Photo: hdclipartall.com

February 22, 2023

- RBNZ hikes 50 bps, suggests rates going even higher.

- Geopolitical tensions remain elevated.

- US dollar consolidates gains ahead of FOMC minutes.

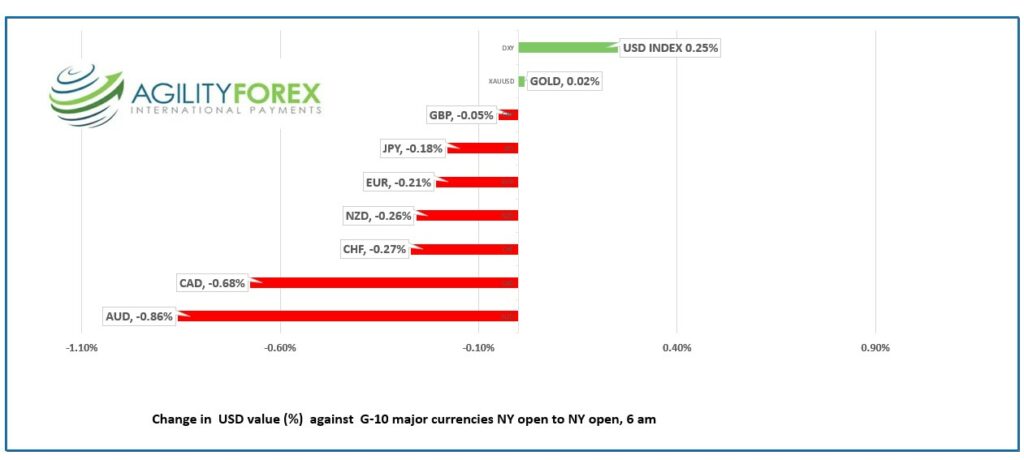

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3554-58, overnight range 1.3516-1.3559, close 1.3537

USDCAD rallied yesterday due to US rate hike concerns, geopolitical tensions and cooler than expected Canadian inflation.

Source: Bank of Canada

BoC Governor Tiff Macklem is feeling rather smug as the lower CPI data supports his decision to pause rate hikes.

USDCAD rallied from 1.3440 to 1.3546 due to the data, but also because of broad-based US dollar demand in the wake of the US 10-year yield climbing from 3.84% to 3.962%. Widening CAD/US interest rate differentials are supporting USDCAD.

WTI oil prices fell from $77.48/b yesterday to $74.99/b overnight mainly due to US dollar strength. Prices have bounced between $75-$80/barrel for two weeks, but Opec, EIA, and IEA analysts continue to forecast rising demand, and higher prices this year.

The New Housing Price Index fell 0.2% m/m (forecast -0.1%, previous 0%) Prices rose 2.7% y/y compared to Decembers reading of 3.9% y/y.

USDCAD Technical Outlook

The hourly USDCAD technicals are bullish above 1.3460, looking for a decisive break above 1.3560 to extend gains to 1.3850. However, this mornings drop below 1.3530 suggests a retest of the 1.3460 uptrend line.

Longer term, the daily chart indicates that the RSI has peaked and is turning lower and that a break below 1.3480 will open the door to a test of 1.3350 support.

For today, USDCAD support is at 1.3460 and 1.34100. Resistance is at 1.3550 and 1.3580.

Today’s range 1.3460-1.3560.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Traders have worked themselves into a lather in the run-up to the release of the minutes from the February 1, FOMC meeting. They bought bonds, US dollars, while selling stocks and commodities, due to concerns that the minutes may reveal that policymakers are hawkish.

Well, Doh!

Fed Chair Powell and his colleagues repeatedly warned that it was far too early for rate cut speculation as the Fed hasn’t finished the tightening cycle. The FOMC minutes will not change that sentiment which suggests recent moves are likely to be unwound.

However, market reversals may be limited as comments from President Biden, President Putin, Russian Deputy Chair of Security council Medvedev and Chinese diplomat Wang Yi, stoke geopolitical tensions.

EURUSD traded narrowly in a 1.0626-1.0663 range. News German Ifo expectations improved (actual 88.5, previous 86.4) while inflation met expectations limited downside.

However, somewhat dovish remarks by ECB board member Francois Villeroy limited gains. He said “There’s been an excess of volatility on expectations for the terminal rate.” His comments didn’t prevent Deutsche Bank from raising its terminal rate forecast to 3.75% from 3.25%.

GBPUSD traded firmly in a 1.2065-1.2134 range, as it continued to benefit from better-than-expected PMI data released yesterday.

USDJPY see-sawed in a 134.38-135.05 band supported by the US 10-year yield consolidating gains in the 3.94% area.

AUDUSD dropped to 0.6813 from 0.6864 due to weak wage growth data easing fears of aggressive RBA rate hikes and by and broad US dollar strength.

NZDUSD traded between 0.6208 and 0.6250 due to the perception the RBNZ is more hawkish than expected, following the 50 bp rate hike. The Overnight Cash Rate (OCR) is 4.75% and analysts are forecasting further hikes to 5.50%. The RBNZ ignored said it was too early to assess the impact of Cyclone Gabrielle on monetary policy.

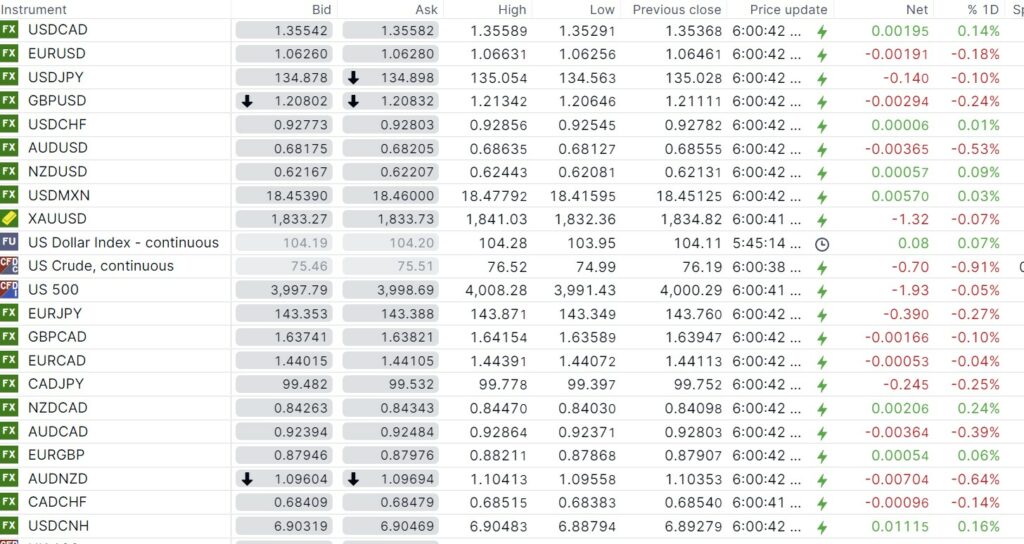

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

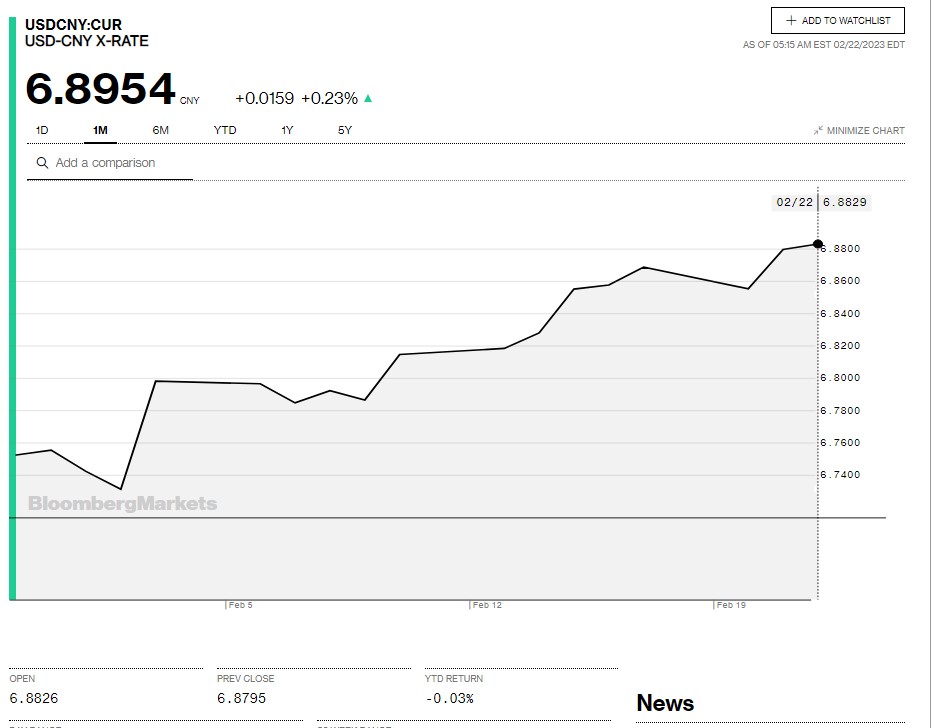

China Snapshot

Bank of China Fix: 6.8759, Feb. 20, Previous: 6.8557

Shanghai Shenzhen CSI 300 fell 0.90%% to 4106.95.

Chart: USDCNY 1 month

Source: Bloomberg