April 4, 2024

- Powell soothes market angst; risk sentiment improves.

- Importance of tomorrow’s NFP data diminished.

- US dollar opens on the defensive, adds to yesterday’s losses.

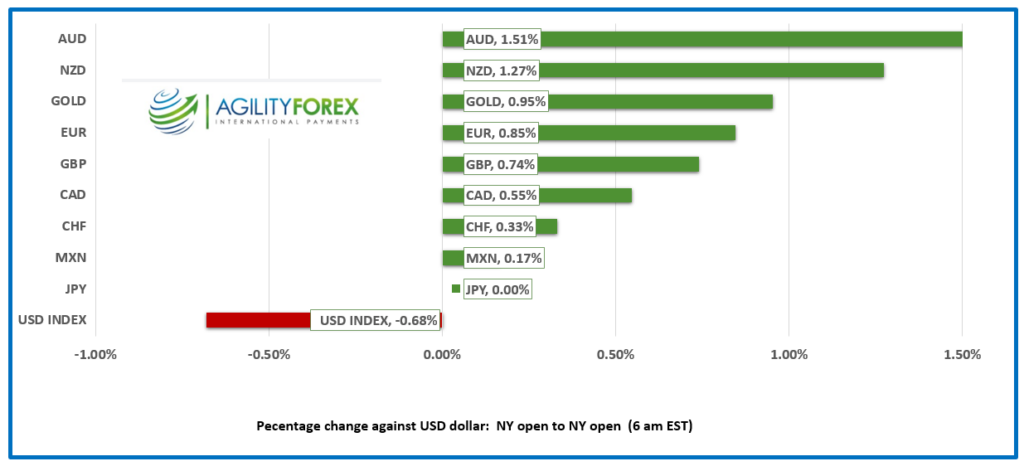

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3499-03, overnight range 1.3499-1.3533, close 1.3527

USDCAD dropped yesterday on the heels of the tame US ISM services data and after Fed Chair Jerome Powell reassured markets that despite recent data surprises, it “did not materially change the overall view.”

USDCAD is likely to consolidate its recent gains ahead of Friday’s US and Canadian employment reports. Canada is expected to have gained 25,700 jobs while US nonfarm payrolls are expected to rise by 200,000.

WTI oil traded quietly in a $85.05-$85.79 range with gains limited due to yesterday’s EIA report showing US crude inventories rose 3.21 million barrels instead of falling by 1.5 million barrels as was expected.

Canada’s trade surplus widened to $1.39 billion in February, compared to $0.61 billion in January.

USD/CAD Technicals

The intraday USDCAD technicals turned bearish with the break below 1.3540. The downtrend is intact below 1.3520 and looking for a break of support in the 1.3480-1.3490 area to extend losses to 1.3440. A move above 1.3520 suggests further 1.3500-1.3600 consolidation.

The longer term , the USDCAD uptrend line from the beginning of the year is intact above 1.3480 which also where 100 day(1.3482) and 200 day (1.3500) moving average support is clustered. A decisive move below support suggests a retest of 1.3180.

For today, USDCAD support is at 1.3490 and 1.3460. Resistance is at 1.3540 and 1.3590. Today’s range is 1.3480-1.3540.

Chart: USDCAD daily

Source: DailyFX

“I Repeat…”

Fed Chair Jerome Powell downplayed recent economic data surprises yesterday. In a speech at the Stanford School of Business he said, “The recent data do not, however, materially change the overall picture, which continues to be one of solid growth, a strong but rebalancing labor market, and inflation moving down toward 2 percent on a sometimes bumpy path.”

The market heard that the Fed remains on track to cut interest rates by 75 bps in 2024 and bought stocks and bonds and sold US dollars.

Mr. Powell’s comments also suggest that traders are less likely to react if Friday’s NFP number is higher than expected (forecast 214,000).

Are New US Tariffs on the Agenda?

US Treasury Secretary Yellen is in China to talk about what she believes are China’s unfair trade practices. China’s penchant for massive subsidies has enabled Chinese companies to undercut prices for similar goods in other countries. New US tariffs on Chinese goods are a possibility.

Equity Market Recap

Asian equity indexes closed with gains, at least the ones that were open. Japan’s Nikkei 225 index gained 0.81% while Australia’s ASX 200 rose 0.45%. Chinese, Hong Kong, and Taiwan indexes were closed for a holiday. European equity traders liked what Powell was saying and the major bourses are trading in positive territory, albeit just slightly. S&P 500 futures are up 0.30% while the US 10-year Treasury yield inched down from 4.42% yesterday to 4.361% this morning. Gold popped above $2300 but has since retreated to $2294.30. The US dollar index (DXY) slid to 103.87 from 104.03.

No Excitement from US jobs or trade data

Weekly jobless claims rose by 9.000 from the upwardly revised 212,000 level last week. US job cuts jumped to 90,309 in March and is a 7% increase from February. The US dollar barely budged on the news.

EURUSD

EURUSD was a big beneficiary of yesterday’s benign US ISM Services data and Powell’s comments, rising from Wednesday’s low of 1.0764 to 1.0866 in early NY trading. The rally was fueled by Eurozone and German Composite and Services PMI data. The S&P Chief Economist wrote, “The service sector in the eurozone is gradually finding its footing, with activity stabilizing in February and showing signs of moderate growth in March. This favorable trend is expected to persist, fueled by wage growth outpacing inflation, thus bolstering the purchasing power of households.”

GBPUSD

GBPUSD climbed to 1.2671 from 1.2644 due to broad US dollar weakness after Powell reignited hopes for three Fed rate cuts in 2024. UK Services PMI ticked down to 53.1 in March, from 53.4 in February. S&P’s Economics Director wrote, “The recovery in service sector output lost a little bit of momentum during March, and more so than suggested by the flash PMI results, but the overall picture remains reasonably positive.”

USDJPY

USDJPY stagnated in a 151.54-151.79 range due to steady US Treasury yields. Fears of BoJ intervention are capping gains.

AUDUSD and NZDUSD

AUDUSD rebounded smartly, rising from yesterday’s low of 0.6503 to 0.6608 in early NY trading. The shift to positive risk sentiment and a 5.2% rise in Building Permits in February (January 4.8%) supported the gains.

NZDUSD climbed from an Asian low of 0.6004 to 0.6043 in early new on the back of broad US dollar weakness. The rally above 0.6010 snapped the month-long downtrend and suggests further gains to 0.6110.

USDMXN

USDMXN consolidated yesterday’s losses in a 16.5343-16.5615 range. Mexican Consumer Confidence ticked up to 47.4 from 47.1 in February which was largely ignored. The dovish outlook for US rates is limiting USDMXN gains.

Bitcoin (BTCUSD)

Bitcoin (BTCUSD) traded sideways in a 65,048-66,931 range with the crypto currency unable to get any traction following yesterday’s benign ISM services data or Fed Chair Powell’s “steady as she goes” comments.

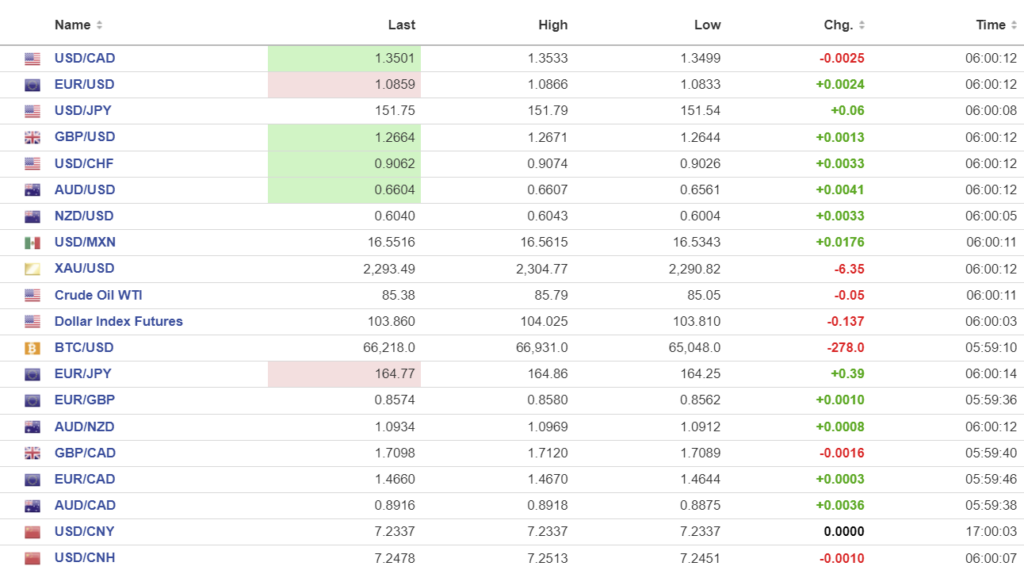

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0949 vs exp. 7.2282 (prev. 7.0957).

Shanghai Shenzhen CLOSED

China is closed today and Friday for National holidays.

Chart: USDCNY and USDCNH 4 hour

Source: Investing.com