March 28, 2025

- US Core PCE Index rises to 2.8% from 2.7% y/y

- Canada GDP rises 0.4% in January (forecast 0.3%).

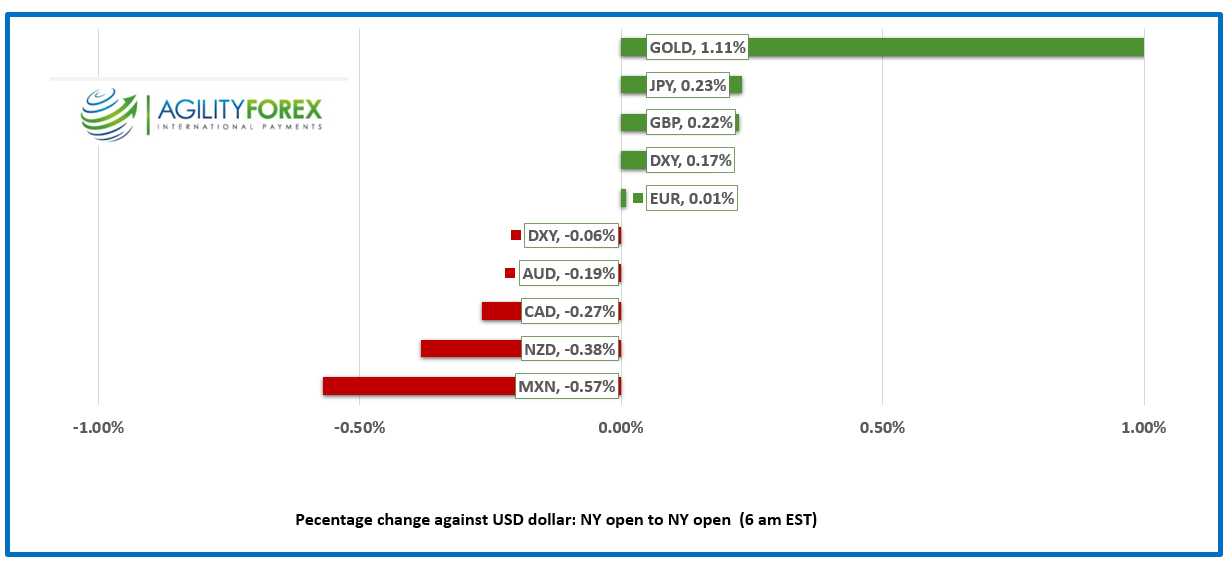

- US dollar opens mixed-commodity currency bloc underperform.

FX at a Glance

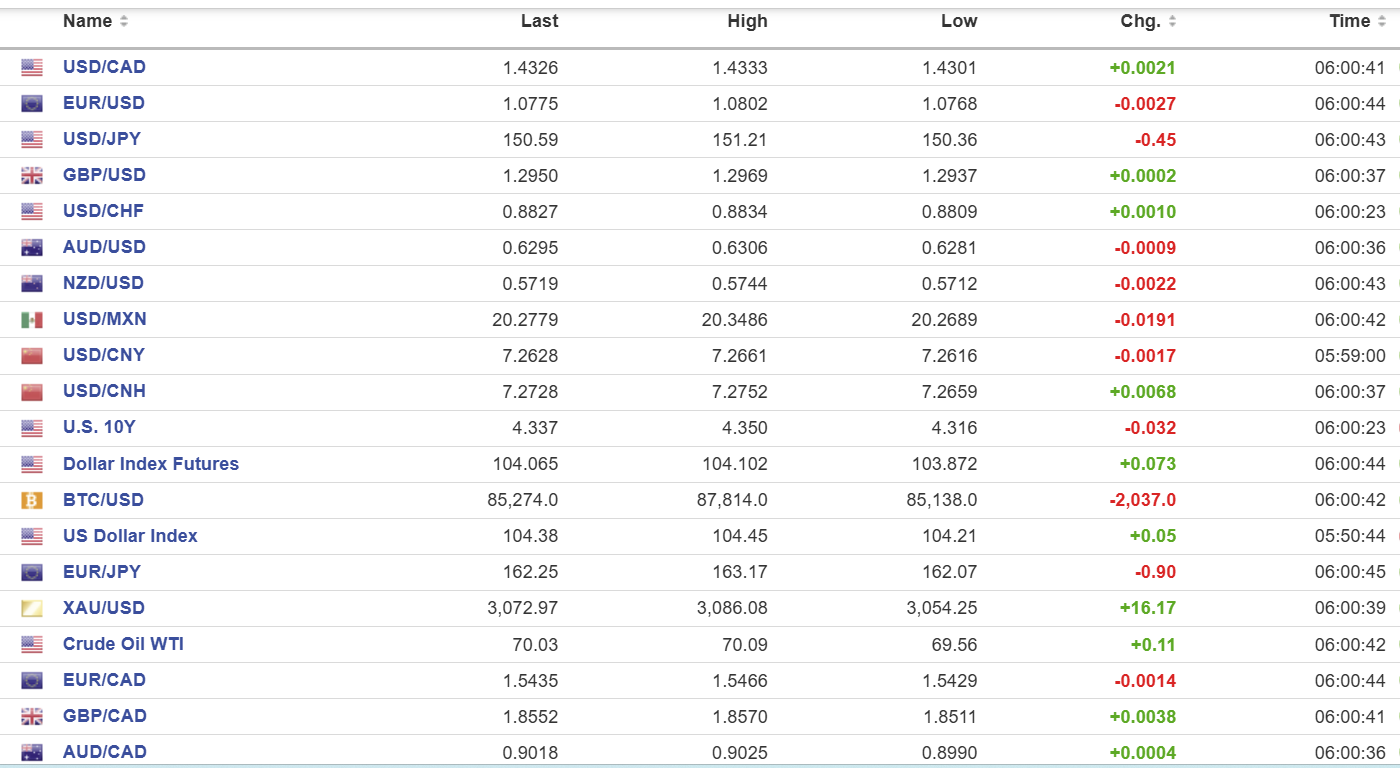

USDCAD: open 1.4326, overnight range 1.4301-1.4333, close 1.4306

“We’re mad as hell and we aren’t going to take it anymore.” That was the message Canadian politicians were sending to Trump and his cronies. Four days ago, Mark Carney said, “I’m available for a call, but we’re going to talk on our terms. As a sovereign country — not as what he pretends we are — and on a comprehensive deal.” R E S P E C T-find out what it means to me.

Trump’s tariff broadside on Thursday must have been the show of respect Carney was waiting for. Carney claims, “Last night, the president of the United States reached out to schedule a call.” Sceptics wonder if Mr. Carney is telling the truth after he made a number of inaccurate statements since becoming Liberal leaders.

The USDCAD story is the tariff story, and Ontario Premier Doug Ford said they will not react until after they see what happens on Tariff Tuesday.

Statistics Canada reports that “Canada January GDP grew 0.4% in January, following a 0.3% increase in December. Both goods-producing and services-producing industries were up, with 13 of 20 sectors rising in January “and predicted February ‘s result would be unchanged.

USDCAD Technicals

The intraday USDCAD technicals are bullish above 1.4300 and looking to break 1.4360 t to target 1.4400, then 1.4450. A move below 1.4300 targets 1.4260, then 1.4210.

The medium-term outlook is bullish with the move above 1.4300 snapping the March downtrend and shifting the focus to a retest of the 1.4550 area. The momentum indicators are starting to turn higher.

For today, USDCAD support is 1.4300 and 1.4260. Resistance is at 1.4360 and 1.4410.

Today’s Range: 1.4300-1.4400

Chart: USDCAD 1 day

US Inflation Decline Stalls

US Core PCE-Price Index was 2.8% y/y in February a tick higher than the upwardly revised 2.7% in January. %, compared to 2.6% last month. The results were “meh”—nothing to alter anyone’s view of the Fed outlook. Slow and steady wins the race.

Global Equity Indexes Fall

Trump’s tariffs and the risk of higher inflation have equity traders heading for the exits. Wall Street closed with losses and Asian equity markets followed suit except for the Australian ASX 200, which eked out a 0.16% gain. Japan’s Topix dropped 2.07%, and Hong Kong’s Hang Seng lost 0.66%. European bourses are in negative territory except for the UK FTSE 100 index which is up 0.19%. S&P 500 futures, are down 0.31% and the US 10-year Treasury yield dipped to 4.30% from 4.33%, while gold (XAUUSD) rose $23.78

EURUSD

NY Open: 1.0775, Overnight Range: 1.0768-1.0802

EURUSD is hanging tough in the wake of Trump’s latest tariff salvo. EU policymakers are in full defensive mode to avoid angering President Trump. The FT reports that they will only levy minimal fines on Apple and Meta for violating the EU Digital Markets Act. Another win for Donnie. Eurozone Economic, Sentiment, and Employment Expectations data fell. The Economic Sentiment Indicator (ESI) decreased 0.9 points to 96.0, and the Employment Expectations Indicator declined -0.7.

Traders remain on the defensive ahead of key US inflation data today and Tariff Tuesday.

GBPUSD

NY Open: 1.2950, Overnight Range: 1.2937-1.2969

GBPUSD caught a bit of a bid after UK Retail Sales surged 2.2% y/y in February, well above the forecast for a gain of 0.5%. Prices were also supported by news that the UK avoided a recession after Oct–December GDP rose 0.1%. Unfortunately, the Office of National Statistics (ONS) wrote that “Real GDP per head is estimated to have fallen by an unrevised 0.1% in Quarter 4 2024 and showed no growth across all of 2024.”

USDJPY

NY Open: 150.59, Overnight Range: 150.36-151.21

USDJPY retreated from its peak after Japanese inflation data rose more than expected. (Tokyo CPI actual 2.9%, forecast 2.8% y/y; ex fresh food and energy 2.2%, forecast 2.0%). The results raised the odds for a rate hike. The BoJ Summary of Opinions revealed policymakers were uncertain about the impact of Trump tariffs and inflationary pressures.

AUDUSD

NY Open: 0.6295, Overnight Range: 0.6281-0.6306

AUDUSD is on the defensive due to Tariff Tuesday and its impact on China, which is Australia’s largest trading partner. A break below 0.6250 targets 0.6150.

NZDUSD

NY Open: 0.5719, Overnight Range: 0.5712-0.5744

NZDUSD remained rangebound overnight and is trading with a negative bias. Bank of America analysts expect NZDUSD to underperform and that the RBNZ will cut rates by 25 bps at the April 9 meeting. Consumer Confidence dipped to 93.2 from 96.6 in February.

USDMXN

NY Open: 20.2779, Overnight Range: 20.2689-20.3486

USDMXN popped following news that Mexico’s jobless rate fell to 2.5% from 2.7% y/y. Yesterday, USDMXN rallied after Thursdays US data showed that the US economy was resilient with jobless claims and GDP a tick better than expected. The Banxico delivered its widely expected 50 bp rate cut taking its benchmark rate to 9.00%. The statement had a mildly dovish tilt and said the door for continued cuts was open.

FX high, low, open (as of 6:00 am ET)

China Snapshot`

PBoC fix: 7.1752 vs exp. 7.2591 (Prev. 7.1763)

Shanghai Shenzhen CSI 300 fell 0.44% to 3915.17

Xi Jinping has learned his lesson. China’s president had a penchant for locking up successful businessmen on trumped up anti-corutpion charges. His actions fostered the perception of an anti-business enviroment and investors fled in droves. Today, Xi Jinping met with a group of global investors to woo them back. He said “We are providing a transparent,steady and predictable policy environment. Embracing China is embracing opportunities.”

Sources: Yahoo Finance, Oanda, Investing.com, Bloomberg.