Image by DALL-E

November 24, 2023

- German IFO below forecasts.

- UK Consumer confidence improves but still in negative territory.

- US dollar is uninspired at the open

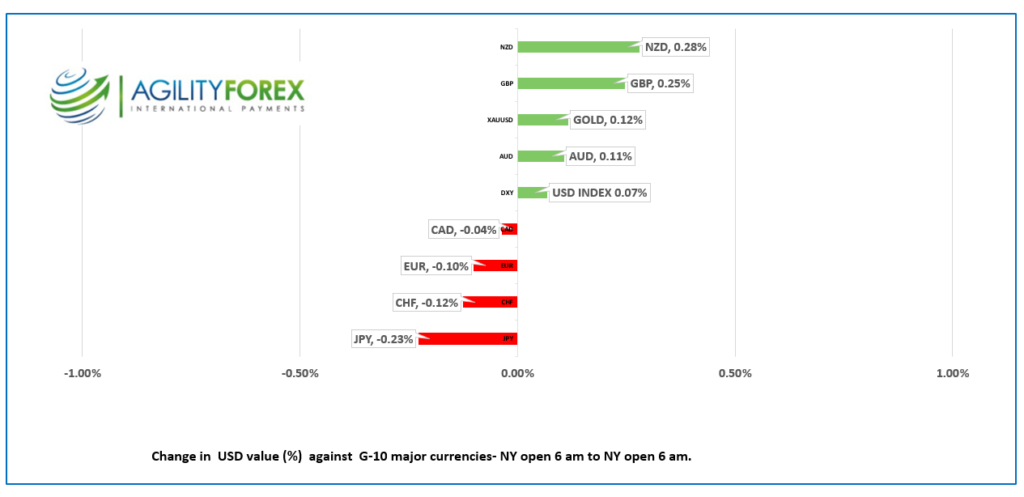

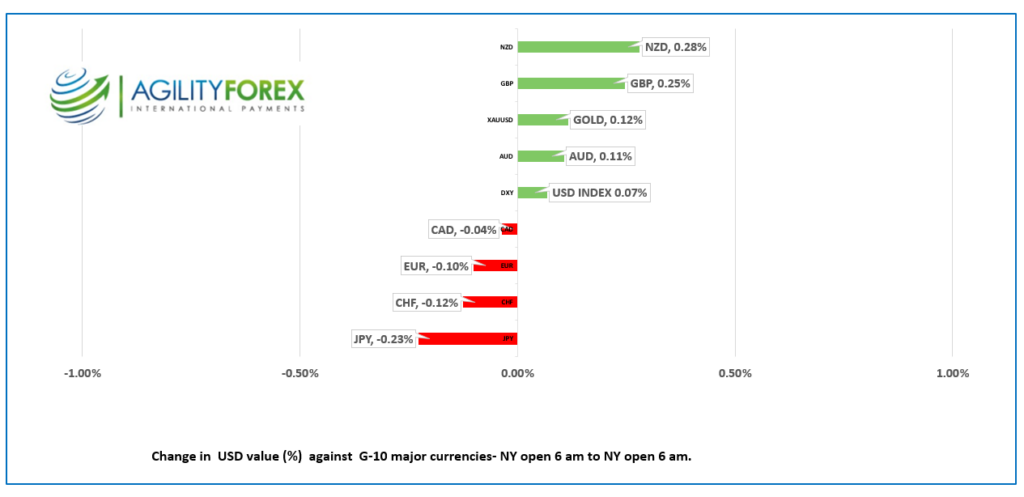

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3687-91, overnight range 1.3654-1.3712, close 1.3692

USDCAD drifted aimlessly yesterday and again overnight, with the currency unable to gain any traction due to the absence of the US market. That changed after Canadian September Retail Sales rose 0.6% m/m, far faster than expected and USDCAD dropped to 1.3663. It’s a knee jerk reaction and unlikely to last because the gains were due to auto sales. Car manufacturers and dealers tend to offer hefty discounts in the September/October period as they make room for the new models.

Core Retail Sales, which excludes, autos and fuel, fell 0.3%m/m. Consumers are obviously feeling the pain of high taxes and high interest rates as sales at supermarkets and other grocery retailers, fell 0.9%. beverages. Same money-don’t eat.

The left-wing coalition governing Canada (Liberal-NDP) attempted to deflect outrage from the inflationary impact of their tax and spend policies over high grocery prices inflationary policies to food retailers. The government suggested a host of reasons for rising food costs, while saying that the “big five” grocery store chains were to blame. To that end, they enacted Bill C-56, the Affordable Housing and Groceries Act, described by the Finance Minister as an effort “to support Canadians with the cost of living.”

Galen Weston Jr. and colleagues have been known to fix the odd price or two, so they deserve some blame. However, the federal government should get the lion’s share.

A self-described low mileage trucker, hauling loads locally, broke down his fuel bill for one month: Diesel $3402.86 + Fed Tax $118.56 + Prov. Tax $223.46 + Carbon tax $462.69 + HST (which is charged after all the other taxes are levied) $548.31. The total bill was $4765.88, and 40% is taxes. Those taxes are passed on to consumers. The solution is simple.

Those high taxes may be reflected in today’s Retail Sales data for September. Retail Sales, ex-autos, are expected to have fallen by 0.2% m/m (August 0.1%), mainly because consumers are giving more of their money to the government. You can see the results in the retail sales data.

WTI oil prices danced in a $76.18-76.79/b range due to caution ahead of the OPEC meeting at the end of the month. There are a lot of rumors about new production cuts being announced for January 2024

USDCAD Technicals:

The intraday USDCAD are bearish, like yesterday. The intraday downtrend is intact while prices are below 1.3720 and looking for a break of support in the 1.3630-50 zone. If successful, USDCAD would test 1.3560. A break above 1.3720 suggests further 1.3660-1.3760 consolidation.

Longer term, the monthly chart shows a bullish bias from May 2021 with prices consolidating gains from 1.2020 in a 1.3100-1.4000 range. The fact that USDCAD is close to the top of the band offers some scope for further losses.

For today, USDCAD support at 1.3650 and 1.3630. Resistance is at 1.3720 and 1.3760. Today’s range 1.3640-1.3720

Chart: USDCAD weekly

Source: Daily FX

G-10 FX recap

FX markets traded quietly overnight as the loss of the US market on Thursday and an unofficial holiday today derailed price action continuity. Markets could react to today’s S&P Global Manufacturing PMI (forecast 49.8 vs. Oct. 50) and Services PMI (forecast 50.4 vs. 50.9 in October), but the ISM report (released December 1) carries more weight with traders.

Asian equity indexes closed higher with Japan’s Nikkei 225 index up 0.52%. European bourses are posting small gains led by a 0.19% rise in the French CAC-40 index. S&P 500 futures are barely positive, which, if they turn negative and drop, suggests early morning US dollar sellers will become late morning US dollar buyers.

EURUSD chopped about in a 1.0895-1.0920 range with somewhat disappointing German data not having much impact on prices. Germany’s GDP fell 0.4% y/y, slightly underperforming against a forecasted 0.3% decrease. Additionally, the German IFO Business Climate Index, along with data on Current Assessment and Expectations, showed results that were marginally below expectations but showed a slight improvement compared to October’s figures. ING economists suggest the Ifo data means the German economy may be bottoming out, but it doesn’t suggest a recovery.

GBPUSD is at the top of its 1.2524-1.2580 range. The currency pair is benefitting from a bit of optimism that started with the recent tax cut announcements and stronger than expected PMI data yesterday and higher than forecast Consumer confidence today.

USDJPY rose from 149.19 to 149.72, partly due to the higher 10-year Treasury yield which climbed to 4.65% from 4.416% at Wednesday’s NY close.

AUDUSD was uninspired and traded in a 0.6550-0.6579 range. The currency has a bit of a bid from recent comments by RBA Governor Michel Bullock who suggested another rate hike was possible.

FX high, low, open (as of 6:28 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1151, expected 7.1440, previous 7.1212.

Shanghai Shenzhen CSI 300 rose 0.40% to 3561.52.

The WHO appears concerned about a surge in respiratory illnesses in Northern China. Chinese authorities claim there is no detection of unusual or novel pathogens or unusual clinical presentation, which sounds rather similar to what they said about COVID around this time in 2019.

Chart: USDCNY (onshore) vs USDCNH (offshore)

Source: Investing.com