Source: HDClipart.com

- Japanese yen sewers as traders taunt Bank of Japan

- BoC rate hike today-75 or 100 bps, it’s a coin flip

- US dollar rallies again JPY underperforms.

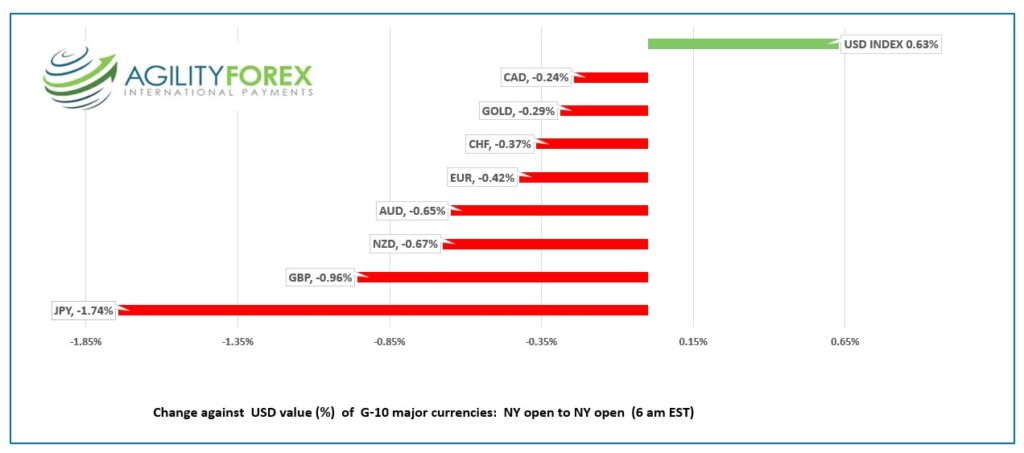

FX at a glance:

Source: IFXA Ltd/RP

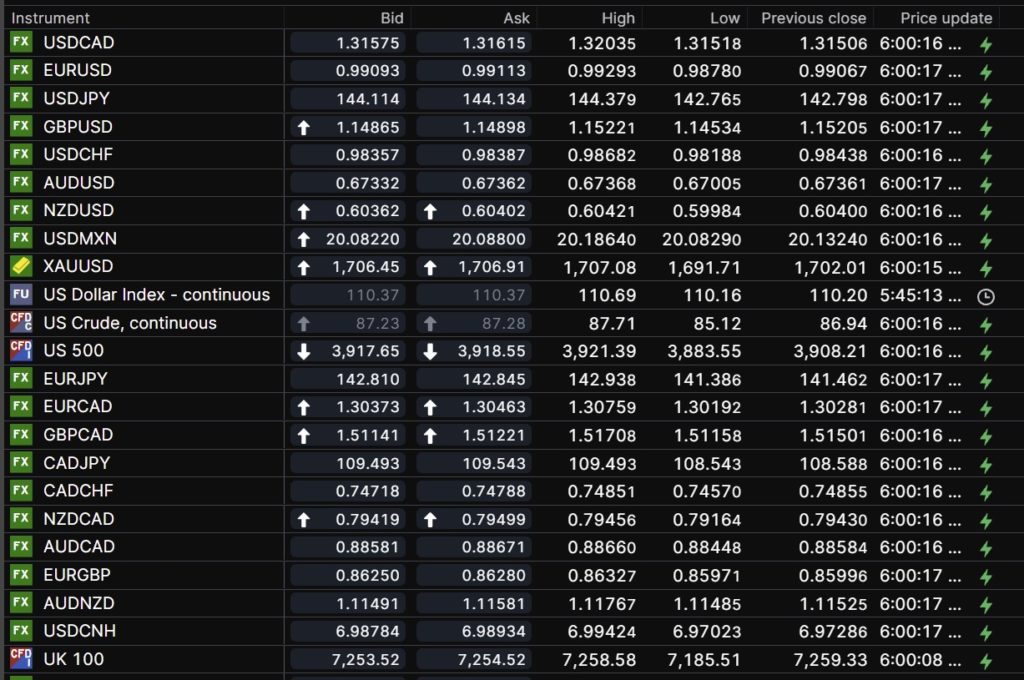

USDCAD Snapshot: open 1.3158-62, overnight range 1.3152-1.3204, close 1.3151

Today’s Bank of Canada monetary policy meeting promises a bit of drama. The BoC hiking rates is a given, only the size of the hike is in question. A 75 bp hike, the favoured outcome, would be quickly forgotten, while a 100 bp bump, would drive USDCAD toward support at 1.3030.

Even so, whatever the BoC decides, the market reaction will be brief.

The FX focus is on the Fed. Traders want to know how high US rates will rise and how long they will stay elevated. The BoC monetary policy decision is merely a distraction.

Recent US economic reports reflect a robust economy that can easily support higher interest rates. Yesterday’s ISM report was stronger than expected and helped lift the 10-year US Treasury yield to 3.35% from 3.208%.

WTI oil prices are being pressured by fears that a global economic slowdown will depress demand. The intraday technicals are bearish below $90.00/barrel which guards the longer-term downtrend line at $95.50. A decisive break below $85.00/b targets $59.10.

Canada’s Trade surplus narrowed to $4.05 billion from a the downwardly revised $4.88 billion in June.

USDCAD Technical outlook

The intraday USDCAD technicals are bullish above 1.3120, looking for a move above 1.3225 to target 1.3340, the 50% Fibonacci retracement level of the Covid range. A break below 1.3130 targets 1.3060, but only a move below 1.300 will negate the upside pressure.

For today, USDCAD support is at 1.3130 and 1.3060. Resistance is at 1.3230 and 1.3260. Today’s range: 1.3130-1.3230

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Different day, same old, same old. Fears of a global economic slowdown fueled by rising interest rates and the prospect that rates remain elevated for a long time knocked commodity prices and stocks lower and boosted US dollar demand against the G-10 currencies.

California, a state with a population that exceeds Canada’s, is experiencing its longest and hottest heat wave ever. And with it, rolling electrical blackouts. Government officials may be rethinking their ban on gas-powered cars by 2035 as they stroll to work in 100 F (37.8C) temperatures because they can’t charge their Teslas. They may die of heat stroke, but hey, they are saving the planet.

Russian President Mad-Vlad Putin blamed the EU for shutting down the Nord Stream 1 pipeline.

Yesterday it was a maintenance issue.

Wall Street closed with losses on Tuesday after slightly higher ISM data boosted Treasury yields. Asian equity indexes didn’t fare any better with a 1.42% drop in Australia’s ASX 200 leading them lower. European bourses opened defensively and continued to retreat with the UK FTSE 100 down 0.63%. S&P 500 and DJIA futures are flat. Gold and oil prices squeezed out small gains compared to Tuesday’s NY close.

The US 10-year Treasury yield consolidated yesterday’s gains and sits in the middle of its overnight 3.305-3.365% range.

EURUSD traded in a 0.9878-0.9929 range and remained under pressure from the ongoing Euro area energy crisis and war in Ukraine. Hawkish Fed speak suggesting higher rates for longer, and strong economic data suggesting the US economy can withstand higher rates overshadowed expectations for an ECB rate hike on Thursday. Eurozone GDP rose 4.1% y/y in Q2.

GBPUSD sank, rallied and sank again in a 1.1453-1.1522 range, as the euphoria from the announcement of Liz Truss as Prime Minister faded, and the focus shifted to US interest rates.

There is plenty of discussion about the Truss government’s spending plans which ING economists suggest may be weighing on the currency due to the UK’s very high debt burden.

USDJPY climbed 1.74% since yesterday’s NY opening, rising from 141.65 to 144.59 overnight. The gains were fueled by robust US data and hawkish Fed speak, which underscored the vast differences in monetary policy between the BoJ and Fed. As expected, the Ministry of Finance warned that they were watching FX markets closely, but the comments were laughed away. Even former BoJ Governor Watanabe said intervention in the market would be meaningless.

AUDUSD bounced in a 0.6701-0.6737 range. Australia’s GDP came in as expected, rising 0.9% q/q. NZDUSD mirrored AUDUSD moves and traded in a 0.5998-0.6042 range.

The US July trade deficit narrowed to $70.7 billion, in line with expectations.

Later today, there are speeches from Richmond Fed President Thomas Barkin and Cleveland Fed Loretta Mester.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

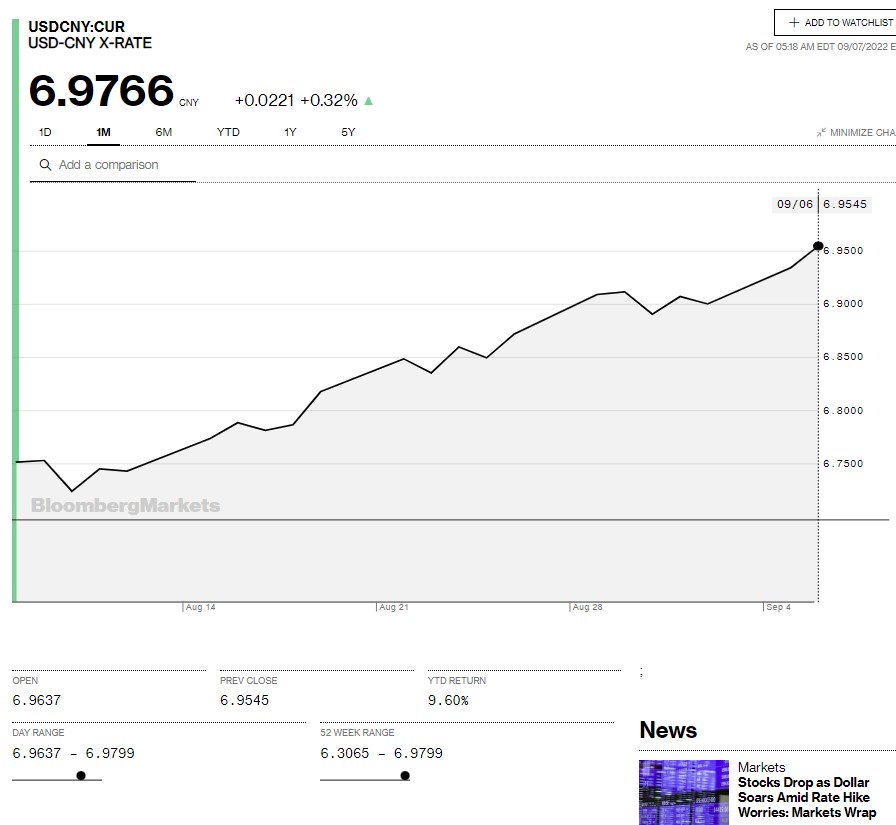

China Snapshot

Today’s Bank of China Fix: 6.9160, previous 6, 6.9096

Shanghai Shenzhen CSI 300 rose 0.02% to 4,054.98

August Trade Surplus $79.39 billion, July 101.26 b

CNN reports that since August 20, 74 cities with a population total of 313 million are in various lockdown stages, including 15 provincial capitals.

CNN said many of the lockdowns occurred because local officials want to show fealty to wannabe-emperor Xi Jinping

Chart: USDCNY 1 month

Source: Bloomberg