September 4, 2025

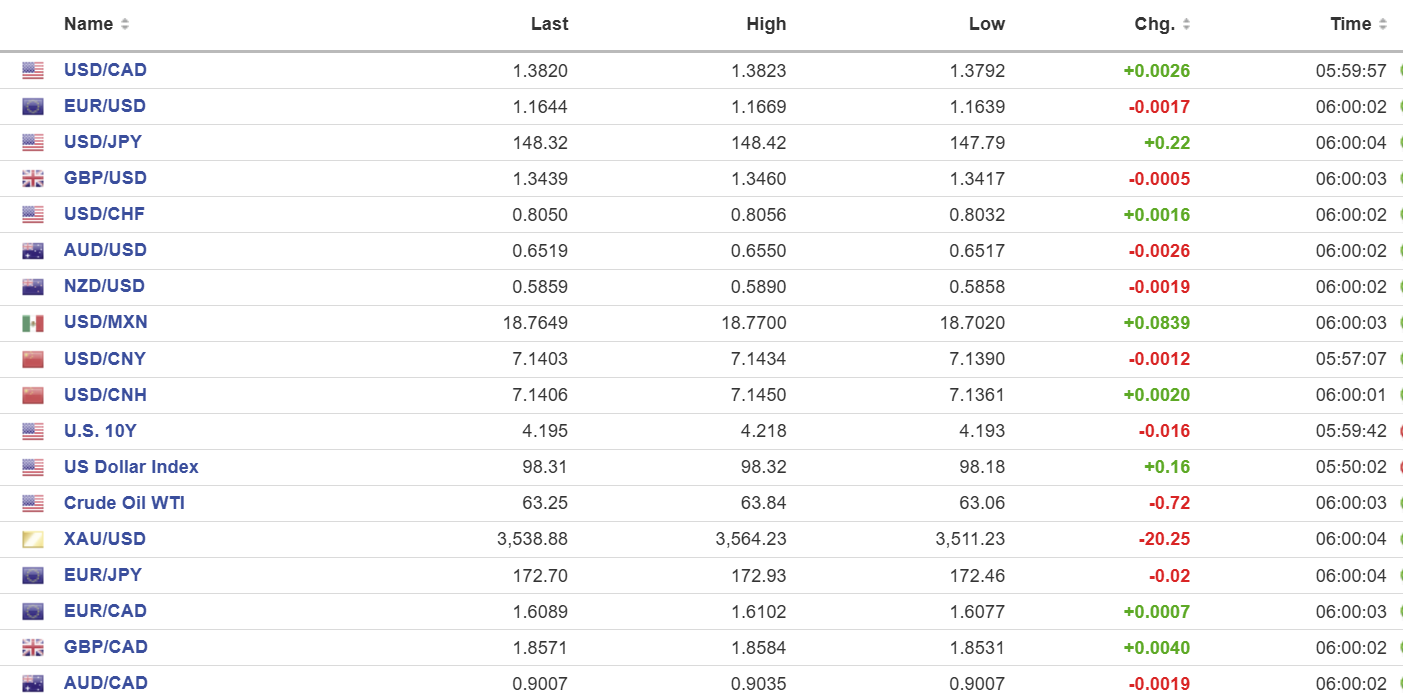

USDCAD open 1.3820, overnight range 1.3792-1.3828, close, 1.3793

USDCAD drifted higher overnight in concert with broad US dollar gains against the majors. Traders are adjusting positions ahead of the employment reports that are being released today and tomorrow. The data has taken on a heightened sense of importance because Powell suggested a weakening job market would lead to rate cuts.

Yesterday, Fed Governor Christopher Waller said he wanted lower interest rates this month and multiple cuts in the coming months. Atalanta Fed President Raphael Bostic said he favoured a rate cut but didn’t say when. Minneapolis Fed President Neal Kashkari claimed that the neutral rate was around 3.0% and =said rates have some room to go lower.

Despite the dovish comments, the greenback caught a bid.

WTI is at the lower end of its 62.91-63.84 range on fears that Opec may announce another production increase on September 8. Russia President Putin is feeling better after China and Russia signed a deal to increase oil sales to China.

Canada’s trade deficit narrowed to $4.94 billion from 5.988 billion

USDCAD Technical Outlook:

The intraday technicals are bullish while trading above 1.3760 and looking for a break above 1.3830 to extend gains to 1.3870. A move below 1.3760 suggests a retest of support at 1.3710.

The medium-term picture is bullish with a sustained moved above the 61.8% Fibonacci retracement of the November 24-Feb 2025 range at 1.3951 and the 100 day moving average at 1.3766 suggesting further gains to the 200-day moving average at 1.4024. The MACD and RSI are mildly bullish.

For today, USDCAD support is 1.3760 and 1.3720. Resistance is 1.3830 and 1.3860. Today’s Range: 1.3760-1.3860

Employment Reports take Center Stage

There is no shortage of American labour reports to fan the flames of fear for Friday’s nonfarm payrolls data.

Challenger job cuts surged 39% to 85,979 in August compared to 62,075 in July and was the highest numbers since 2020.

The ADP Employment change report showed a gain of 54,000 which was below the forecast of 65,000 and well-below July’s 104,000. ADP’s reputation as an unreliable precursor to NFP has been challenged this year, as recent divergences were erased after NFP revisions, suggesting ADP was closer to the underlying employment trend from the outset.

Weekly jobless claims rose by 7,000 to 237,000 and the 4-week average ticked up to 231,000 from 228,500. rise in claims, to 230,000.

The US trade deficit widened to $78.3 billion from $60.2 billion which will likely have a negative impact on GDP as well.

The above data not only guarantees a rate cut on September 17 (which is already fully price in) but raises the odds for a 50 bp move.

Taking Stock

Wall Street closed with the S&P 500 and NASDAQ higher thanks to Google winning its court case, and Asian equity indexes joined the party. Australia’s ASX 200 rose 1.00% and Japan’s TOPIX rose 1.03%. Hong Kong’s Hang Seng fell 1.12% on fears of fresh government regulation to help cool the market.

As of 8:40 am EDT, the German DAX has risen 0.65% while the French CAC 40 has dropped 0.16%. The UK FTSE 100 is down 0.18% while the S&P 500 futures are up by 0.15%. The US Dollar Index (DXY) is 98.29. Gold is 3544.42and the US 10-year Treasury yield is 4.186%.

EURUSD

EURUSD traded in a 1.1639-1.1669 range due to a mix of soft data and profit-taking ahead of tomorrow’s US NFP data. Eurozone retail sales rose 2.2% rather than the 2.4% that was expected, which sparked concern that consumer demand could help offset the negative impact to economic growth from Trump’s tariffs.

GBPUSD

GBPUSD traded choppily in a 1.3417-1.3460 range as global bond tensions eased and BoE Governor Bailey spoke of a more cautious stance to additional rate cuts. Analysts do not expect the BoE to cut rates on November 6 because the Autumn budget is planned for November 26.

USDJPY

USDJPY is bid and traded in a 147.79-148.42 range. This week, analysts have determined that the BoJ is rather reluctant to raise interest rates any time soon and that, coupled with a profit-taking bid for US dollars ahead of tomorrow’s NFP report, is supporting prices. US and Japan trade talks start today in Washington.

AUDUSD

AUDUSD is reversing yesterday’s rally and traded negatively in a 0.6517-0.6550 range due to broad US dollar demand. The currency pair did not get much benefit following news Australia’s trade surplus widened to AUD 7.31 billion from 5.36 billion in July.

USDMXN

USDMXN fully erased yesterday’s gains and rose from 18.7020 to 18.7700 due to renewed demand for US dollars ahead of today and Friday’s US employment reports.

USDCNY

PBoC fix: 7.1052 vs exp. 7.1405 (Prev. 7.1108)

Shanghai Shenzhen CSI 300 fell 2.12% to 4365.21

Chinese equity indexes got spanked on a Bloomberg report that authorities are discussing a number of measures to cool the stock market. Some measures include removing short-selling restrictions and curbing speculation.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics