Image by DALL-E

December 15, 2023

- Traders dismiss hawkish comments from ECB and BoE officials.

- US 10-year Treasury yield ticks lower

- US dollar continues to slide-GBP outperforms.

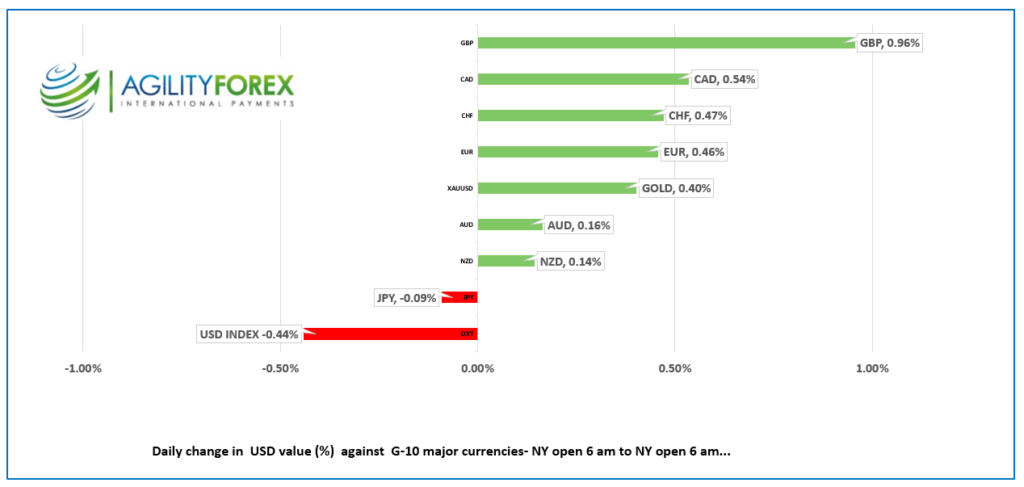

FX at a glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3378-82, overnight range 1.3372-1.3415, close 1.3409

USDCAD is under pressure but above its overnight session low due to broad-based US dollar weakness and firmer commodity prices.

Bank of Canada Governor Tiff Macklem is Christmas shopping in Toronto today. He is taking time out of his trip to speak before the Canadian Club at the Royal York Hotel, and the text of his remarks is available at 12:25 pm ET.

His words should have as much effect on USDCAD as remarks from Bank of England Governor Andrew Bailey had on GBPUSD, or even ECB President Christine Lagarde’s comments yesterday. That’s because it is the outlook for US interest rates that is moving markets. The other central bankers are just a sideshow.

USDCAD Technicals:

The intraday USDCAD technicals are bearish following the move below 1.3540 on Wednesday. The intraday down channel guiding prices lower is intact between 1.3410 and 1.3320. A break above 1.3420 suggest a retest of resistance in the 1.3440-60 area.

Longer term, the USDCAD down trend from the middle of November is intact while prices are below 1.3610 and looking for a move below the 1.3340-60 area to extend losses to 1.3200.

For today, USDCAD support at 1.3360 and 1.3340. Resistance is at 1.3420 and 1.3460. Today’s range 1.3360-1.3440.

Chart: USDCAD daily

Source: Daily FX\

G-10 FX recap

The fallout from the final Fed meeting of 2023 is still reverberating through financial markets. The US dollar is under pressure, commodity prices are higher, and the US 10-year Treasury yield inched higher to 3.95%.

Fed Chair Jerome Powell half-heartedly pushed back against interest rate cuts, repeating, ‘We are prepared to tighten policy further, if appropriate.’ No one believed him, including the FOMC committee members who penciled in 75 bps of rate cuts in 2024. Traders took note and said, ‘I see your 75 and raise you another 75.’ The CME Fedwatch tool expects 150 bps of rate cuts by next December.

Asian equity indexes closed higher, and even Japan’s Nikkei 225 managed to gain 0.87% despite the firm yen. European bourses are trading mixed. The UK FTSE 100 and Spanish IBEX 35 indices are negative, while the others are in the green. S&P 500 futures are up 0.18%.

The Empire State Manufacturing index fell to -14.5 from 9.1 in November which allowed the US dollar to scrape back some losses.

EURUSD traded in a 1.0947-1.1004 range overnight. The gains above 1.1000 were not sustained, partly because of ECB President Christine Lagarde’s press conference comments when she insisted that policymakers did not discuss rate cuts during the meeting. Nevertheless, UBS analysts are predicting the first rate cut will occur in April. Weaker than expected Eurozone Manufacturing and Services PMI data also weighed on prices.

GBPUSD remains bid and is trading at the top of its 1.2740-1.2790 overnight range. The Bank of England left rates unchanged at 5.25% in a hawkish statement that warned of inflation risks necessitating high rates. BoE Governor Andrew Bailey said, ‘So my view at the moment is, it’s really too early to start speculating about cutting interest rates. We’ve got to see more progress.’ Traders continue to expect a rate cut in the spring of 2024. Weaker than expected UK Manufacturing PMI was offset by an increase in Service PMI.

USDJPY is consolidating this week’s losses in a 141.47-142.47 range. Prices continue to be pressured by the outlook for US interest rates and expected BoJ tightening.

AUDUSD traded sideways in a 0.6694-0.6726 range. The currency did not get any help from December PMI data. Services PMI ticked up to 47.6 from 46.0, while Manufacturing PMI dipped to 46.0 from 47.2. Judo Bank Chief Economist Warren Hogan said, ‘The December Flash PMI report showed some minor improvements in business activity heading into the end of the year but confirms that the economy remains on a soft-landing trajectory.’

Today’s US data includes S&P Global PMI data, Industrial Production, and Capacity Utilization, are on tap.

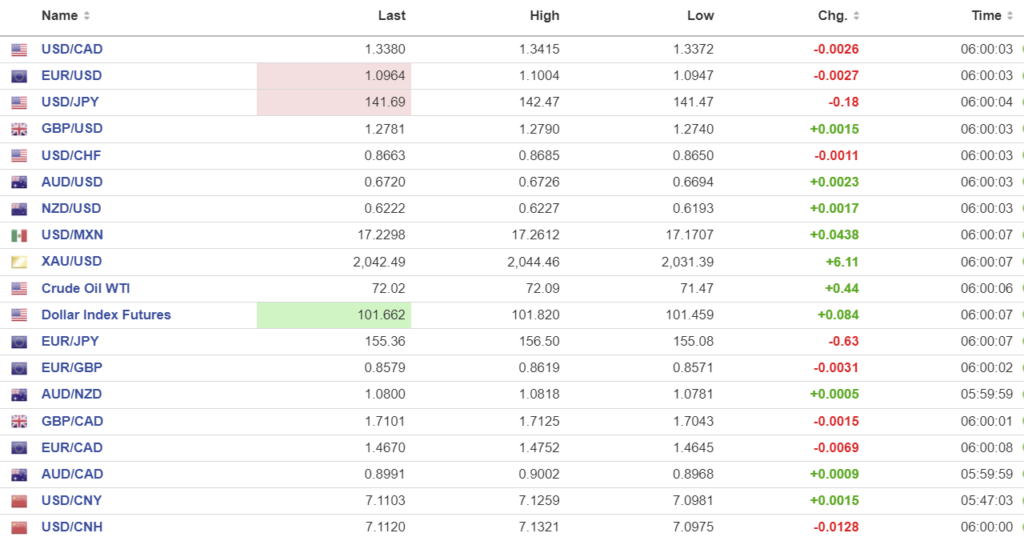

FX high, low, open (as of 6:28 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.0957, expected 7.1132, previous 7.1090.

Shanghai Shenzhen CSI 300 fell 0.31% to 3341.55.

China stocks dip after Fixed Asset Investment data rose just 2.9%. The reported 6.6% y/y rise in Industrial Production is considered a dodgy number due to its comparison to last year’s data which was impacted by Covid lockdowns.

China’s youth unemployment data was not available because authorities do not want outsiders to know how badly Xi Jinping is managing the economy.

Bloomberg reports that the PBoC pumped a “record $112.0 billion of one-year loan cash to allay concerns over cash scarcity amid a surge in government debt issuance.”

Chart: USDCNY and USDCNH

Source: Investing.com