Picture: Matt Groening

- Bank of Canada hiked 50 bps-suggests it could be the last

- Putin injects nukes into the conversation, again.

- US dollar modestly lower from Wednesday, but higher than where it closed

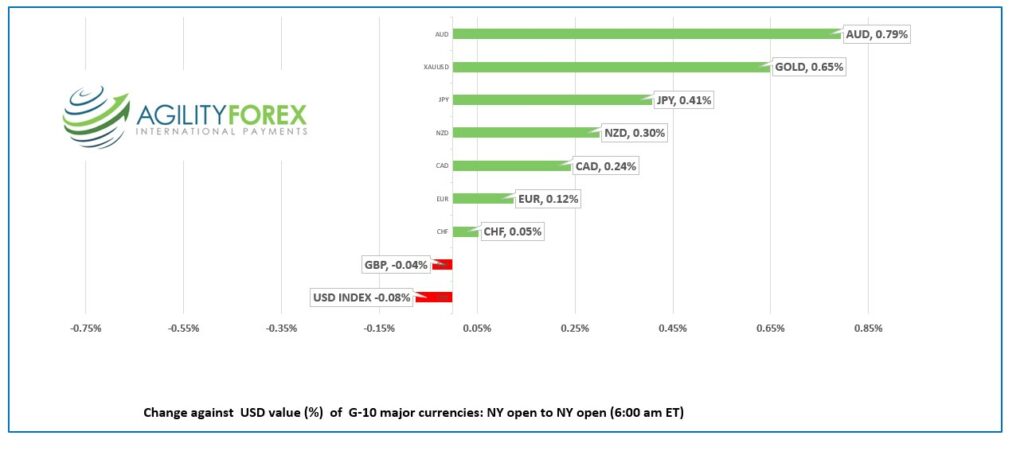

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3651-55, overnight range 1.3574-1.3687, close 1.3653

The Bank of Canada hiked its benchmark rate by 50 bps yesterday then warned that it may be the last rate increase of this cycle. Traders sold USDCAD on the headline driving prices from 1.3650 to 1.3588, then bought dollars when they read the last line in the statement

The USDCAD rally also got some help from poor risk sentiment and wobbly US equity markets.

Traders are hoping for some more insight about the BoC’s outlook for Canadian rates from Deputy Governor Sharon Kozicki this afternoon around 2:00 pm.

Governor Tiff Macklem is having a fireside chat with the Business Council of BC on Monday and that may be more interesting. That’s because Mr Macklem’s (BoC) has demonstrated a poor understanding of what “forward guidance” means. Many times, this year, the Bank’s actions were markedly different from pre-meeting communication. It wouldn’t be much of a surprise if his speech is hawkish.

WTI consolidated yesterday’s losses in a $72.28/barrel-$73.23 range. Prices are depressed due to US recession concerns but vulnerable to a sharp spike higher on news that China is ending its Covid-zero policies. Trading is distorted due to thin markets ahead of the Fed and Christmas.

The Canadian data calendar is empty.

USDCAD technical outlook.

The USDCAD intraday technicals turned bearish with the move below the bottom of the 1.3640- 1.3740 uptrend channels setting the stage for a retest of 1.3550.

Longer term, USDCAD is overbought according to RSI studies and approaching Bollinger band resistance at 1.3730. A decisive break below 1.3600 suggests further losses to 1.3420.

For today, USDCAD support is at 1.3560 and 1.3510. Resistance is at 1.3640 and 1.3690

Today’s range 1.3550-1.3640

Chart: USDCAD daily with Bollinger bands and RSI

Source: Saxo Bank

G-10 FX recap and outlook

Financial markets are directionless in a low-volume, poor liquidity environment as traders bide their time until next week’s US inflation data, and policy meetings from the FOMC and ECB.

Russian President Vladimir Putin is maintaining the farce that he is a brilliant wartime leader and that he expected the Russian invasion of Ukraine to be protracted and “take a while.”

He also warned that “As for the idea that Russia wouldn’t use such weapons first under any circumstances, then it means we wouldn’t be able to be the second to use them either – because the possibility to do so in case of an attack on our territory would be very limited.”

Asian equity markets closed with small losses except Hong Kong’s Hang Seng which rallied 3.38% on rumour that covid restrictions would be eased further. European bourses are in negative territory while S&P 500 futures gained 0.30%. The US 10-year Treasury yield is 3.442%.

US weekly jobless claims were 230,000 as expected and therefore the data was ignored.

EURUSD traded in a 1.0491-1.0530 range. The single currency is underpinned by speculation the ECB will raise rates by 75 bps next week, following hawkish comments by policymakers recently. Traders are looking ahead to the Wall Street open for direction.

GBPUSD is near the bottom of its 1.2156-1.2213 range. The government has decided the solution to its energy woes is below ground. Policymakers approved the UK’s first new coal mine in 30 years, which should vastly improve job opportunities for the ten-year old cohort.

Source: History Crunch

USDJPY traded in a 136.26-137.24 range. Japan’s Q3 GDP shrank 0.2% q/q, a tick better than expected, and fell 0.8% y/y (forecast -1.1%). Soft US treasury yields are also weighing on prices.

AUDUSD traded narrowly in a 0.6700-0.6737 range supported by hopes China eases covid restrictions faster, but gains were limited by soft commodity prices. Australia’s trade surplus was 12.217 billion in October, which was far better than the 1.115 expected.

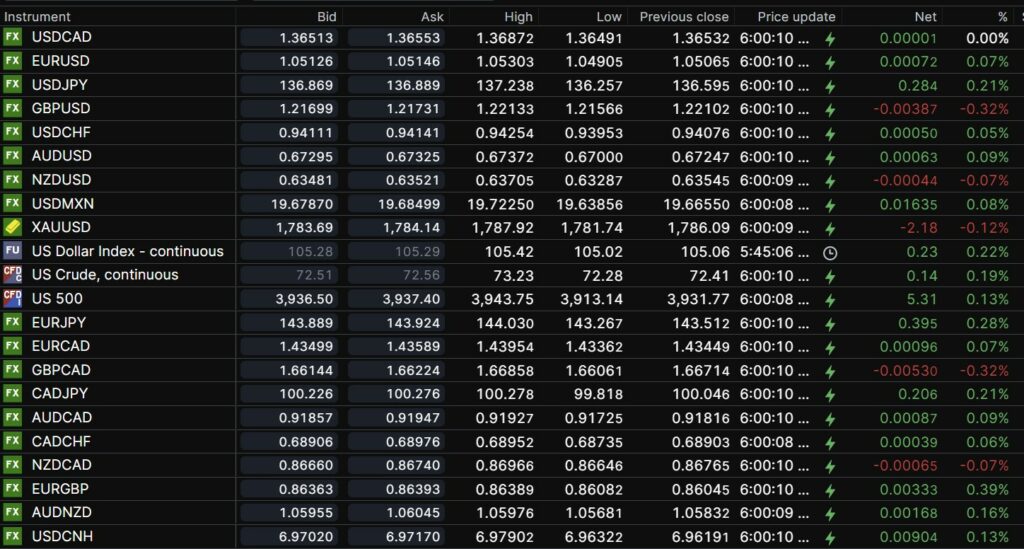

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

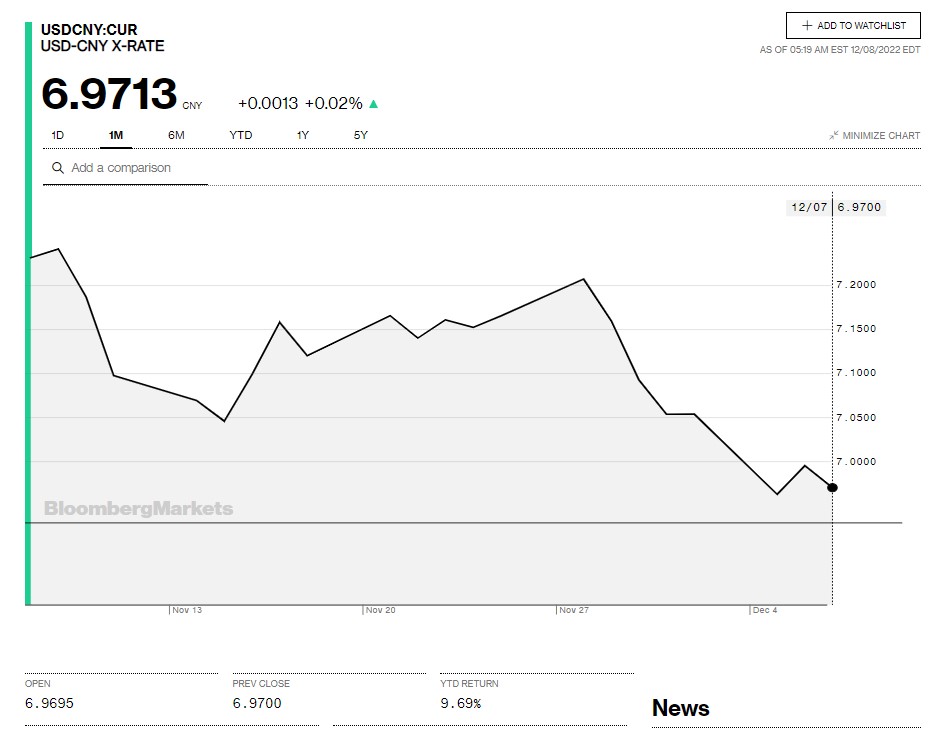

China Snapshot

Today’s Bank of China Fix: 6.9606, previous 6.9975

Shanghai Shenzhen CSI 300 rose 0.02% to 3959.18

Chart: USDCNY 1 month

Source: Bloomberg