Source: Clip-art-Library.com

- Bank of England Intervenes in bond markets

- Nord Stream pipeline sabotage sinks stocks and bonds

- US dollar surges on renewed risk aversion

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3803-07, overnight range 1.3711-1.3831, close 1.3724

USDCAD is having a wild and woolly morning after a whacky overnight session. Bank of England bond market intervention is roiling currency and bond markets, already unsettled by month and quarter end portfolio rebalancing flows, and negative global risk sentiment.

USDCAD peaked at 1.3831, just ahead of the BoE news and then dropped to 1.3711 by 5:30 am PDT.

WTI oil traded in a $76.59/barrel-$80/b range overnight with the peak reached in NY trading followed the US dollar retreat, post-BoE.

News that API reported crude inventories rose 4.1 million barrels in the week ending September 23 was overshadowed by supply disruption concerns from Hurricane Ian. There is talk that Opec is considering larger production cuts in the face of rising global recession risks.

There are no Canadian economic reports today.

USDCAD Technical outlook

The USDCAD technicals are bullish following the move above the 1.3680-1.3710 yesterday, which will now function as support. The intraday uptrend is intact above 1.3710, looking for a break of 1.3760 to retest the overnight 1.3830 peak. A move below 1.3680 targets 1.3630.

Long-term Fibonacci retracement analysis projects a test of 1.4490 following the break above 1.3450.

For today, USDCAD support is at 1.3740 and 1.37100. Resistance is at 1.3810 and 1.3850. Today’s range: 1.3750-1.3850.

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

“Beep Beep” UK bond bears got run over.

The Bank of England roiled global financial markets with a surprise intervention to buy bonds.

The BoE announced plans to “carry out temporary purchases of long-dated UK government bonds from 28 September. The purpose of these purchases will be to restore orderly market conditions.”

The Bank justified the action because of “significant repricing of UK and global financial assets. This repricing has become more significant in the past day – and it is particularly affecting long-dated UK government debt. Were dysfunction in this market to continue or worsen, there would be a material risk to UK financial stability. This would lead to an unwarranted tightening of financing conditions and a reduction of the flow of credit to the real economy.”

Effectively the Bank of England has restarted “Quantitative Easing” at the same time they are raising interest rates. Hmm-is Homer Simpson in charge?”

Overnight markets were choppy thanks to a new wave of risk aversion following news the European-critical Nord Stream pipeline was sabotaged. It would have been worse, but Russia wasn’t pumping any gas. Nevertheless, the blast will hamper the flow of energy to Europe this winter.

Hawkish Fed rhetoric helped keep the focus on the Fed and its plans to keep raising interest rates and the US dollar bid. There is more to come today, but the message is becoming stale.

Even so, it was enough to convince bond traders to dump Treasuries which drove the US 10-year yield to 4.019% overnight. Then the BoE acted, and everything changed.

The US 10-year yield dropped to 3.888% and S&P 500 futures rallied from the session low to positive territory. The US dollar plunged with the commodity bloc currencies returning to Tuesday’s closing levels.

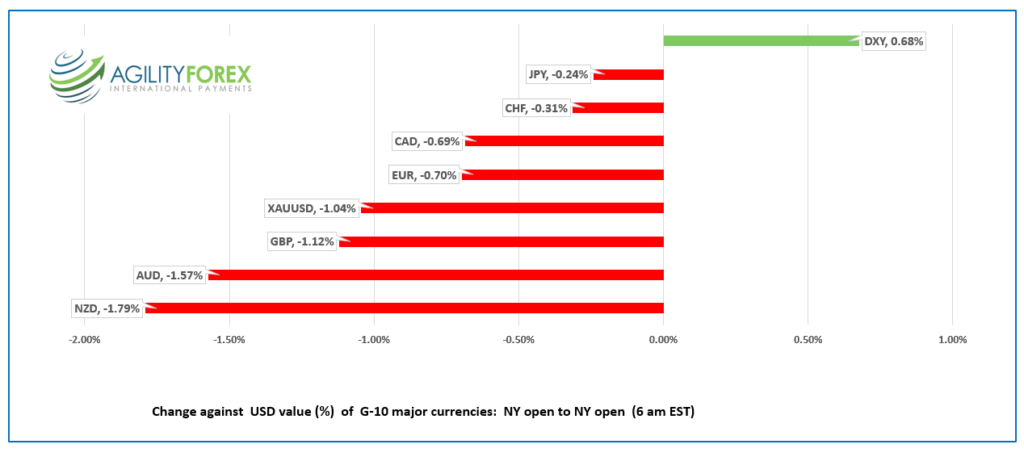

GBPUSD traded choppily in a 1.0625-1.0738 range overnight until the BoE bond market action. GBPUSD soared to 1.0838 in a heart-beat before settling back to 1.0670. The currency is far from being out of the woods and the bounced just means it has that much further to fall.

EURUSD dropped from 0.9600 to 0.9537 as the Nord Stream pipeline sabotage added to the Euro area’s woes. Prices recovered to 0.9587 in NY. The single currency is pressured by the risk of a worsening energy crisis, political concerns around the new Italian government, and widening US and ECB interest rate spreads.

USDJPY traded in a 144.40-144.86 range, supported by the rise in US Treasury yields but traders were reluctant to test the resolve of the Bank of Japan which is expected to intervene around 145.00. The BoJ monetary policy minutes from the July 20 meeting were a non-event.

AUDUSD traded in a 0.6365-0.6443 range with price action directed by broad US dollar moves. Australia Retail Sales rose 0.6% m/m in August, better than the 0.4% expected.

NZDUSD was the worst performing G-10 currency since yesterday’s open, falling 1.79% with the weaker before recovering its losses in NY.

Fed Chair Powell delivers opening remarks at the 2022 Community Banking Research conference at 7:15 am PDT.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Today’s Bank of China Fix: 7.1107, previous 7.0722

Shanghai Shenzhen CSI 300 fell 1.63% to 3,828.71

USDCNY at highest level since 2008. PboC warns against bets against the yuan.

Chinese authorities plan to “tweak” Yuan Fixing. Reuters reports that officials ask 14 banks to include a “counter-cyclical factor” (or X factor) in their fixing calculations, which effectively puts a bias into calculations.

Chart: USDCNY 1 month

Source: Bloomberg