July 4, 2024

- Eurozone inflation ticks lower.

- Greenback rises after Supreme Court rules on Trump immunity.

- US dollar opens on a mixed note

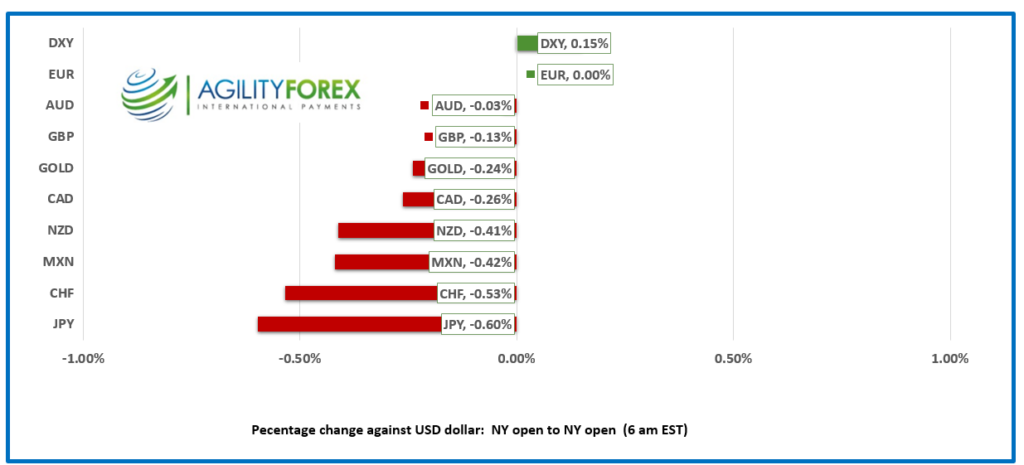

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3731, Monday-Tuesday range 1.3663-1.3756, Friday close 1.3680-Monday close 1.3738.

USDCAD took a walk on the wild side since Friday with prices dropping from 1.3733 to 1.3656 after Statistics Canada reported that April GDP rose 0.3% compared to 0% in March. The losses were fully reversed Monday after the French election results spooked markets and USDCAD rallied to 1.3756 overnight.

The improvement in domestic growth offset the sting from the higher inflation reading, making the odds for a July 24 rate cut a coin toss. US markets are closed Thursday and Friday. Canadian and US employment reports are due which suggests market catalysts will come from the UK election July 4 and rumors ahead of round 2 of the French elections which are July 7.

WTI oil prices have climbed from 80.99 on Friday to 84.13 overnight. Escalating tensions between Israel and Hezbollah, the early start to the US hurricane season, and increased gasoline demand around the July 4 holidays are underpinning prices.

There are no Canadian economic reports of note. US JOLTS job openings survey and Fed Chair Jerome Powell’s remarks from Portugal are the day’s highlights.

USDCAD Technicals

The intraday technicals flipped to bullish while still inside the 1.3650-1.3760 range that has contained price action for two weeks. Monday’s move above 1.3690 snapped an intraday downtrend are targeting a decisive break above 1.3760. Failure to do so ensures more 1.3640-1.3760 consolidation.

The 2024 uptrend line remains intact above 1.3710 and 1.3660. Resistance is at 1.3760-1.3690..

For today USDCAD support is at 1.3650 and 1.3620. Resistance is at 1.3720 and 1.3750. Today’s range is 1.3680-1.3750.

Chart: USDCAD daily

Source: DailyFX

A President Can Do No Wrong

The US Supreme Court ruled that former presidents have absolute immunity from prosecution for official acts that fall within their “exclusive sphere of constitutional authority” and are presumptively entitled to immunity for all official acts. Three of the judges supporting the ruling were nominated by Trump. Fortunately, it is unlikely that anyone, other than a convicted felon and egomaniac, would ever use the powers to seek vengeance on opponents and perceived enemies.

School’s Out for French Left

French President Emmanuel Macron and his woke policies have been rejected by French voters. Marine Le Pen’s National Party trounced Macron’s Renaissance party in round 1 of the French elections. All parties are scrambling to create alliances and the outcome is far from certain, limiting EURUSD upside.

Stocks on the Run

The Supreme Court ruling in favor of Trump combined with “Cadaver Joe’s” debate performance has equity traders fearing President Trump-the Sequel. Australia’s ASX 200 closed down 0.42% while the Tokyo Topix index surged 1.15%, fueled by the yen slide. The German DAX (down 0.90%) leads European bourses lower, while S&P 500 futures are down 0.37%.

EURUSD

EURUSD peaked at 1.0771 on Monday then fell to 1.0709 just before NY opened. Eurozone inflation fell to 2.5% from 2.6%. French election news will drive EURUSD direction until Friday’s US employment report.

GBPUSD

GBPUSD dropped from 1.2707 to 1.2633 yesterday due to broad US dollar strength on safe haven demand following round 1 of the French elections and the Supreme Court ruling on Trump. Prices traded slightly firmer in a 1.2615-1.2654 range overnight, partly because compared to the French political outlook, the UK is an oasis of tranquility.

USDJPY

USDJPY continues to trade higher. Prices rose from 160.63 on Monday to 161.77 just before NY opened due to the jump in the 10-year Treasury yield from 4.261% on Friday to 4.454% today. The higher US rates combined with suggestions that the BoJ will not intervene until prices get closer to 165.00 are supporting prices.

AUDUSD and NZDUSD

AUDUSD climbed from 0.6620 to 0.6685 on Friday following soft US data but gave back 50% of the move yesterday. Prices consolidated in a 0.6634-0.6661 range overnight. The minutes of the June 18 RBA meeting revealed policymakers were concerned about upside risks to inflation and discussed raising.

NZDUSD is at the bottom of its Monday-Tuesday range of 0.6048-0.6109 due to a mix of AUDNZD demand and a strong US dollar.

USDMXN

USDMXN rallied from 18.2008 on Friday to 18.4965 in NY today. The gains are supported by higher risks for Banxico to cut interest rates and because some economists downgraded their GDP forecasts to 2.1% from 2.2% in 2024. The USDMXN technicals are bullish above 18.3400 on a 4-hour chart.

Bitcoin (BTCUSD)

BTCUSD climbed from Friday’s low of 60,188 to 63,900 but failed to break above the top after two tries. The BTCUSD intraday technicals are bullish above 61,930

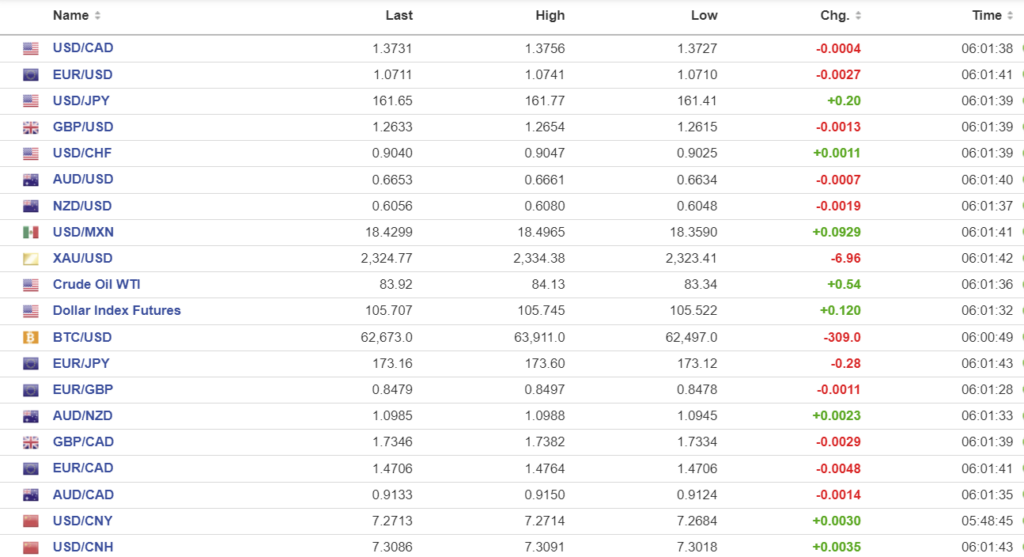

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1265 vs exp. 7.2558 (prev. 7.1268).

Sanghai Shenzhen CSI 300 fell 0.18% to 3471.79

NBS June Manufacturing PMI 49.5 (as forecast and unchanged from May). No-Manufacturing PMI 50.5 (forecast 51, May 51.1).

Caixin Manufacturing PMI 51.8 (forecast 51.2, May 51.7)

Chart: USDCNY and USDCNH

Source: Investing.com