Photo:Pixabay

May 15, 2023

- Turkish elections undecided

- G-7 to take veiled shots at China on Friday

- US dollar retreats overnight but opens higher compared to Friday.

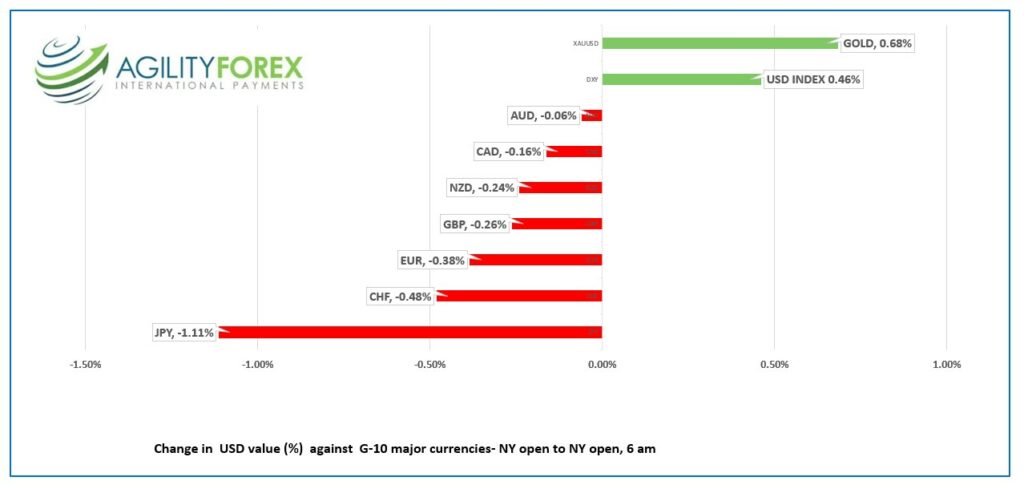

FX at a glance

Source: IFXA Ltd/RP

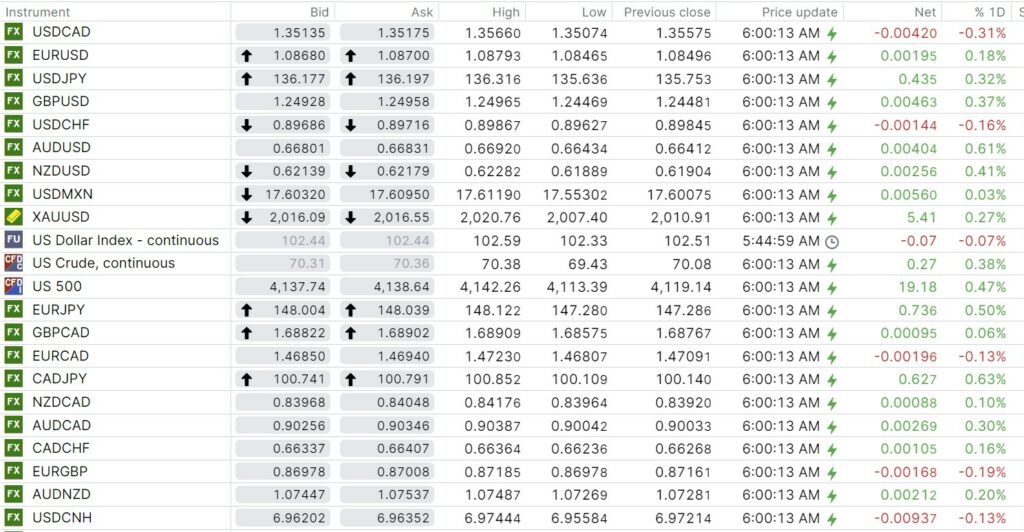

USDCAD Snapshot: open 1.3514-18, overnight range 1.3498-1.3566, close 1.3558

USDCAD may uncouple from the US dollar train this week, albeit briefly, thanks to the release of key economic data and the soothing musings of Bank of Canada Governor Tiff Macklem.

Canada’s April inflation data is released Tuesday. Headline CPI is expected to fall to 4.1% from 4.3% y/y while the more important Core CPI drops to 3.9% from 4.3%. Hotter than expected readings will cause speculation that the BoC will be forced off the fence and raise interest rates.

Economists are hoping that Governor Macklem will provide monetary policy insight during his Financial System Review press conference on Thursday.

Retail Sales are Friday along with the kick-off to the Victoria Day long weekend.

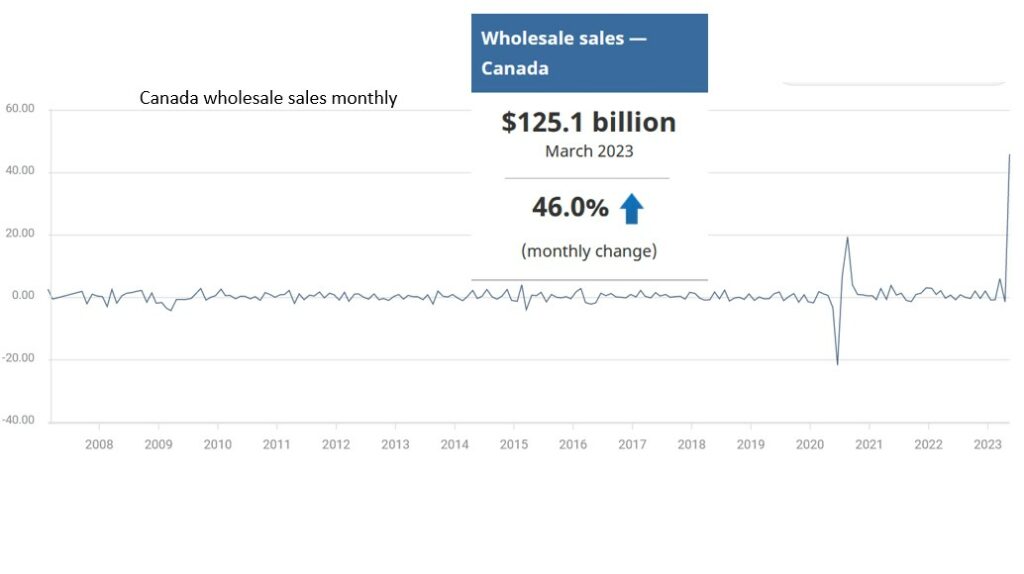

Canada Wholesale Sales rise 46% m/m (forecast -0.4%) which suggests something is dodgy with the data

Source: FXS/StatsCanada

USDCAD Technical Outlook

The latest USDCAD rally stalled at 1.3570, ahead of the March downtrend line which comes into play at 1.3600. USDCAD is trading with an intraday bearish bias below 1.3520, looking for a break below 1.3470 to extend losses to 1.3420.

The USDCAD failure to even test the March downtrend even as WTI prices are trading defensively suggests further 1.3300-1.3600 price action for this week.

For today, USDCAD support is at 1.3470 and 1.3430. Resistance is at 1.3520 and 1.3560

Today’s range 1.3450-1.3530

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The Turkish election has not resulted in a clear winner leading to a run-off vote on May 28. The result will leave Turkey with a similar landscape to the US; half the country supports the president while the other half hates him.

The lack of top tier, actionable US data and the next FOMC meeting still being a month away has traders (and the media) focused on the US debt ceiling talks.

Fed Vice Chair Philip Jefferson (voter) did not sound overly enthusiastic about pausing rate hikes. He said that inflation was too high and said that little recent progress in core inflation is “bad news.”

The G-7 meet on Friday and are supposedly going to discuss China’s coercive trade practice, but they are too afraid of Beijing’s wrath to actually mention China by name.

Chicago Fed President Austan Goolsbee eased fears for a June rate hike when he said the Fed needs to monitor more than the usual data sets as it assesses how banking stresses impact GDP.

EURUSD is steady in a 1.0847-1.0879 range with price action tracking US debt discussion headlines. Eurozone Industrial Production was not a factor (actual -4.1% m/m in March forecast -2.5% m/m)

GBPUSD is rebounding from Friday’s low rising from 1.2447 to 1.2510 in NY trading. GBPUSD gains may be capped by concerns that the UK economy underperforms that of the EU.

USDJPY is consolidating Friday’s gains in a 135.64 to 136.32 band, underpinned in part by non-stop dovish comments from BoJ Governor Kazuo Ueda. Japan’s PPI index rose 5.6% y/y In April, compared to the consensus forecast of 6.0%.

AUDUSD rallied in a 0.6642-0.6692 band. Prices were underpinned by a hawkish interest rate outlook from National Australia Bank (NAB). Economist’s changed their RBA on hold forecast to RBA will hike in July and again before year end.

NZDUSD mirrored Aussie moves and rose in a 0.6190-0.6228 band. The RBNZ is expected to hike rates by 25 bps on May 24.

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

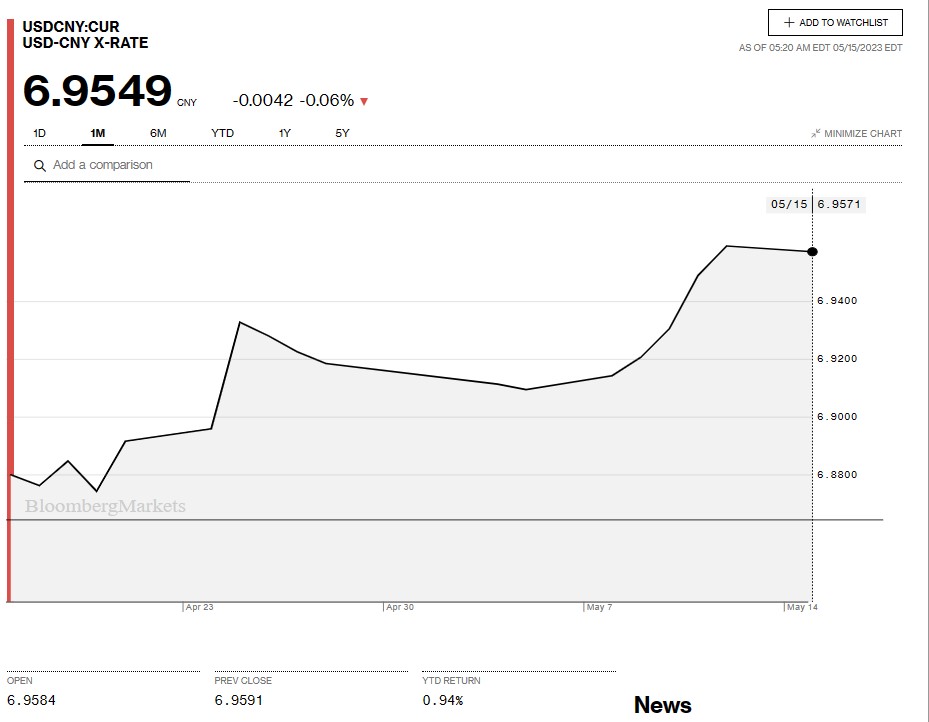

China Snapshot

Bank of China Fix: 6.9654 previous 6.9481.

Shanghai Shenzhen CSI 300 rose 1.55% to 3995.89.

Chart: USDCNY 1 month

Source: Bloomberg