January 9, 2024

- Wall Street poised to open lower.

- US and Canadian trade data close to as expected.

- US dollar opens mixed from Monday but bid in early NY trading.

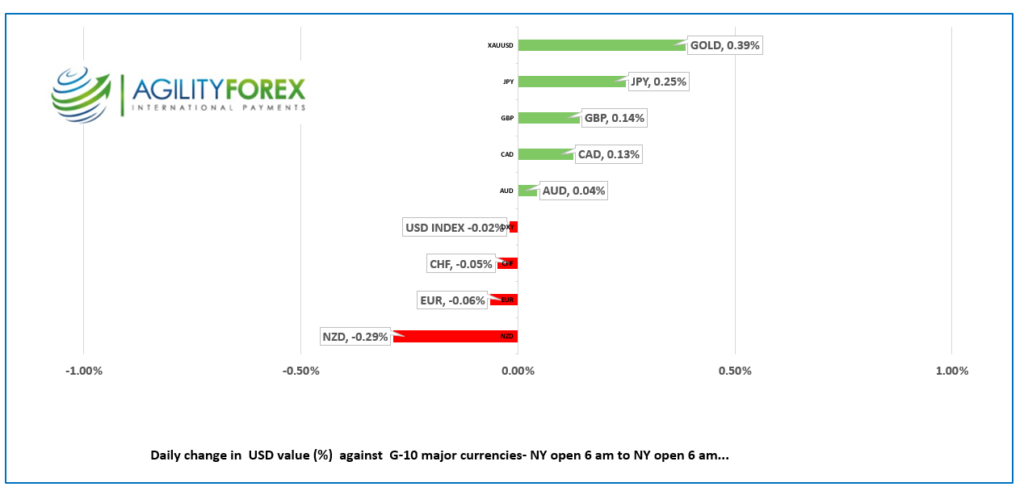

FX at a glance

Source: IFXA

USDCAD Snapshot: open 1.3365-69, overnight range 1.3341-1.3376, close 1.3348.

USD/CAD is at the top of its overnight session range due to broad US dollar demand against the G-10 majors, but it is still inside yesterday’s 1.3345-1.3405 range. For the most part, the price action is just noise as traders await economic insight from the release of US inflation data on Thursday. USD/CAD got a little support from the rise in the US 10-year yield from 4.01% to 4.04% overnight.

USD/CAD is not feeling any pressure even though Friday’s Canadian employment data suggested that the BoC would delay cutting rates until the summer at the earliest.

Oil prices continue to churn inside a $70.00/b – $74.00/b band as slowing global demand competes with OPEC production cuts for dominance.

Canada building permits fall 3.9% m/m in November. Canada’s merchandise trade surplus with the world narrowed from $3.2 billion in October to $1.6 billion in November.

USDCAD Technicals:

The intraday USDCAD technicals are bullish above 1.3340, looking for a break above 1.3405 to extend gains to the 1.3440-1.3450 resistance area. A break below 1.3340 targets 1.3305 then 1.3250.

USDCAD dropped steadily after peaking at 1.3895 on November 1, until it found a bottom at 1.3195 at the end of December. The subsequent rally has been underwhelming and unless 1.3450 breaks, it is just a correction and suggests another test of 1.3195 is likely.

For today, USDCAD support is at 1.3340 and 1.3310. Resistance is at 1.3410 and 1.3440. Todays range 1.3330-1.3430.

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

Markets are noisy but directionless as traders bide their time until the release of US inflation data on Thursday. Traders appear inured to dire news about the wars in Gaza, Ukraine, and Africa, and are equally bored with China’s imperialism and the latest Trump saga.

Boeing provided equity traders with a bit of entertainment after new problems with its 737 Max 9 aircraft came to light over the weekend. An Alaska Air 737 rained parts over Portland, Oregon, leading to the FAA grounding the plane (again) and BA: NYSE falling 8.0% on Monday.

Japanese equity traders returned from vacation and lifted the Nikkei 1.16% to 33,763.18, a level last seen in 1990. Australia’s ASX climbed 0.92%. The positive sentiment did not carry over into Europe as the major bourses are in negative territory, led by a 0.32% drop in the German DAX. S&P 500 futures are down 0.37%.

EUR/USD rallied in Asia, reaching 1.0966, then dropped in Europe until it found a short-term bottom at 1.0930. Sellers emerged after another weak German industrial output report, which fell for the sixth month in a row (actual 0.7% m/m, forecast 0.2%). Eurozone unemployment dropped to 6.4% in November, a new low, which suggests the ECB may not be too quick to cut interest rates due to the risk of wage inflation.

GBP/USD bounced in a 1.2722-1.2765 range. The currency is underpinned by EUR/GBP selling pressures as some analysts believe that the BoE is more hawkish than the ECB. More importantly, traders are not motivated as they await the US inflation data due Thursday.

USD/JPY traded erratically. Prices dropped from 144.32 to 143.43 in Asia following soft Tokyo inflation data (actual Dec. CPI 2.4%, vs 2.7% y/y in Nov.), then bounced to 143.90 with the rise in the US 10-year Treasury yield to 4.04% from 4.01%.

AUD/USD traded in a 0.6695-0.6734 range overnight, supported by better than expected Retail Sales and Building Permits data. However, the gains eroded, and AUD/USD is trading at 0.6704 in early NY.

US Trade deficit narrowed to -$63.2 billion from -$64.5 b.

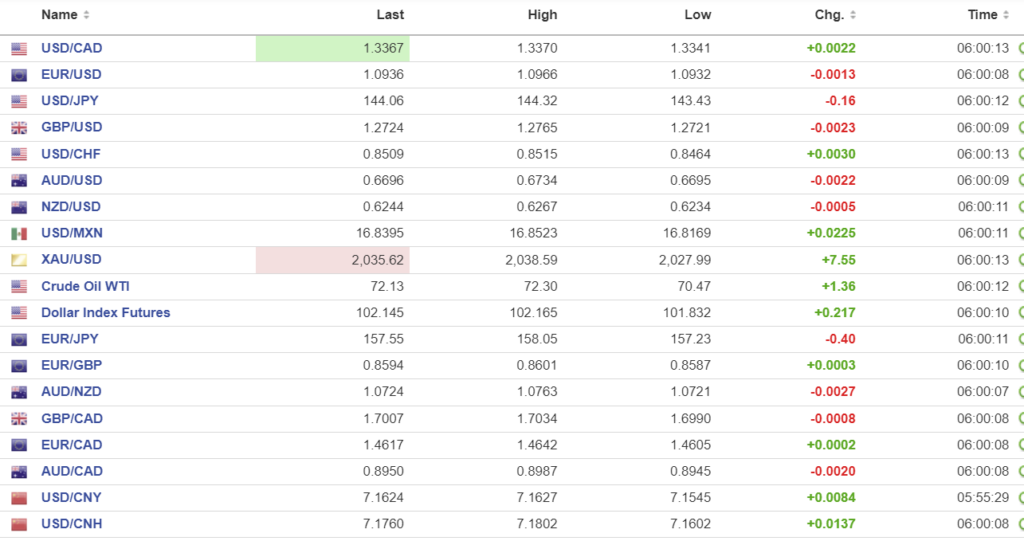

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1010, expected 7.1502, previous 7.1006

Shanghai Shenzhen CSI 300 rose 0.20% to 3292.50.

PBoC official says the bank will use a variety of tools to provide strong support for reasonable growth in credit. Analysts suggest the comments are hinting at a Reserve Requirement Ratio (RRR) cut in the near future.

A Bloomberg article warns that if Xi Jinping’s aspirations for Taiwan lead to an invasion, it would cost the global economy $10 trillion. The Taiwan election is January 13.

Chart: USDCNY and USDCNH hourly from Dec. 21

Source: Investing.com