The Bank of Canada hiked its overnight interest rate to 0.75 percent on July 12. It was a big deal as it was the first rate increase since June 2010.

The Canadian dollar soared, gaining 1 ½ cents in minutes. The move was not a direct result of the rate increase because the Bank of Canada had done a very good job about telegraphing its intentions throughout the past weeks.

Instead, it occurred due to other factors. They included; the upbeat tone of the statement, tweaks to growth forecasts in the Monetary Policy Report and comments by Governor Poloz at the press conference.

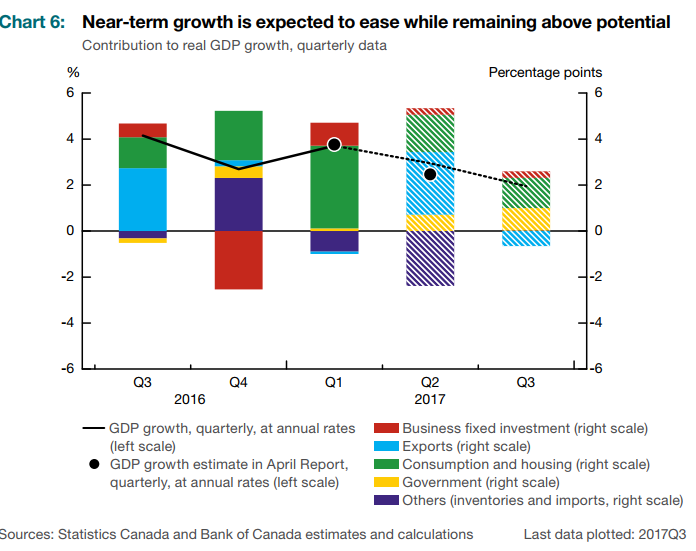

In the policy statement, the Bank expressed confidence in its outlook for above-potential growth. They acknowledged recent soft inflation data but dismissed it as temporary. They tweaked their 2018 and 2019 GDP forecasts, raising the former to 2.8% from 2.6% and the latter by 0.1% to 1.9%.

The BoC isn’t bothered about the soft inflation data seen recently. They are chalking it up to “temporary factors” attributed to an easing of consumer energy and automobile price inflation.

The Bank of Canada also noted that the economy was absorbing excess capacity more rapidly than previously anticipated. They now forecast the “output gap” to close “around the end of this year” rather than sometime in 2018.

Although the Bank expects near term growth to ease it will still be above its potential.

USDCAD traders appear to have been caught off-guard by the hawkish tone in the statement and press conference. Some expected a mere shift in tone which would have set up a rate increase in September. They weren’t prepared for the prospect of two more increases in the next six months.

USDCAD crashed below key support at 1.2860 and is targeting further losses to 1.2500 or 80 cents.

Of course, oil prices will have a role to play in further Canadian dollar gains.

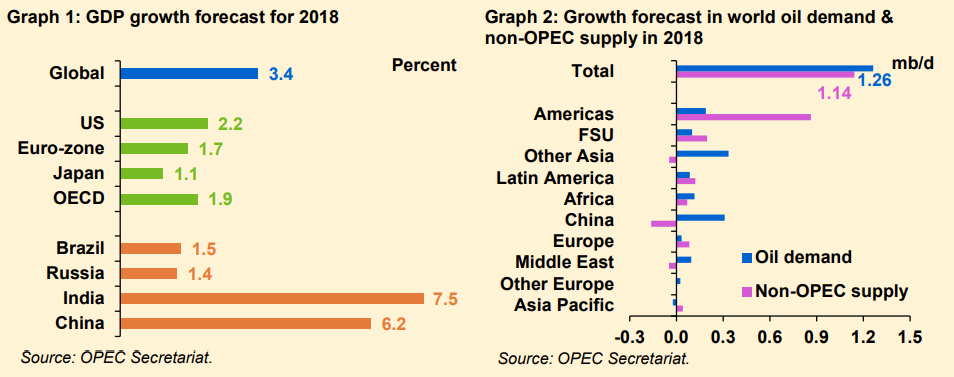

Opec’s Monthly Oil Market Report was released July 12. It raised questions about the sustainability of oil prices at current levels.

Opec crude production increased. That was thanks to Libya and Nigeria pumping more and because Saudi Arabia exceeded its production cap. The Saudi’s claimed the oil production increase was needed to serve domestic power stations due to heavy air conditioning demand at this time of year.

Opec predicted a tiny decrease in 2018 demand for Opec crude of about 1,000 barrels a day, which in the context of global production, is just spillage.

If oil prices continue to trade in the $42.00-$48.00/barrel area, they should not pose much of a problem for the Canadian dollar.

However, despite the Bank of Canada’s upbeat outlook for the Canadian economy, there are still a couple of 800 pound elephants in the room.

Those elephants are the US Federal Reserve and the Nafta renegotiations.

Federal Reserve Chair Janet Yellen testified before Congress on July 12. Markets considered her testimony to be doveish. The evidence was in the falling US dollar against the majors, a drop in Treasury yields and a jump in stock prices.

She said that rate increases would be gradual. The kicker came when she opined that the Fed is ready to “adjust policy if necessary, if it appears that the inflation undershoot will be persistent. Some took that to mean rate cuts were still a risk.

As it stands now, less than 50 percent of market participants expect the Fed to raise rates again, by the end of the year.

If that is the case, the Canadian dollar may rise further, considering the Bank of Canada is forecast to raise interest rates again in September or October.

But before those rate increases happen, August heralds, the start of the North American Free Trade Agreement renegotiation.

In preparation for that, Prime Minister Justin Trudeau is addressing a national conference of state governors on July 13 or 14 in Rhode Island.

Aside from adding to his selfie collection, he is expected to highlight the benefits of trade with Canada. He is also holding an official bilateral meeting with US Vice President Mike Pence.

The official negotiations are expected to begin after August 16.

President Trump is on record for calling Nafta the “worst deal ever.” He needs a victory. He has been unable to repeal Obamacare, his tax cut plans are still plans, not reality and he is mired in a mess of election intrigue over his relationship with Russia.

He may be looking to Justin to bolster his political fortunes. President Trump is known for his book “The Art of the Deal.” Prime Minister Trudeau is famous for saying “budgets balance themselves.” At first glance, the Trump/Trudeau matchup looks as even as a Mayweather/Peewee Herman title bout.

The outlook for the Canadian dollar is looking rather rosy thanks to the possibility of further interest rate increases while the Fed takes a breather. Nevertheless, there are other events lurking which could knock the loonie to the canvas.