- Canada CPI rises 4.8% y/y in December (November 4.7%)

- UK PM Johnson’s job at risk

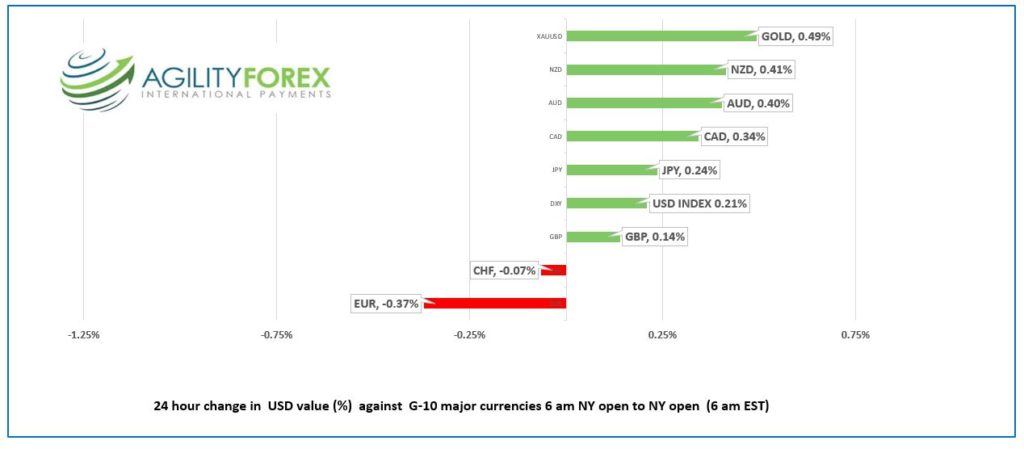

- Commodity currency bloc outperforms

FX at a Glance

Source: IFXA Ltd/RP

USDCAD Snapshot: Open 1.2470-74, Overnight Range-1.2452-1.2573, previous close 1.2512

Surfs up and the Canadian dollar caught a wave. Yesterday, USDCAD tracked the S&P 500 index, which was taking its lead from US 10-year Treasury yields. The 1.89% drop in the index that coincided with yields topping out at 1.897%, lifted USDCAD to 1.2560. In the afternoon, USDCAD reasserted its petro-currency status dropped to 1.2512 at the close. The pattern was repeated in Asia and Europe with USDCAD peaking at 1.2523 then dropping to 1.2472 as NY opened.

The sell-off continued after news Canada CPI rose 4.8% y/y in December, a tick higher than the 4.7% gain seen in November.

Stats Canada wrote: “Canadians continued to feel the impact of rising prices for groceries in December, as unfavourable weather conditions during the growing season and supply chain disruptions put upward pressure on prices. Supply chain disruptions also led to higher prices for durable goods, including passenger vehicles and household appliances, while higher construction costs and the increased frequency and severity of weather events contributed to rising home and mortgage insurance costs.

USDCAD crashed through the overnight low of 1.2472 and dropped to 1.2452. The move quickly reversed, in part because December CPI fell 0.1% m/m, even though the drop was due to lower gas prices due to new Omicron restrictions.

WTI oil surged 26% surge in WTI since December 2, and forecasts for further gains to $125.00/b, suggest further oil upside. However, the steep rally suggests oil is “overbought” and will consolidate.

The Opec Monthly Oil Report is expected to lower its H1 oil surplus forecast when it is released today

USDCAD has further downside. Monday’s BoC Business Outlook Survey conclusions raised the odds for a rate hike at next week’s monetary policy meeting, and today’s higher than expected Canadian CPI reading, confirms it.

Technical view: The USDCAD technicals are bearish below 1.2590, a level guarded by resistance at 1.2560 and by the 200-day moving average at 1.2498. A break below 1.2440 suggests further losses to 1.2310. Only a move above 1.2600 will negate the downside pressure.

For today, USDCAD support is at 1.2440 and 1.2410. Resistance is at 1.2530 and 1.2570. Today’s Range 1.2480-1.2530

Chart USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Equity traders finally acknowledged what other markets already expected: US rates are going higher, sooner, and faster than expected.

The US 10-year Treasury yield is trading at 1.883% in NY, and the 2-year yield touched 1.059% as traders expect the Fed to hike rates four times in 2022. No one expects the FOMC to raise rates on January 26, but why not?

It’s not like inflation will collapse in two months.

Asia equity markets followed Wall Street lower, with the Nikkei shedding 2.8%, and Australia’s ASX down 1.0%. European bourses recovered from a soft open and are green across the board. S&P 500 and DJIA futures are modestly higher, as are gold and oil.

EURUSD is at the top of its 1.1320-1.1350 overnight range. German HICP was 5.7% which helped underpin prices. Traders and economists appear to have a different view for the timing of an ECB rate hike. Traders expect a 10 bp rate increase at the October 27 ECB meeting, while economists surveyed by Reuters do not expect a rate increase until the first half of 2023 at the earliest.

Regardless, the divergent Fed and ECB outlooks argue for a lower EURUSD. A break of support at 1.1310 targets 1.1250.

GBPUSD bounced from the Asia low of 1.3590 to reach 1.3643 before inching back to 1.3626 in NY.

UK inflation reports were higher than expected. CPI rose 5.4% y/y in December compared to the forecast of 5.2% y/y. The news raises the odds for a BoE rate hike at the February meeting. UK political drama may limit gains, especially if Prime Minister Boris Johnson is ousted by MP’s unhappy with his COVID-19 partying antics.

USDJPY chopped in a 114.22-114.78 range supported by firmer Treasury yields. However, widespread US dollar weakness, and new COVID-19 restrictions in Tokyo capped gains.

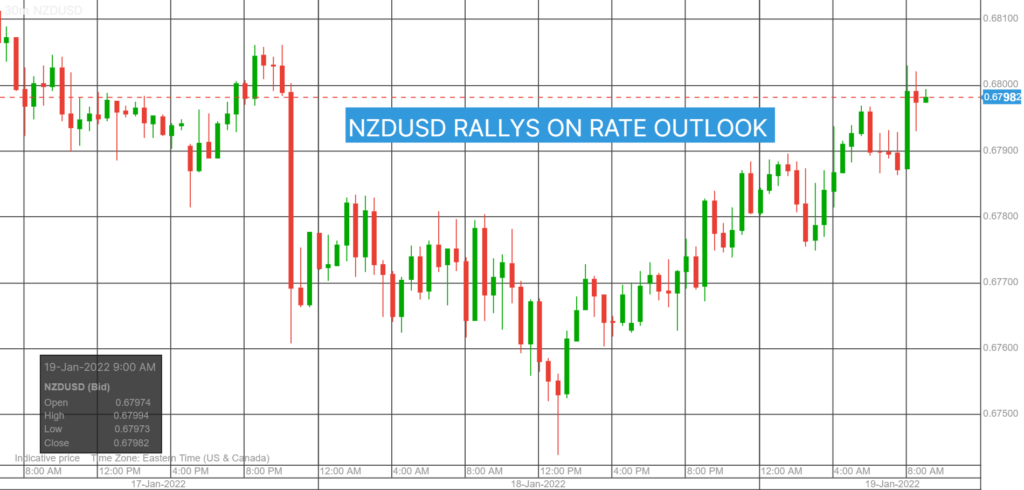

AUDUSD and NZDUSD rallied alongside rising commodity prices. ANZ Bank predicted that the RBNZ would raise rates to 3.0% by April 2023, which gave NZDUSD a boost.

US Building Permits rose 1.4% m/m in December while Building Permits rose 9.1%.

Chart of the Day: NZDUSD

Source: Saxo Bank

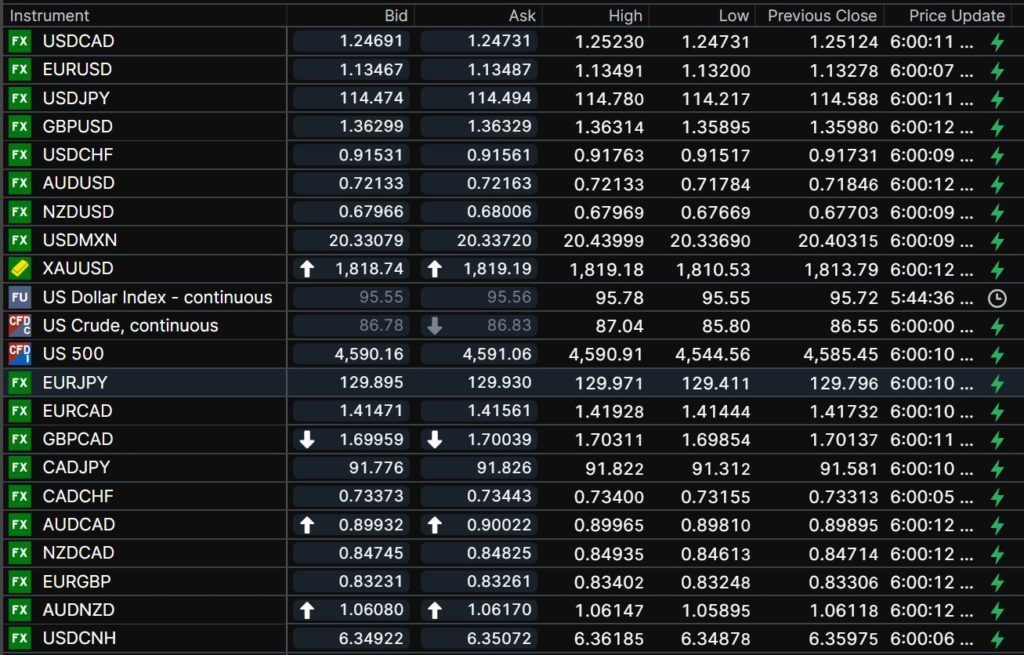

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

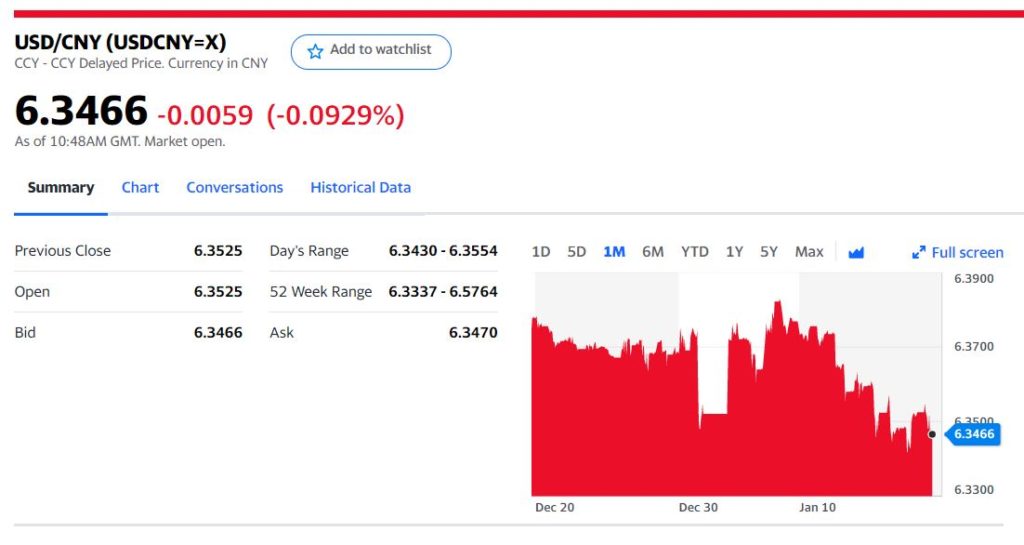

China Snapshot

Today’s Bank of China Fix 6.3624, previous 6.3521

Shanghai Shenzhen CSI 300 fell 0.69% to 4,780.38

Upside from expectations of further easing by PBoC offset by rumours that officials are planning more regulations on tech firms

Chart: USDCNY 1 month