September 8, 2025

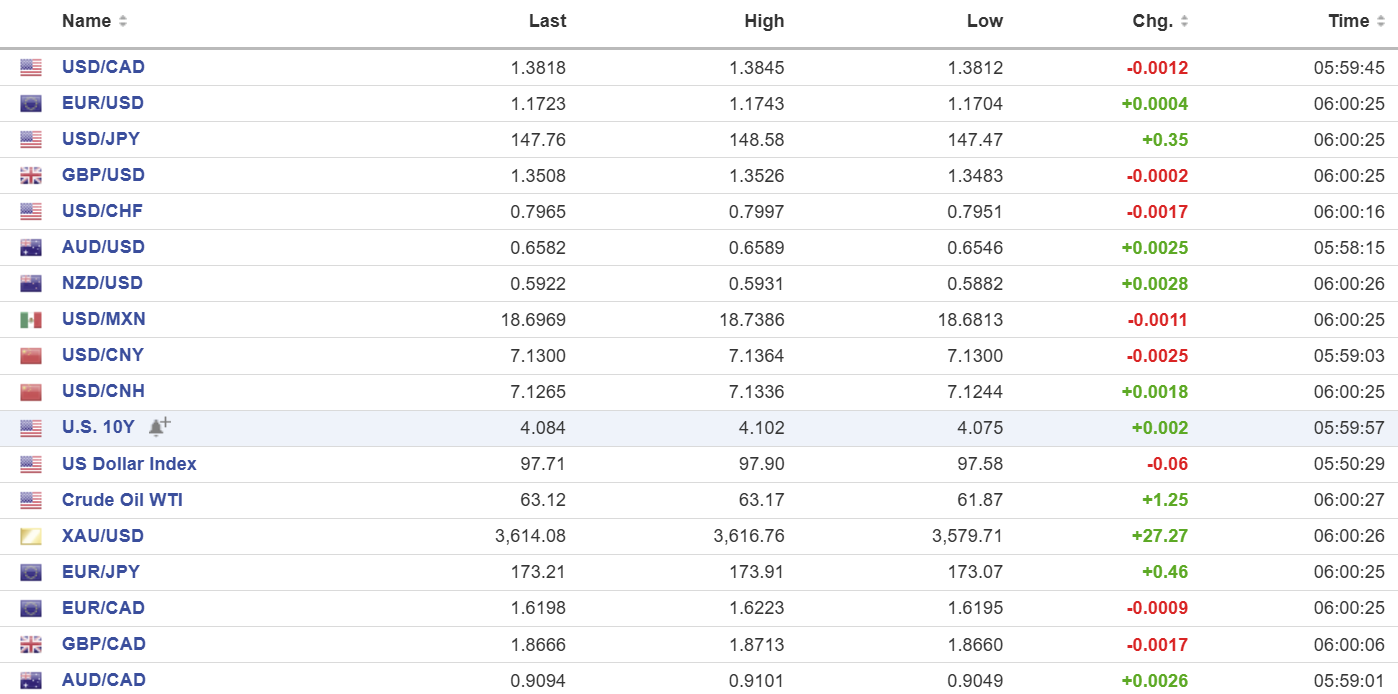

USDCAD open 1.3818,, overnight range 1.3799-1.3845, close, 1.3829

USDCAD is trading defensively as it consolidates Friday’s gains. Canada’s employment picture is rather ugly. The country lost 65,500 jobs on top of the 40,500 jobs that disappeared last month. Canada has lost 39,000 jobs since January. The results pretty much guarantee a 25 bp rate cut on September 17.

WTI oil prices rose from 61.87 to 63.23 and are at the top of that band in NY, despite Opec announcing a 137.000 barrel/day production increase effective October 1. The gain is supported by concerns that the US will impose new sanctions on Russian and Iranian oil.

Gold prices hit a record high of 3,621.92 overnight supported by news that China continues to buy gold and on speculation of sharply falling US interest rates.

USDCAD Technical Outlook:

The intraday technicals are bullish in a minor uptrend channel bound by 1.3780 on the bottom and 1.3870 on the top. A break below the base targets 1.3760 then 1.3730. A topside move will extend gains to 1.3920.

The medium-term picture is unchanged—USDCAD is bearish while prices remain below 1.4000 and 1.3951 which is major 61.8% Fibonacci resistance. The momentum indicators are neutral.

For today, USDCAD support is 1.3780 and 1.3750. Resistance is 1.3840 and 1.3890. Today’s Range: 1.3780-1.3840

Managing Expectations

Treasury Secretary Scott Bessent wrote an opinion column in the WSJ on the weekend. He argues that the Federal Reserve’s post-2008 reliance on unconventional tools—quantitative easing, balance-sheet expansion, and expanded regulatory authority—has turned into a risky gain-of-function experiment. Bessent’s argument is just another front in Trump’s multi-pronged attack on Fed Chair Powell in an effort to secure his resignation and lower interest rates.

Trump’s finalists for Fed Chair are Fed Governor Christopher Waller, Director of the National Economic Council Kevin Hassett, and former Fed Governor Kevin Warsh.

Misguided Expectations

Economists from the Dallas Federal Reserve penned an essay a few days ago that crushes Trump’s arguments of how tariffs will reduce the deficit. The short answer is “they don’t.” Tariffs raise costs on imported goods including parts for components manufactured in the USA. Manufacturers end up paying more for steel, chips, or machinery, which makes their own exports less competitive. The Dallas Fed notes that these effects “largely neutralize one another. The result—higher costs for businesses and consumers, supply-chain uncertainty, and retaliation from trading partners.

Taking Stock

Asian equity indexes closed higher, except for the Australian ASX 200 which fell 0.24% due to poor China trade data. Japan’s Topix rose 1.06% and Hong Kong’s Hang Seng gained 0.86%.

As of 5:30 am PDT, the French CAC 40 is leading the other major European indices higher and has risen 0.40%, the German Dax is up 0.30%, and the UK FTSE 100 has gained 0.12%. S&P 500 futures are posting a gain of 0.14% while the US Dollar Index (DXY) is softer at 97.66. Gold is $3,618.99, and the US 10-year Treasury yield is 4.068%.

EURUSD

EURUSD is consolidating Friday’s post-NFP gains in a 1.1704-1.1743 range as the rally hit a wall of caution stemming from French political uncertainty (the government is expected to lose a non-confidence vote today) and falling investor confidence (actual -9.2 vs -3.7 in August). German industrial production rose 1.3%, as expected. Thursday, the ECB is expected to leave rates unchanged. The upcoming US inflation data, French politics, and the ECB meeting suggest that EURUSD will trade in a 1.1660-1.1760 range until Thursday.

GBPUSD

GBPUSD is trading with a bullish bias in a 1.3483-1.3526 range with commuting traders grumpier than usual due to an ongoing tube strike and computer issues with the Transport for London website. There is a dearth of economic data from the UK, leaving GBPUSD direction to the whim of US dollar sentiment.

USDJPY

USDJPY trading was volatile in a 147.47-148.58 range. Prices gapped higher at the Asia open, soaring from 147.40 at Friday’s close to the session peak and then dropping to 147.48 by mid-morning in Europe to fill the gap. Prime Minister Shigeru Ishiba’s sudden resignation sparked the turmoil. He will remain on the job until his replacement is elected. The political news overshadowed Q2 GDP which rose 0.5% q/q compared to the forecast and previous result of 0.3%.

AUDUSD

AUDUSD is hanging on to Friday’s gains and traded in a 0.6546-0.6589 range. Traders ignored the soft Chinese trade data and focused on the risk of further US dollar downside on lingering fall-out from the ugly US jobs data on Friday. The two-week AUDUSD uptrend channel is intact while prices are in a 0.6520-0.6610 range.

USDMXN

USDMXN traded lower in a 18.6781-18.7386 range on broad-based US dollar selling pressure. Tuesday’s domestic inflation data will not be a factor.

USDCNY

PBoC fix: 7.1029 vs exp. 7.1317 (Prev. 7.1064)

Shanghai Shenzhen CSI 300 rose 0.16% to 4467.57

China trade surplus widens to $102.33 billion from $94.24 billion in July. Exports rose 4.4% (forecast 5.0%) while imports rose 1.3% (forecast 3.0%).

China’s gold holdings rose for the 10th month in a row to 74.02 million ounces.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics