May 28, 2024

- Canadian data increases inflation risk.

- Risk sentiment improves on anticipation of soft PCE Price data

- US dollar inches lower in positive risk environment.

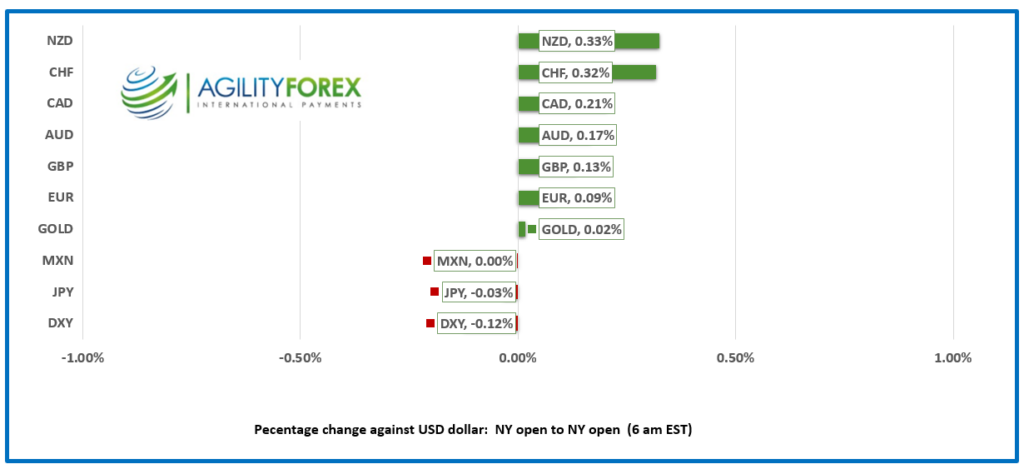

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3626, overnight range 1.3614-1.3637, close 1.3636

USDCAD slipped alongside general bearish US dollar sentiment and renewed hopes for an earlier than expected Fed rate cut. That is partially offsetting risks of renewed USDCAD demand from a Bank of Canada rate cut on June 5.

However, the BoC may not be so eager to cut rates after today’s Canadian Industrial Product Price and Raw Materials Prices Indexes which rose more than expected. Industrial Prices rose 1.5% m/m in April, well above the forecast for a 0.6% gain and the upwardly revised 0.9% March result. The Raw Material Price index soared 5.5 % (forecast 3.2% m/m) but the March result was revised lower.

WTI oil prices moved higher, rising from 77.69 to 79.22 on rising risks of middle east crude supply disruption after Israeli’s killed an Egyptian soldier near Rafah. In addition Opec is expected to extend production cuts at its June 6 meeting.

USDCAD Technicals

The intraday USDCAD technicals are bearish with the break below 1.3630 setting up a test of support in the 1.3580 area. A break above 1.3630will delay the move but only a break above 1.3730 will negate the downside pressure.

The longer term uptrend from January 2024 is intact while prices are above 1.3550. That trendline is supported by the 100 and 200 day moving averages at 1.3568 and 1.3570, respectively.

For today, USDCAD support is at 1.3580 and 1.3550. Resistance is at 1.3640 and 1.3680. Today’s range is 1.3580-1.3640.

Chart: USDCAD daily

Source: DailyFX

“What Me Worry?”

Once again, traders have embraced Alfred E. Neuman’s carefree, blissfully ignorant attitude toward life. They merely shrug their shoulders on news about Russia’s latest advances into an ammunition-depleted Ukraine, Hamas using Palestinians as human shields in order to launch missiles into Israel, China’s overt hostility to Taiwan, and Iran’s nuclear ambitions. They only care about the data-dependent Fed’s intention for interest rates. Fed officials continue to warn that US rates need to remain at elevated levels for longer while traders have decided that recent soft CPI and PPI data mean that Friday’s PCE Price index will be weak as well and are pricing a 48% chance for a rate cut in September.

Where has all the Volatility Gone?

A calm has descended over the US Treasury market. The US 10-year Treasury yield has been locked into a 4.44-4.50% range for the past week and that sense of calm has improved global risk sentiment. The US dollar is on the defensive as a result. Maybe today’s US Case-Shiller Home Prices and Consumer Confidence reports will give volatility a boost.

EURUSD

EURUSD is at the top of its 1.0854-1.0880 range due to speculation of a soft US PCE price report on Friday, which has offset dovish comments from ECB policymakers yesterday. EURUSD is unlikely to break out of the existing 1.0800-1.0900 range until Friday’s US PCE price report.

GBPUSD

GBPUSD inched higher in a 1.2761-1.2784 range due to general US dollar weakness and an absence of actionable UK economic data. Last week’s higher-than-expected inflation result and Rishi Sunak’s snap election call, which led to BoE officials cancelling all public engagements, suggest GBPUSD may remain bid.

USDJPY

USDJPY inched higher in a 156.62-157.00 range, boosted by steady US Treasury yields. However, gains were slowed by a steep jump in the Corporate Service Price Index, which rose to 2.8% y/y in April from an upwardly revised 2.4% in March. The gains support the case for a BoJ rate hike. Meanwhile, the ongoing demand for the carry trade (sell JPY and buy higher-yielding US dollars) will continue to limit the BoJ’s ability to sustain intervention-driven USDJPY moves lower.

AUDUSD AND NZDUSD

AUDUSD drifted sideways in a 0.6653-0.6674 range, supported by broad-based US dollar weakness and by a tepid April Retail Sales report (actual -0.1% m/m vs forecast 0.2% and previous -0.4%). Even so, the RBA is not expected to cut interest rates until May 2025.

NZDUSD traded narrowly in a 0.6148-0.6166 band. Kiwi traders are awaiting Business confidence data tomorrow, the Government budget, and Governor Adrian Orr’s speech on Thursday.

USDMXN

USDMXN is little changed from yesterday and is in the middle of its 16.6456-16.7117 overnight range. Price action is subdued ahead of Friday’s US PCE-Prices data and the June 2 Mexican election, for which Mexico City Mayor Claudia Sheinbaum is widely expected to win the Presidential election.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1101 vs exp. 7.2402 (prev. 7.1091).

Shanghai Shenzhen CSI 300 fell 0.73% to 3609.17

Chart: USDCNY and USDCNH

Source: Investing.com