November 27, 2024

- Wall Street closes early today.

- FOMC minutes and today’s data confirm “slow and steady” pace.

- US dollar retreats except against MXN

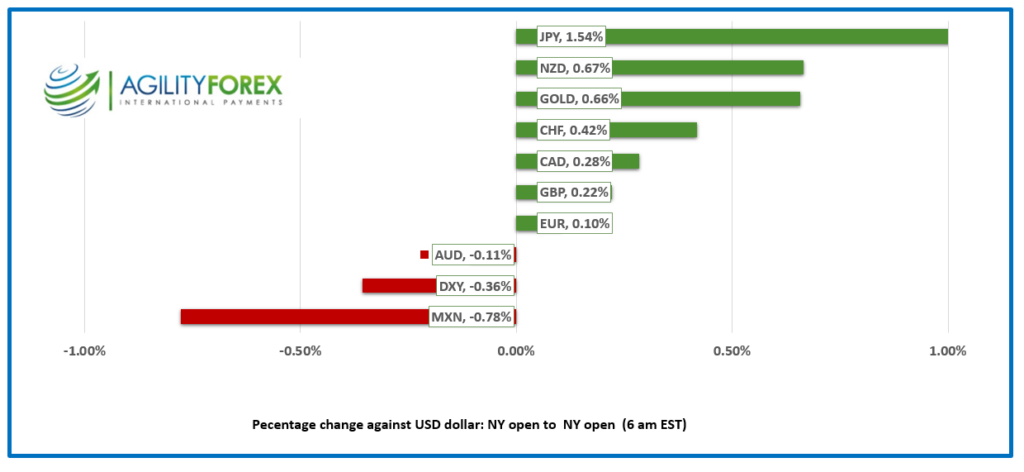

FX at a Glance

Source: IFXA/RP

USDCAD open 1.4049, overnight range,1.4035-1.4078, close 1.4056

USDCAD consolidated its gains following Trump’s bombshell tariff announcement and looks to have settled into a 1.4000-1.4100 range ahead of US Thanksgiving and the usual month-end portfolio rebalancing flows. Tuesday’s USDCAD spike to 1.4178 sets the stage for a generally bullish USDCAD outlook heading into Trump’s inauguration.

USDCAD does not face any headwinds from oil prices. The Israel/Lebanon cease-fire lowers the risk of a supply disruption from the middle east while Saudi Arabia’s rumored plans to boost production even has China’s economy struggles will limit gains. WTI traded in a 68.58-69.34 range overnight.

There are no Canadian economic reports today and trading activity will evaporate as US stock and bond markets close around 1:00 pm today.

USDCAD Technicals

The intraday technicals are modestly bearish while prices are below 1.4070 and looking for a break below 1.4030 to extend losses to 1.4000. A move above 1.4070 targets 1.4140.

Longer term, the USDCAD uptrend from October comes into play at 1.3970 and that line is guarding major support at 1.3820.

For today, USDCAD support is 1.4030 and 1.4010. Resistance is 1.4070 and 1.4140.

Today’s Range: 1.4010-1.4090

Chart: USDCAD daily

Source: Oanda.com

Data Dump May Be Offset by Holiday Scramble

The flurry of U.S. economic reports this morning, (Durable Goods Orders, ex Defense rose 0.4%, previous -0.9%) weekly jobless claims (actual 213,000, below forecast of 215,000) and Q3 GDP (as expected at 2.8% y/y gave the Fed plenty of ammunition to justify a gradual approach to easing monetary policy.

Many U.S. traders are also partaking in the annual Turkey Trot to head home for the holidays.

FOMC Minutes – All Fizzle, No Sizzle

The FOMC minutes were largely ignored, as the upcoming December 18 meeting will include updated forecasts and dot-plot projections. Meanwhile, Donald Trump’s comments, appointments, and trade threats are diverting attention away from the Fed.

Ceasefire in Lebanon

Lebanon and Israel agreed to a ceasefire. It remains unclear who negotiated on behalf of Hezbollah, as most of their senior leaders are deceased. The truce is likely temporary, lasting only until Iran can re-arm the group—something that may not occur until after Trump’s presidency. Trump’s disdain for Iran’s rulers and his firm stance on U.S. military action are likely deterrents.

EURUSD

EURUSD traded in a 1.0474–1.0539 range, receiving modest support after ECB board member Isabel Schnabel emphasized that interest rates should only be lowered gradually. The market expects ECB rates to drop from 3.25% to 1.75% by the end of 2025, but Schnabel appears less dovish. Weaker-than-expected German consumer confidence and the threat of a new trade war limited gains.

GBPUSD

GBPUSD edged higher overnight, trading in a 1.2567–1.2620 range. A broadly weaker U.S. dollar, EURGBP softness, and the prospect of steady UK interest rates (at 4.75%, higher than the rest of the G7) supported the pound.

USDJPY

USDJPY slid steadily, falling from 153.24 to 151.22. The decline reflects increased speculation that the BoJ may raise rates in December, coupled with a drop in the U.S. 10-year Treasury yield from 4.42% on Monday to 4.26% today.

AUDUSD and NZDUSD

AUDUSD: The pair climbed from 0.6463 to 0.6501, driven by broad-based U.S. dollar weakness. Australian inflation rose 2.1% in October, slightly below the 2.3% forecast. The trimmed mean CPI (Core CPI) increased to 3.5% y/y from 3.2% in September. The data is unlikely to prompt the RBA to cut rates before May 2025.

NZDUSD: NZDUSD rallied from 0.5826 to 0.5901 despite the RBNZ cutting the OCR by 50 bps. Many traders expected a 75 bps cut, but Governor Orr noted this was not even considered. The RBNZ’s outlook remains dovish, hinting at another 50 bp cut in February.

USDMXN

USDMXN traded quietly in a 20.5814–20.7425 range. The pair remains supported by Trump’s tariff threats and a dovish Banxico outlook. Falling inflation may push the central bank to accelerate rate cuts. Inflation in the first half of November dropped to 4.56%, below the 4.65% forecast.

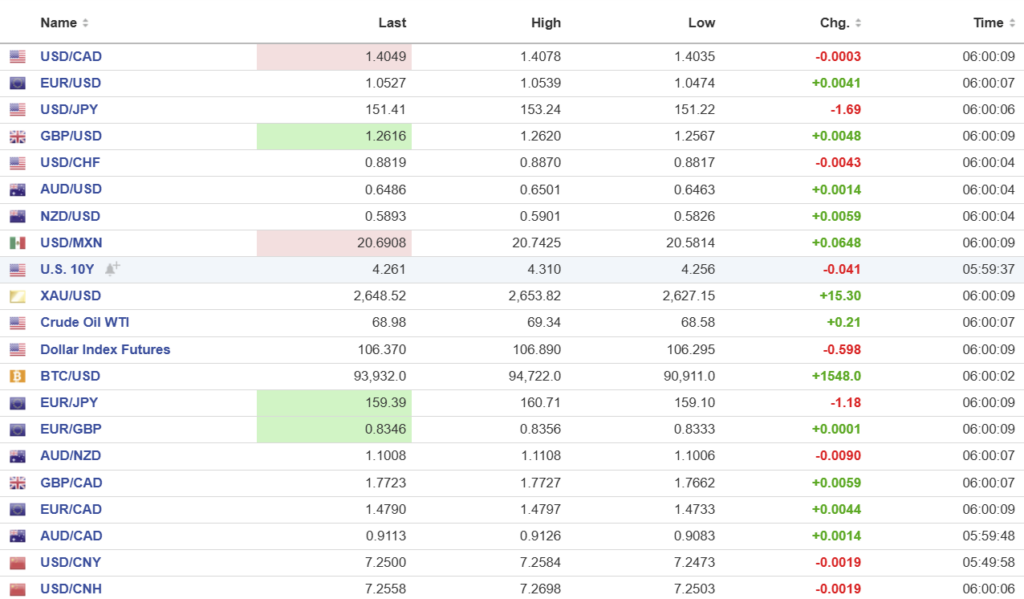

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

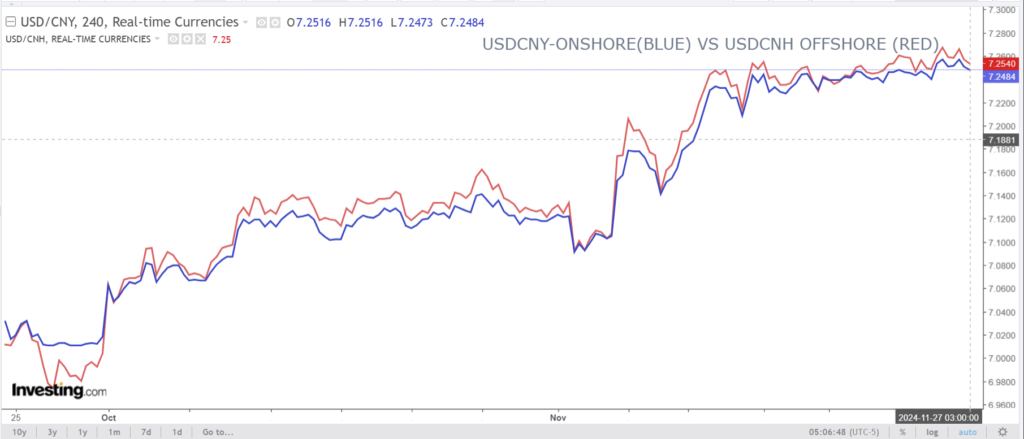

China Snapshot

PBoC Fix: 7.1982 (prev. 7.1910)

Shanghai Shenzhen CSI 300 rose 1.74% to 3907.04

PBoC Governor Pan Gongsheng hits a Reserve Ratio Requirement (RRR) before the endo for the year. The SCMP notes: “The average RRR for Chinese banks stood at 6.6 per cent as of September 27, with larger institutions required to hold 8 per cent of their deposits as reserves, while medium-sized banks must hold 6 per cent and small banks must hold 5 per cent.”

Trump’s nomination of Jamieson Greer at US Trade Representative is expected to take a hard-line approach to trade negotiations with China.

Chart: USDCNY and USDCNH

Source: Investing.com