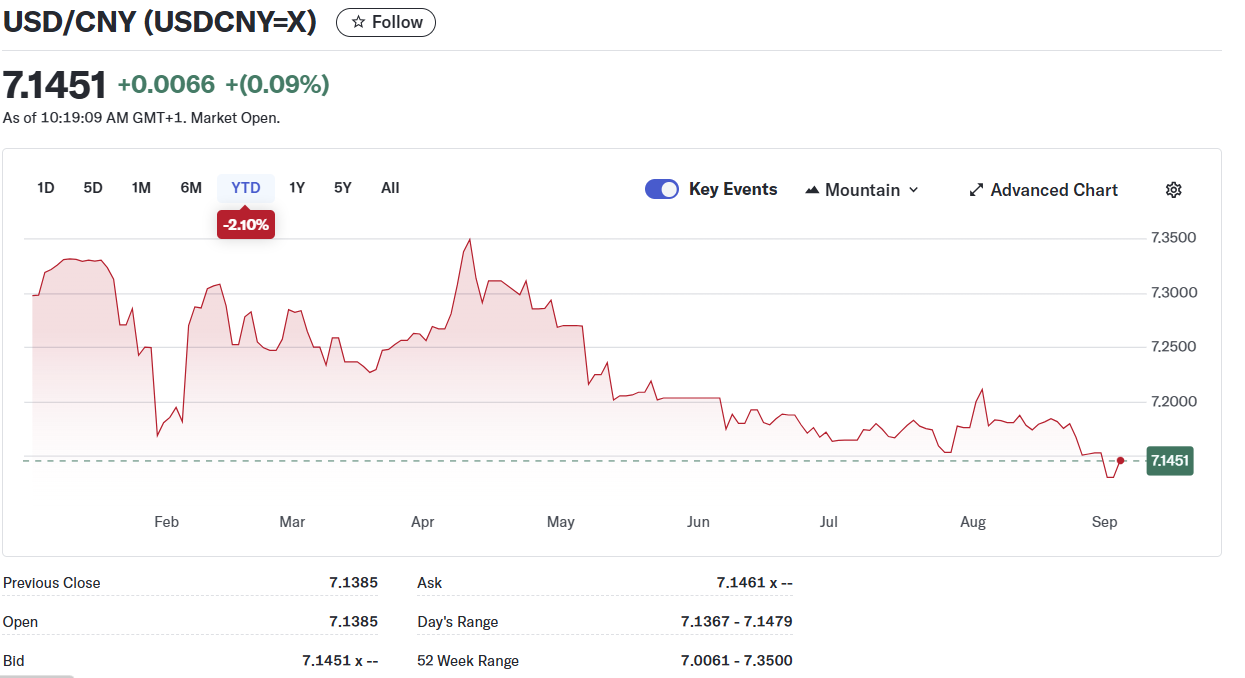

USDCNY

PBoC fix: 7.1108 vs exp. 7.1476 (Prev. 7.1089).

Shanghai Shenzhen CSI 300 fell 0.68% to 4459.83.

RatingDog (formerly Caixin-but in partnership) Services PMI rose to 53 compared to 52.6 in July. It was the fastest increase since May 2024.

Xi Jinping plant his flag on the side of the “good guys” against the backdrop of a military parade showcasing China’s military might. He said “today, mankind is faced with the choice of peace or war, dialogue or confrontation, win-win or zero-sum.”

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics