Photo: Pixabay

- US Core-CPI fell to 6.0% y/y from 6.3%

- BoC’s Macklem admits policy errors-will now use data to make decisions

- US dollar opens modestly firmer from yesterday-CAD outperforms

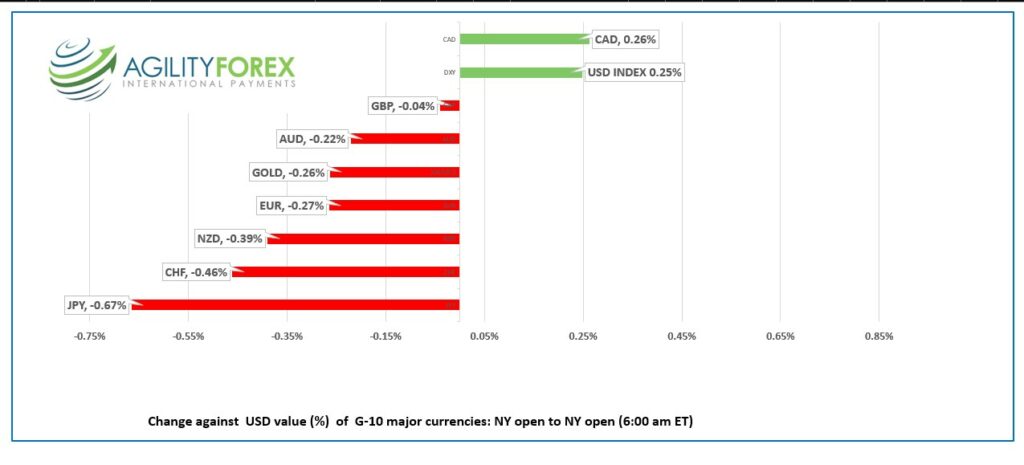

FX at a glance:

Source: IFXA Ltd/RP

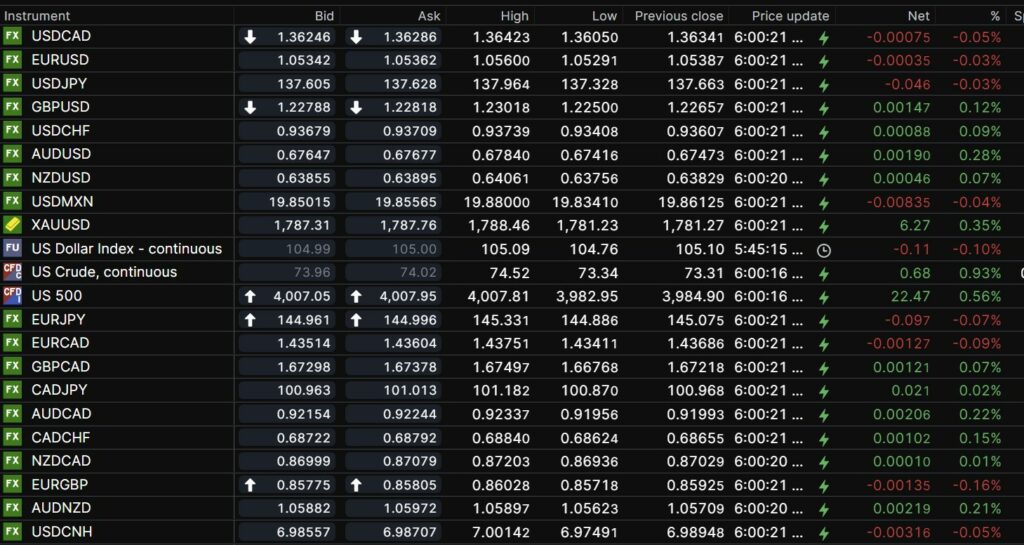

USDCAD Snapshot: open 1.3625-29, overnight range 1.3523-1.3642, close 1.3634

USDCAD plunged to 1.3524 from 1.3604 following the lower-than-expected headline and core US CPI data. CPI rose 7.1% y/y in November compared to 7.7% y/y in October The results will encourage further speculation that the Fed is close to its peak rate in this cycle.

Yesterday, BoC Governor Tiff Macklem did not provide much insight into last week’s monetary policy decision. The BoC hiked rates 50 bps and then suggested it was the last hike of this cycle. The speech was mostly a defence for the BoC’s bungled reaction to inflation warning signs and blamed their inflation models.

Risk sentiment is mildly positive after reports that China and Hong Kong continue to relax covid-zero restrictions, and on hopes for a lower-than-expected US inflation result.

WTI oil rallied on the improved risk sentiment and consolidated Monday’s gains in a $73.34-$74.52/b range then reached $74.71/b, post CPI. Prices are supported on hopes for renewed demand from China, and by a major leak which forced the shutdown of the Keystone pipeline for a loss of 600,000 barrel/day.

USDCAD technical outlook.

The intraday USDCAD technicals are bearish below 1.3630 with the break below 1.3550 opening the door to a test of the November uptrend line in the 1.3450-60 zone. A rally above 1.3630 suggests further 1.3450-1.3700 range trading

For today, USDCAD support is at 1.3510 and 1.3470. Resistance is at 1.3560 and 1.3640

Today’s range 1.3510-1.3590.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The cooler than expected US headline CPI report (actual 7.1% y/y vs forecast 7.3%, October 7.7%) and Fed Chair Powell’s favourite measure, Core-CPI (actual 6.0% vs forecast 6.1%, October 6.3%) fueled a US dollar sell-off and a 3.07% gain in S&P 500 futures.

The US 10-year yield plunged to 3.448% from a pre-CPI level of 3.61%.

The market reaction is exaggerated du to thin year-end markets. As many pundits noted, it is just one data point and Jerome Powell is on record saying he needs to see evidence of a steady decline.

Nevertheless, it encourages the “inflation is peaking” story.

Profit-taking has knocked S&P 500 futures down from its post-CPI peak and lifted the US dollar from its lows. The focus has shifted to Fed Chair Powell’s press conference, and the updated Summary of Projections on Wednesday and the Argentina vs Croatia World Cup semi-final today.

EURUSD bounced erratically in a 1.0529-1.0560 range overnight the soared to 1.0661 in NY trading after the US data. Prices were also supported by improved German inflation data (actual 10.0% y/y in vs 10.4% in October. ZEW economic sentiment in German and the Euro zone was better than expected at -23.3 and -23.6 respectively. The EURUSD technicals are bullish and look for a test of 1.0770.

GBPUSD accelerated to 1.2438 in NY from an Asian low of 1.2250 The gains were underpinned by strong employment weekly earnings data. (actual 6.1% 3 months, y/y vs 5.8% previously.)

USDJPY reversed its overnight gains and plunged from 137.96 to 134.96 when the US 10-year Treasury yield dropped to 3.448%. with prices underpinned by the rebound in the US 10-year yield to 3.61%.

AUDUSD climbed from 0.6742 to 0.6876 on broad US dollar weakness and higher Westpac Consumer Confidence.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

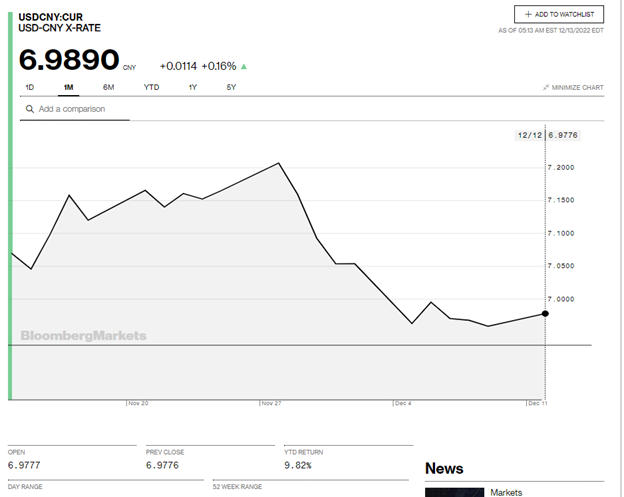

China Snapshot

Today’s Bank of China Fix: 6.9746, previous 6.9565

Shanghai Shenzhen CSI 300 fell 0.20%% to 3945.68

China-Hong Kong quarantine free- travel to be permitted in January.

Japan and Netherlands have agreed in principle to join US in tightening controls of advanced chip making equipment to China.

Chart: USDCNY 1 month

Source: Bloomberg