March 15, 2024

- Markets in wait and see mode ahead of March 20 FOMC meeting.

- Treasury Yields hold on to gains,

- US dollar opens with gains all around.

FX at a Glance

Source: IFXA/RP

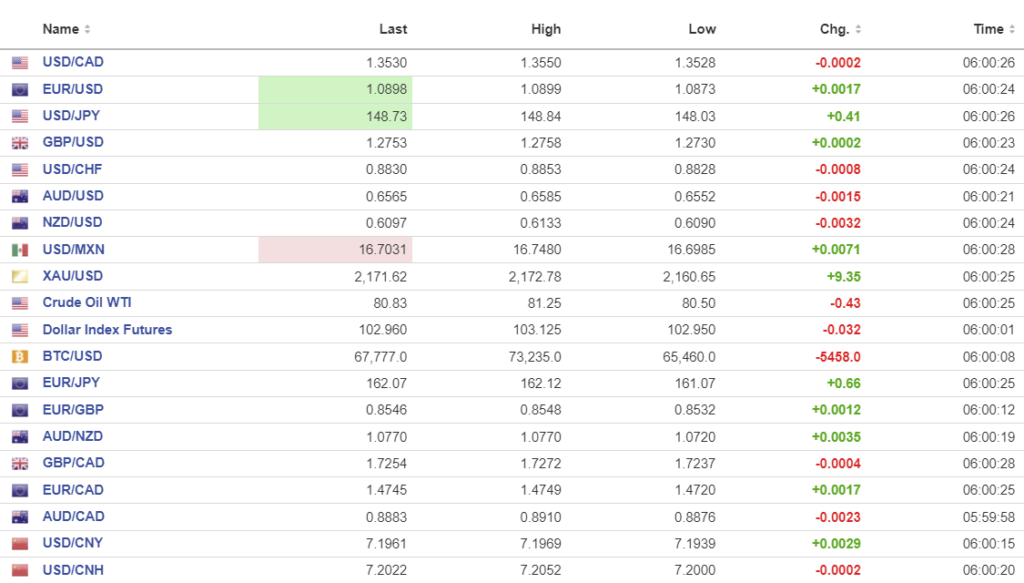

USDCAD Snapshot: open 1.3528-32, overnight range 1.3525-1.3550, close 1.3535

USDCAD rallied on the back of surging US Treasury yields and concerns that the BoC could cut interest rates sooner than the Fed. The gains are supported by Canada’s lagging economic growth and sharp declines in direct foreign investment, which many attribute to the government’s hostile business practices, including unrealistic climate change goals and soaring carbon taxes.

Government spending has risen to such levels that Desjardins Bank economists suggest the Liberal government will be forced to hike corporate taxes. The government’s mandate that all new passenger vehicles and light trucks must have zero emissions by 2035 is as ridiculous as having a convicted criminal eco-terrorist as Environment Minister. But we do. The Fraser Institute says the government’s ill-thought plan would require the construction of ten new mega dams, comparable to BC’s Site C, on Canadian rivers or thirteen new average-sized gas plants. “Buddy, can you spare a dime?”

WTI oil traded in a $80.50-$81.25 range, which may have served to slow USDCAD gains.

Canadian Housing Starts and Wholesale Sales reports are ahead.

USDCAD Technicals

The USDCAD intraday technicals turned bullish with the breach of resistance at 1.3505 (100-day moving average) and again at 1.3530 yesterday while snapping the week-long downtrend. USDCAD is vulnerable to further gains to 1.3610.

Longer term, USDCAD continues shuffle between 1.3300 and 1.3600. Momentum indicators are neutral which supports further upside to the top of the range.

For today, USDCAD support is at 1.3510 and 1.3470. Resistance is at 1.3560 and 1.3590. Today’s range is 1.3470-1.3570

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX

Julius Caesar did not have a good day on this date in 44 BC (Biden was just a teenager), and US dollar bears may be suffering a similar fate. In just three months, analysts have shifted from predicting 150 basis points of Fed rate cuts in 2024 to just 50 basis points. CME futures traders are less certain, seeing about a 67% chance for three rate cuts. Today’s US data won’t change that outlook, but to paraphrase Desi Arnaz, “Mr. Powell, you’ve got some ‘splainin’ to do.”

Asian equity indexes followed Wall Street lower. Australia’s ASX 200 closed down 0.56% while Japan’s Nikkei 225 index lost 0.26% and the Hong Kong Hang Seng index dropped 1.42%. European bourses are treading water but are in the green. S&P 500 futures are up 0.20%.

The 10-year Treasury yield surged from 4.04% on March 8 to 4.30% yesterday and is steady at 4.277% today. Hotter than expected inflation data and the downgraded Fed rate cut outlook are underpinning prices.

EUR/USD is at the top of its 1.0873-1.0900 overnight range. Dovish comments by ECB officials this week combined with US data that projects just two Fed rate cuts in 2024 are limiting gains. The EUR/USD technicals are bullish above 1.0870, which is where the uptrend line from the middle of February comes into play. A break below that level targets 1.0800.

GBP/USD drifted lower in a 1.2730-1.2758 range. The US data kept traders on the defensive. The UK public expectations for inflation fell to 3.0% from 3.3% last November, which is good news for those hoping for BoE rate cuts, although a rate cut is not on the agenda for next week’s monetary policy meeting. UK workers at the Office for National Statistics are outraged that the government expects them to show up to the office two days a week and are threatening to strike. The news is further evidence for why all government unions should be abolished or at least lose the right to strike.

USD/JPY took off like a scared cat yesterday, soaring to 148.36 from 147.44, then extending the gains in a 148.03-148.84 range overnight. Yesterday’s US data convinced traders that the Fed may be less dovish, which lifted the US 10-year Treasury yield to 4.30% from 4.19%. The outlook for a dovish Fed overshadowed news that Japan’s negotiated wages were 5.3%, the highest increase in 30 years, which supports a BoJ rate hike next week.

AUD/USD retreated in a 0.6552-0.6585 range with prices weighed down by US dollar demand. Traders expect that the RBA will leave rates unchanged at 4.35% on Tuesday and keep them at that level until September.

NZD/USD traded in a 0.6090-0.6133 range despite improving BNZ PMI data in February (Actual 49.3 vs 47.5 in January). BNZ Head of Research Stephen Tolis said, “New Zealand’s manufacturing sector is still in recession, but this month’s PMI indicates there is light at the end of the tunnel.”

USD/MXN traded in a 16.6989-16.7480 range. Prices traded higher after more robust than expected US inflation data on Thursday sparked broad-based US dollar demand. Some analysts expect that Banxico will trim its benchmark rate by 25% next week.

Michigan Consumer Sentiment is expected to be unchanged at 76.9.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0975 vs (prev. 7.0974}.

Shanghai Shenzhen CSI 300 rose 0.22% to 3569.99.

PBoC left 1-year medium term-lending facility (MLF) unchanged at 2.5%.

February House Price Index falls 1.4% (January -0.7%). China’s falling house prices are keep prospective buyers on the sidelines and exacerbating the developer crisis.

Source: Bloomberg

Chart: USDCNY and USDCNH daily

Source: Investing.com