Source: YouTube ABC Sunday Night Football

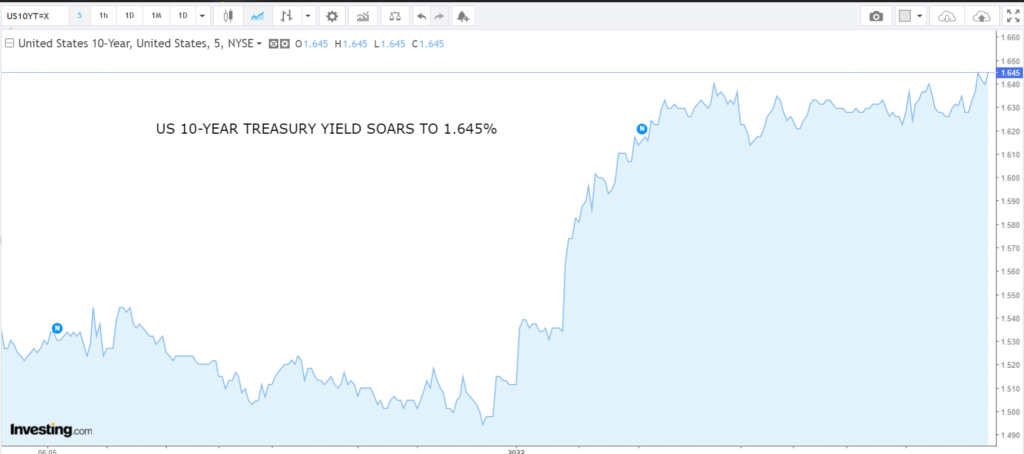

- US 10-year Treasury yield soars to 1.645%

- FOMC minutes Wednesday, NFP Friday

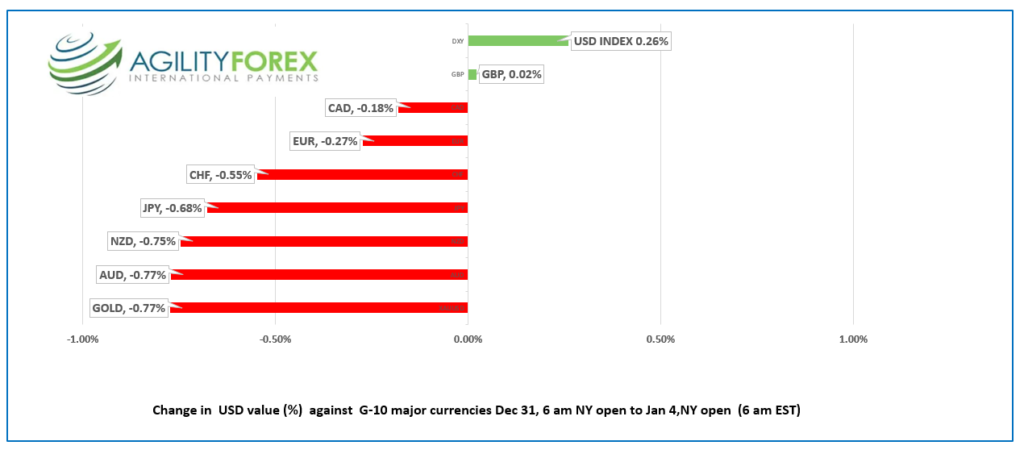

- US dollar opens with gains compared to year end; GBP unchanged

FX at a Glance

Source: IFXA Ltd/RP

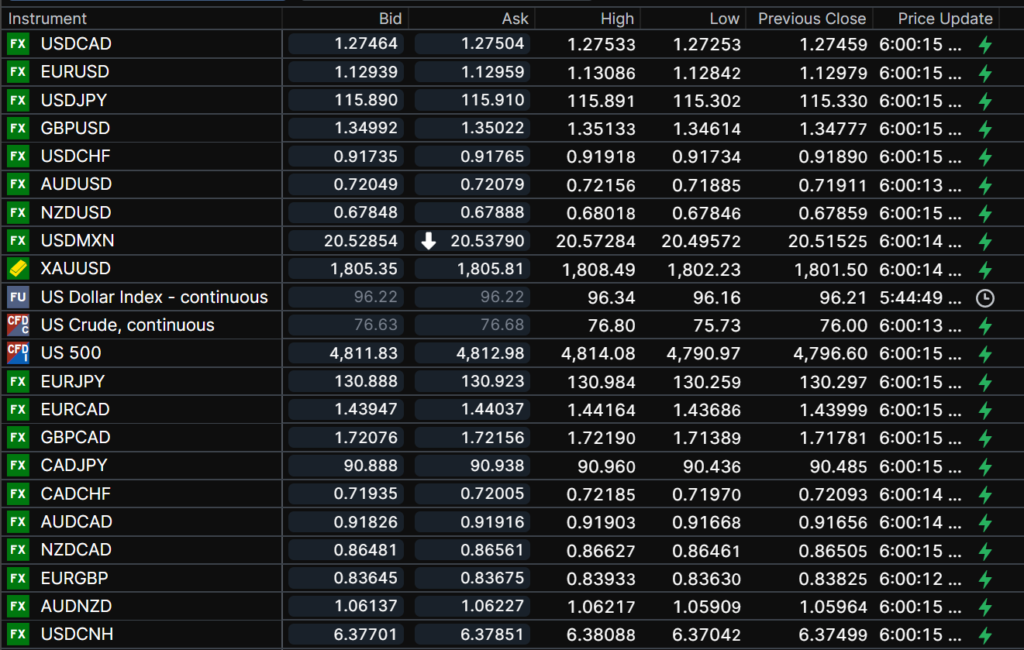

USDCAD Snapshot: Open 1.2746-50, Range-Dec 31 close-Jan 4 open 1.2626-1.2774, Dec. 31 close 1.2641

USDCAD is consolidating gains made since closing at 1.2641 on New Year’s Eve. The year-end sell off made the Canadian dollar the best performing G-10 currency in 2021, with a gain of 0.65%, which is rather anti-climatic after trading in a 1.2020-1.2965 band in 2021.

The year end drop to 1.2626 was due to month and year end portfolio rebalancing flows, while the rebound to 1.2774 on Monday was due profit-taking, and the surge in the US 10-year Treasury yield, in a thin market as many centers including the UK were closed.

USDCAD gains will be slowed by steady to firm WTI oil prices, which are underpinned due to ongoing production issues, falling US crude inventories, and hopes the Omicron variant will not seriously derail global growth. The OPEC meeting is today, and the cartel is expected to reaffirm plans to increase February production by 400,000 b/day.

USDCAD price action will track broad US dollar moves with a slew of top-tier economic data releases on tap this week, including Canadian and US employment reports and the FOMC minutes from the December 15 meeting.

Technical view: The intraday USDCAD technicals are bearish below the 1.2750-70 area, looking for a break below 1.2710 to extend losses to 1.2630. The drop below 1.2740 on December 31 snapped the October uptrend line, and the subsequent rebound is merely a correction while prices are below 1.2770. A break below 1.2630 will target 1.2540.

For today, USDCAD support is at 1.2720 and 1.2670. Resistance is at 1.2750 and 1.2790. Today’s Range 1.2690-1.2770

Chart USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Welcome back! It is a data-rich week with top-tier economic reports from the EU, UK, US, and Canada on tap, as well as the minutes from the December 15 FOMC meeting.

A surge in US 10-year Treasury yields from 1.497% on December 31 to 1.645% this morning shifted FX focus from Omicron to the outlook for US interest rates. The debate is raging as to whether the rally is merely due to banks and others unwinding cautionary balance sheet positions or a belief that US rates will be rising higher and faster than expected.

The first day of equity trading in the US ended with the S&P 500 and DJIA closing at new record highs. Apple (AAPL: NASDAQ) closed with a valuation over $3.0 trillion. Is that a sign of “irrational exuberance, a phrase made famous by former Fed President Alan Greenspan in 1996, when commenting about stock prices? Yes! Apple went public in November 1980 and took 38 years to reach $1.0 trillion in value. A mere 3.4 years later, it gained another $2.0 trillion.

EURUSD ended 2021 at 1.1372, then dropped steadily to start 2022, falling to 1.1276 in NY today. The retreat is due to renewed US dollar demand following the surge in US Treasury yields which underscored the divergent ECB and Fed interest rate outlooks. In addition, profit-taking, and concerns about short-term pain from the Omicron outbreak in the Euro area, are weighing on prices. Manufacturing PMI and German employment reports were as expected. EURUSD remains rangebound in a 1.1220-1.1380 band.

GBPUSD rallied to 1.3547 on New Year’s Eve, then dropped to 1.3435 yesterday due to profit-taking and broad US dollar demand. Prices recovered to 1.3514 in Europe supported by better than expected December Manufacturing PMI data (actual 57.9 vs 57.6 in Nov.) The technicals are mildly bullish above 1.3430.

USDJPY is riding the US Treasury yield rally, rising from 115.11 at the December 31 close to 116.17 in NY today.

AUDUSD and NZDUSD tracked broad US dollar moves, and both currency pairs are lower than their December 31 closing rates.

US ISM Manufacturing PMI (forecast 60.2vs November 61.1) is ahead.

Chart of the Day: US 10-year yield

Source: Investing.com

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

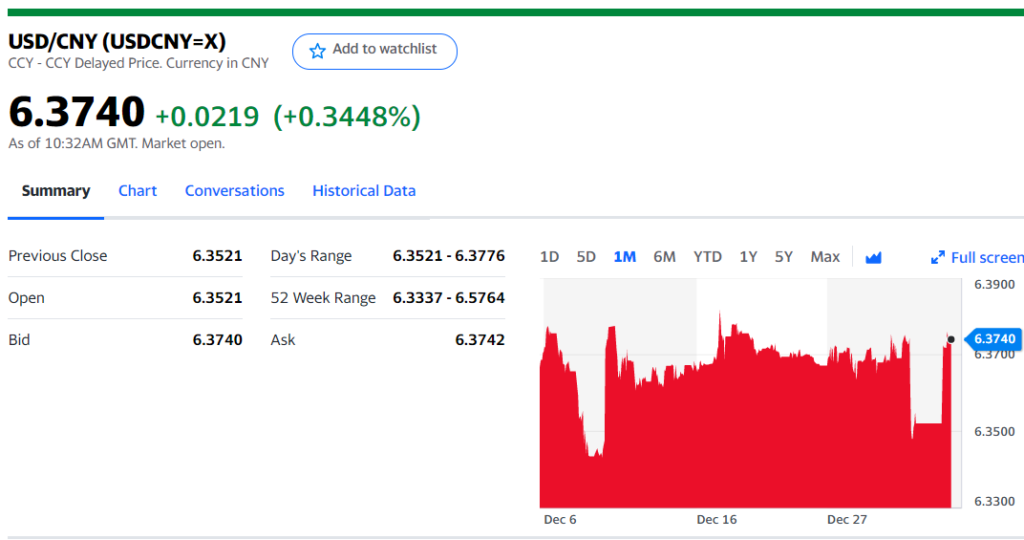

China Snapshot

Today’s Bank of China Fix 6.3794, Jan 3: 6.3757

Shanghai Shenzhen CSI 300 rose 0.38% to 4,9240.36

Caixin December Manufacturing PMI 50.9 vs November 49.9

Chart: USDCNY 1 month

Source: Yahoo Finance